New Delhi: In a semi-urban pocket of Gujarat, a family that prides itself on being “financially aware” ticks many of the right boxes. They hold multiple bank accounts, transact regularly through UPI, maintain a small fixed deposit, and even dabble in stock trading through a mobile app. Yet when income dips unexpectedly, their response is immediate and familiar. Liquidate savings, delay repayments, and borrow informally.

This contradiction, between perceived financial sophistication and actual vulnerability, sits at the heart of India’s evolving financial landscape.

The Financial Maturity Index: A Survey of Two States, released by the IIM-Udaipur (IIMU) and People Research on India’s Consumer Economy (PRICE), provides perhaps the most comprehensive answer yet. Based on a primary survey of 4,075 individuals across Gujarat and Rajasthan, the report goes beyond access to decode how households actually make financial decisions.

The key contribution of the Financial Maturity Index (FMI) lies in its multi-dimensional and empirically grounded framework, which captures financial capability not as a static attribute but as a lived, behavioural outcome. It integrates 10 dimensions — from numeracy and literacy to resilience, behaviour and gender — offering a far more realistic lens on financial well-being.

What emerges is a sobering picture: while financial inclusion has expanded rapidly, financial maturity remains uneven, fragile, and deeply contextual.

Limits of Access: What Data Really Show

Over the past decade, India’s financial architecture has undergone a dramatic transformation. Bank account penetration has surged, digital payments have become ubiquitous, and access to credit and insurance has widened. Yet the FMI reveals that access alone does not guarantee informed usage.

“Financial maturity extends beyond financial literacy or inclusion. It reflects a household’s ability to make informed financial decisions, align financial actions with long-term goals, absorb shocks, and adapt,” says the report.

The data underline this gap sharply. In basic numeracy, while 95.4% of respondents in Gujarat and 92.7% in Rajasthan could correctly calculate wage-based earnings, only 65.6% in Gujarat and 52.7% in Rajasthan could correctly define inflation. Price arithmetic accuracy stands at 86.3% in Gujarat and 82.6% in Rajasthan, suggesting that while transactional competence is strong, conceptual clarity remains weak.

This divergence between operational competence and conceptual understanding is critical. It suggests that while households can manage day-to-day arithmetic, they struggle with forward-looking financial concepts that underpin savings and investment decisions.

The gaps widen further in sophisticated financial literacy. Despite increasing exposure to financial products, understanding of risk-return trade-offs, diversification, and insurance remains limited.

Many households continue to rely on traditional assets such as gold and land, often without a clear understanding of liquidity or risk implications. Notably, higher income does not necessarily translate into better financial literacy, exposing even relatively affluent households to risk.

“Financial deepening without commensurate growth in advanced literacy may amplify vulnerability rather than reduce it,” says the report.

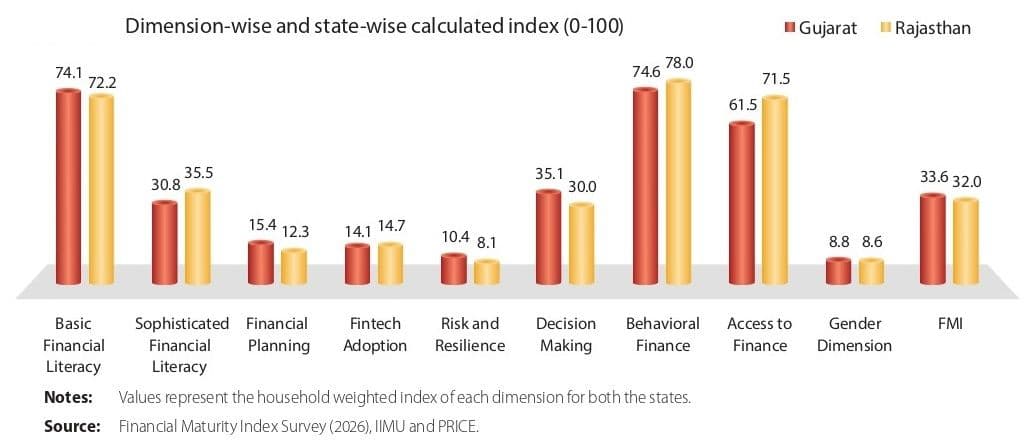

The survey also highlights stark differences between the two states. Gujarat, with a per capita income of ₹3.13 lakh and contributing 8.1% to India’s GDP, shows relatively better outcomes across most dimensions. Rajasthan, with a per capita income of ₹1.67 lakh and a 5% GDP share, exhibits wider gaps in literacy, access and preparedness.

