New Delhi: India’s non-banking financial companies (NBFCs) have completed a remarkable transition from a sector battling a liquidity crisis to one that has become a critical driver of credit expansion and financial inclusion. Strong balance-sheet growth, improving asset quality and rapid digital adoption have reinforced their position in the country’s financial system, although rising funding costs and tighter regulation are beginning to test profitability.

The latest industry assessment comes at a time when NBFCs are extending credit faster than banks in several high-growth segments, including retail, MSMEs and infrastructure, while adapting to a more demanding regulatory environment shaped by lessons from the IL&FS collapse and the pandemic.

According to the latest report by Brickwork Ratings, the sector has undergone a structural transformation over the past decade. “The Indian NBFC sector has emerged as a resilient, digitally empowered catalyst for India’s financial inclusion and growth story. NBFCs contribute nearly one-fourth of India’s total credit portfolio, complementing banks by serving high-growth, high-risk segments that traditional lenders often avoid,” says the report.

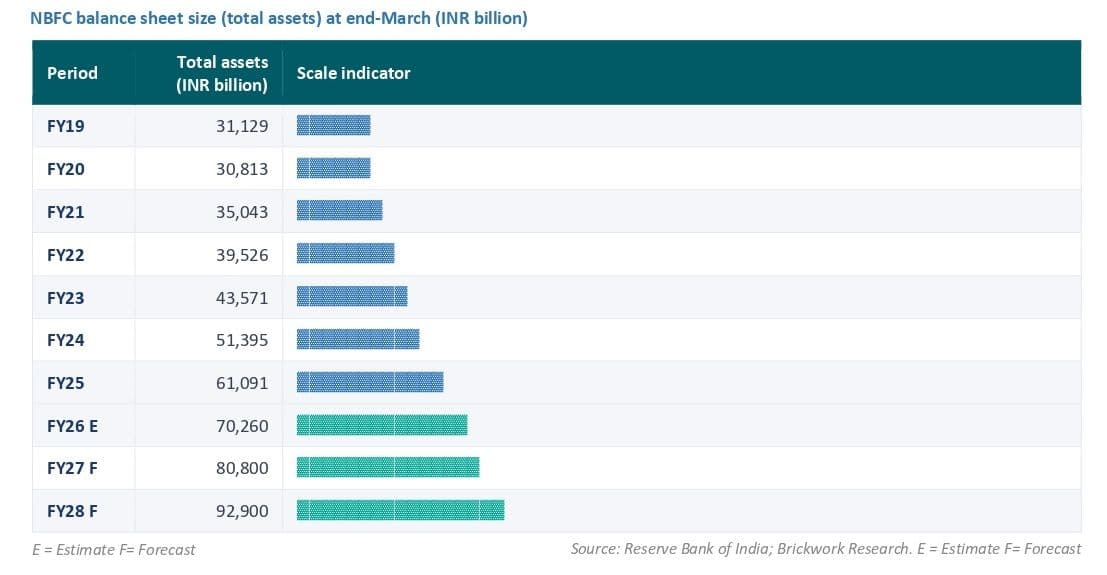

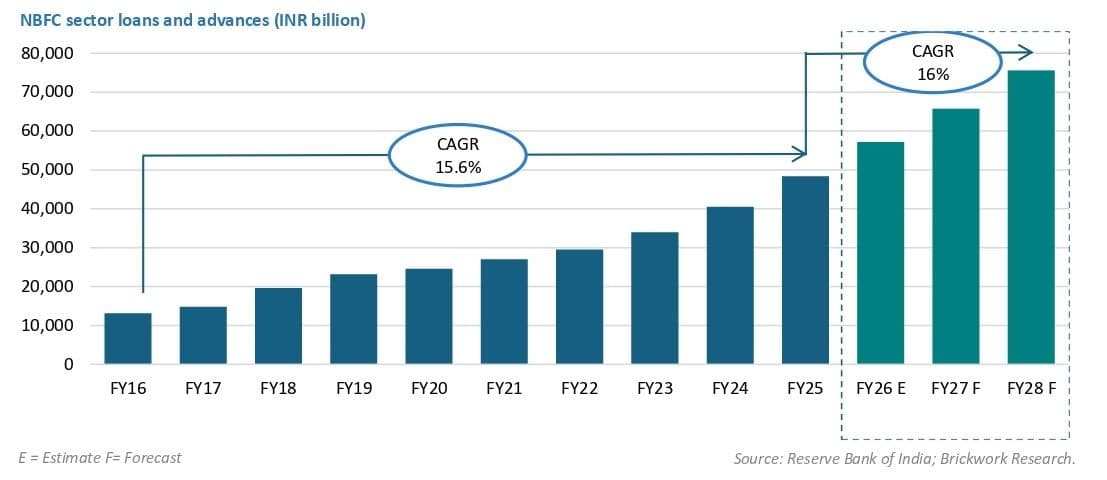

The report estimates total NBFC assets at Rs 61.1 trillion in FY25, up 18.9% from the previous year, while loans and advances increased 19.4% to Rs 48.4 trillion. Borrowings climbed 21% to Rs 41.8 trillion, underlining both the sector’s rapid expansion and its growing interconnectedness with banks and capital markets.

