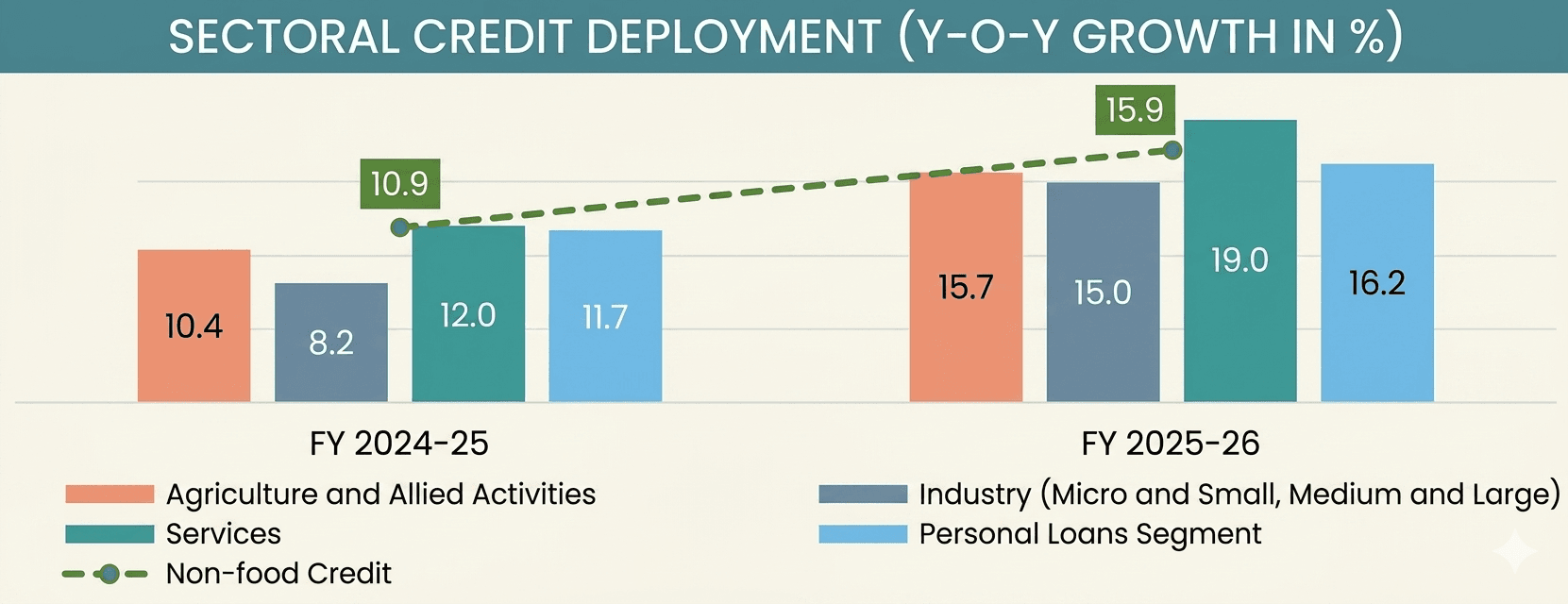

New Delhi: India’s scheduled commercial banks (SCBs) posted a strong 15.9% year-on-year non-food credit growth in FY 2025-26, signalling a solid economic momentum. This marks a sharp acceleration of 497 basis points over the 10.9% growth seen a year earlier, underscoring a broad-based revival in credit demand across sectors.

The numbers are striking not just for their scale but for their spread too. Aggregate credit outstanding surged to ₹212.9 lakh crore by March 2026, reflecting an annual increase of ₹29.2 lakh crore. This expansion comes amid a low-interest rate environment and a government-led capex cycle that appears to be catalysing private investment, reinforcing confidence among both corporates and households.

What stands out in FY26 is the depth of participation across sectors. The services sector, which accounts for 28% of total credit, emerged as the primary driver, posting a sharp 19% growth compared with 12% in the previous year. Demand from non-banking financial companies (NBFCs), trade and commercial real estate played a pivotal role in this expansion, indicating strong activity in both financial intermediation and urban economic cycles.

Close behind, the personal loans segment, which constitutes a substantial 33% share of overall credit, expanded by 16.2%, up from 11.7% last year. While housing credit maintained steady momentum, the real push came from vehicle loans and loans against gold jewellery, pointing to resilient consumption patterns and rising household confidence.

The industrial sector, often seen as a bellwether for long-term economic health, also staged a notable recovery. Credit growth nearly doubled to 15% from 8.2% a year ago, with micro and small industries registering a remarkable 33.1% growth — 3.7 times higher than the previous year. Medium industries followed with a robust 21.7% expansion.

This surge reflects renewed momentum in segments such as infrastructure, basic metals, chemicals, petroleum, coal products and nuclear fuels, suggesting that capacity expansion and investment cycles are gaining traction.

Equally significant is the revival in agriculture and allied activities, where credit growth accelerated to 15.7%, up from 10.4% last year. The 528 basis point jump signals sustained rural demand and improved formalisation of credit flows into the farm sector, an encouraging sign for income stability and consumption in rural India.

The broader macro narrative is one of resilience. Despite a challenging global backdrop marked by geo-economic fragmentation and geopolitical tensions, India continues to position itself as the fastest-growing major economy. The strength of the banking sector — characterised by well-capitalised balance sheets, historically low impaired assets and sustained profitability — has played a crucial role in enabling this growth.

Importantly, the nature of credit expansion suggests a virtuous cycle at work. Increased borrowing by corporates is translating into capacity creation and fixed asset investments, while household credit is fuelling demand for durable goods. Together, these trends are supporting industrial activity, employment generation and overall economic momentum.

Policy continuity and structural reforms appear to be reinforcing this trajectory. Government efforts aimed at democratising and formalising credit are clearly visible in the widening credit base, particularly in rural and MSME segments. The crowding-in of private investment alongside public capex further strengthens the outlook for sustained growth.

The credit data is a reflection of an economy where confidence is returning across sectors, financial intermediation is deepening and the appetite for growth is firmly intact.

The SCBs in India are: State Bank of India, Bank of Baroda, Bank of India, Bank of Maharashtra, Canara Bank, Central Bank of India, Indian Bank, Indian Overseas Bank, Punjab National Bank, Punjab & Sind Bank, Union Bank of India and UCO Bank.

Note: (Y-o-Y growth is calculated based on credit offtake as on April 4, 2025 against March 31, 2026. With effect from December 31, 2025, definition of last reporting fortnight has been changed to the last day of the month under the Banking Laws (Amendment) Act 2025. Accordingly, the y-o-y growth rates from December 2025 onwards are based on end-of-month data for the current year and data for the last reporting fortnight (as per old definition) for the corresponding month of the previous year)