Yet even in Gujarat, the gaps are far from negligible, reinforcing that financial maturity is not merely a function of income or access.

Behavioural Fault Lines

The most striking findings of the FMI lie in the behavioural domain. The report reveals that financial decision-making in Indian households is rarely structured, often reactive, and deeply influenced by psychological constraints.

“Between 60% and 80% of respondents report never reviewing their financial goals or asset allocation,” says the report.

This lack of periodic review reflects a broader absence of planning discipline. Financial decisions are typically concentrated within households, with only about one-third of respondents reporting independent decision-making. A significant proportion relies on spouses or family members, indicating fragmented financial agency.

Professional advice is conspicuously absent. Only around 11% of respondents consult financial advisors, and fewer than 5% engage with structured financial content or influencers. This leaves the vast majority navigating complex financial choices with limited guidance.

The consequences become stark when examining financial resilience. Over one-third of households reported experiencing a major emergency in the past five years. Yet fewer than 40% maintain an emergency fund covering even three months of expenses. Informal coping mechanisms — borrowing from relatives, rotating savings groups, or distress asset sales — remain widespread, especially in Rajasthan.

“More than half of respondents find financial matters stressful, and over one-third admit postponing important financial decisions,” says the report.

This behavioural inertia — driven by stress, uncertainty and cognitive overload — creates a disconnect between intent and action. While over 85% of households express a preference for saving over discretionary spending, this does not translate into consistent or disciplined financial behaviour.

Technology, often seen as a leveller, presents a nuanced picture. While digital adoption is high — driven by widespread use of UPI and mobile banking — its impact on financial maturity is uneven.

“Many households use digital platforms primarily for payments, while continuing to rely on informal channels for savings, credit, and insurance,” says the report.

This distinction between transactional usage and meaningful engagement is critical. Digital tools enhance efficiency but do not automatically improve decision-making capability.

The report also points to a dual financial landscape. A large majority remains conservative, preferring traditional assets and avoiding perceived risks, while a small segment participates in stock trading through digital platforms. This segment, though confident, often exhibits short-term trading behaviour rather than disciplined wealth accumulation, reflecting another dimension of immature financial engagement.

Policy Imperative: From Inclusion to Maturity

The Financial Maturity Index fundamentally reframes the policy conversation. It shifts the focus from expanding access to strengthening capability, from infrastructure to behaviour, and from uniform solutions to targeted interventions.

“The FMI enables identification of specific capability gaps whether in planning discipline, risk understanding, access quality, or behavioural constraints,” says the report.

This diagnostic power is particularly valuable in a country as diverse as India. The contrast between Gujarat and Rajasthan illustrates how financial maturity is shaped not just by income levels but by institutional environments, education, and social structures.

Gender emerges as a critical dimension. The report finds that households with greater female participation in financial decision-making exhibit stronger savings behaviour, better repayment discipline, and improved long-term planning. Yet significant disparities persist, especially in Rajasthan, where women often face barriers such as lack of collateral, documentation, and institutional bias.

“Financial maturity is not gender-neutral. Policies that enhance women’s agency can generate disproportionate gains,” says the report.

Access itself, while improved, remains uneven in quality. Households report challenges ranging from distance to bank branches and ATMs to delays in transactions, poor connectivity, and difficulties in accessing welfare transfers. Even among banked households, barriers such as documentation requirements and institutional capacity constraints limit effective usage.

Equally concerning is the gap between awareness and long-term financial planning. Retirement preparedness remains one of the weakest areas. Most households have not initiated structured retirement planning, as immediate priorities — education, health, and daily consumption — dominate financial thinking. Insurance penetration, though growing, remains shallow in terms of effective coverage and understanding.

“Retirement planning stands out as the most critical deficiency, with most households yet to begin structured preparation for old age,” says the report.

The implications for policy are far-reaching. Financial education must move beyond awareness to behavioural change. Product design must incorporate flexibility and simplicity. Institutional trust must be strengthened through transparency and reliability.

Crucially, the FMI itself offers a scalable framework for periodic measurement. By constructing a composite index using rigorous statistical techniques and rescaling it to a 0-100 range, it enables benchmarking across states and over time.

As India’s financial ecosystem becomes increasingly complex — with rising credit penetration, expanding digital finance, and growing participation in market-linked products — the need for financial maturity will only intensify.

The evidence from the FMI is unequivocal. Financial inclusion has laid the foundation, but without financial maturity, the edifice remains incomplete.

For millions of households navigating an expanding universe of financial choices, the difference between access and understanding is no longer academic, it’s is the defining factor between resilience and vulnerability.