Growth outpaces banks

NBFCs are steadily widening their footprint across India’s credit ecosystem. Credit growth of 19.4% in FY25 comfortably exceeded the 11.5% expansion recorded by scheduled commercial banks, reflecting strong demand from households, small businesses and infrastructure projects.

The report says this growth is reshaping the financial landscape. “NBFC credit growth has structurally outpaced GDP growth, with the NBFC credit-to-GDP ratio rising from approximately 12.1% in FY19 to approximately 14.6% in FY25. Since FY22, NBFCs have accelerated credit growth. Credit growth reached 19.4% YoY in FY25, outpacing the scheduled commercial banks' growth of 11.5%.”

Industry and retail lending continue to dominate the portfolio mix, accounting for about 81% of total advances. Power projects remain the largest component of industrial credit, while vehicle finance retains its position as the backbone of retail lending. Gold loans have emerged as one of the fastest-growing segments as lenders shift towards secured assets following regulatory tightening in unsecured retail credit.

MSME financing is also becoming a larger growth engine, with its share of the portfolio increasing to 9.9%. The report attributes this to specialised underwriting models and technology-driven lending platforms that enable NBFCs to serve segments where conventional banks have limited reach.

Digital transformation is emerging as another competitive advantage. According to the report, fintech partnerships, account aggregator frameworks and platform-based lending are helping NBFCs improve operational efficiency while expanding access to credit in rural and underserved markets.

Profitability moderates

Despite the robust growth trajectory, profitability has softened under the weight of rising funding costs and higher provisioning requirements.

Net profit declined 6.2% to Rs 1.32 trillion in FY25, while return on equity moderated to 10.1% from 13% a year earlier. Return on assets stood at 2.3%, although early FY26 trends indicate some recovery as credit costs stabilise.

The report notes that the sector has entered a more balanced phase after years of volatility. “The NBFC sector’s profitability cycle has transitioned from a painful reset in FY20-FY22, rooted in the collapse of Infrastructure Leasing & Financial Services (IL&FS) in late 2018, which triggered a severe liquidity crunch across the shadow banking sector. This painful reset gave way to a golden era in FY23-FY24.”

Asset quality continues to improve. Gross non-performing assets declined to 2.9% in FY25 from 3.5% a year earlier, supported by stronger underwriting standards and better recoveries. At the same time, the report cautions that unsecured retail lending and microfinance portfolios remain vulnerable to stress, particularly as household leverage rises.

A significant change for the sector has been the Reserve Bank of India’s Scale-Based Regulation framework, which classifies NBFCs according to their size and systemic importance. Larger entities now face bank-like regulatory standards, including stricter governance, liquidity and capital requirements, increasing compliance costs but strengthening long-term resilience.

The funding environment is also changing. While bank borrowings remain a major source of capital, larger NBFCs are increasingly tapping bond markets, commercial paper and other market-linked instruments to diversify liabilities and reduce refinancing risks.

Long-term prospects

The medium-term outlook for the sector remains positive, supported by India’s economic growth, infrastructure spending and expanding financial inclusion agenda.

The report projects NBFC assets to rise to about Rs 92.9 trillion by FY28, while loans and advances are expected to exceed Rs 75 trillion. Borrowings are also forecast to grow steadily as lenders broaden their funding base.

However, the growth story is likely to be accompanied by greater scrutiny. Rising wholesale funding costs, geopolitical uncertainties, currency volatility and tighter liquidity norms could pressure margins, especially for smaller players with concentrated funding profiles.

The report sums up the sector’s next phase of evolution in measured terms. “The outlook for NBFCs remains stable with moderating growth. Strong fundamentals, balance sheet resilience, and digital transformation provide growth momentum. However, heightened regulatory scrutiny and asset quality risks temper optimism. The sector's trajectory will hinge on managing unsecured loan exposures, diversifying funding sources, and sustaining profitability amid competitive pressures.”

For India’s financial system, the message is clear. NBFCs have moved beyond being alternative lenders to becoming an indispensable part of the country’s credit architecture. Their ability to balance rapid expansion with disciplined risk management will determine whether they can sustain their role as one of the principal engines of India’s next phase of economic growth.

(Cover photo by Towfiqu barbhuiya on Unsplash)