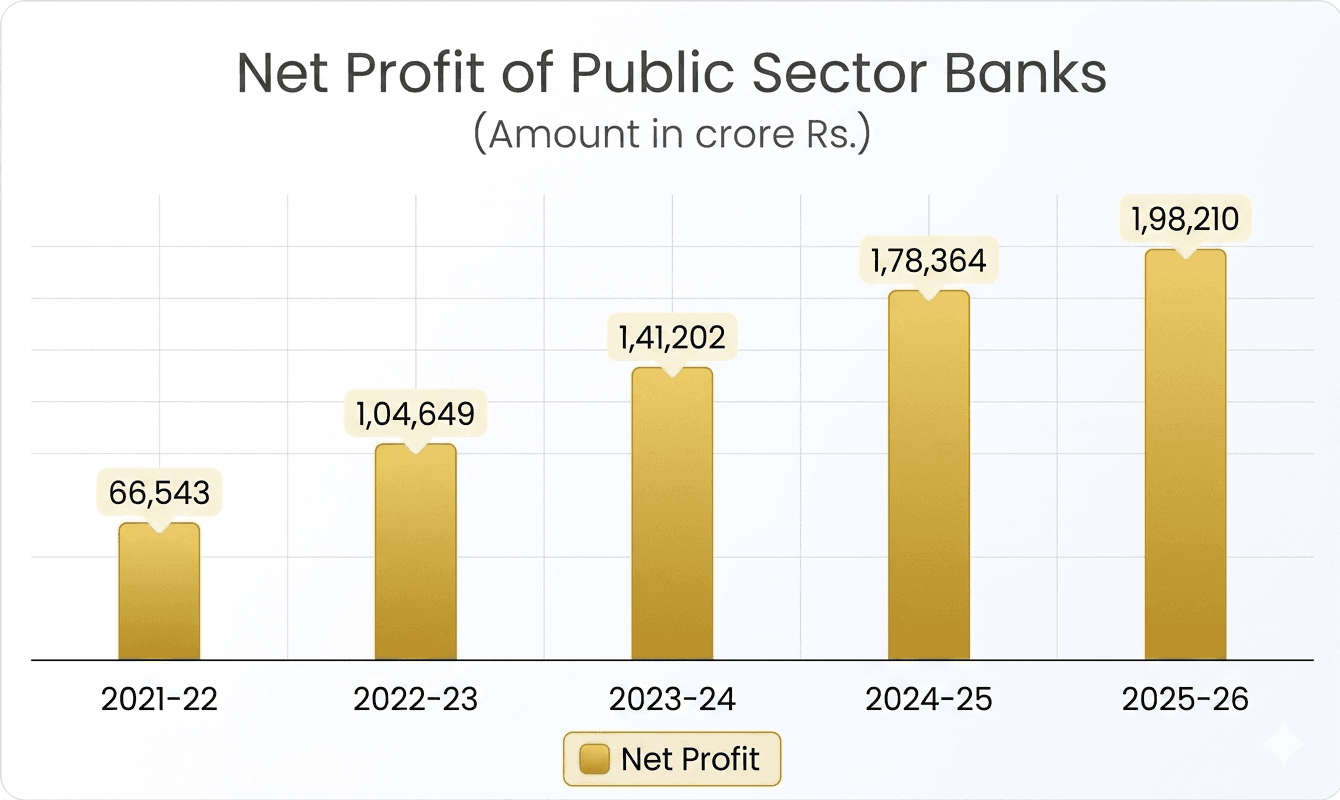

New Delhi: India’s public sector banks (PSBs) have delivered their strongest financial performance on record, underscoring a dramatic turnaround in the country’s nationalised banking sector after years of stress, mounting bad loans, and weak balance sheets. The PSBs together reported a historic aggregate net profit of ₹1.98 lakh crore in FY2025-26, marking an 11.1% year-on-year rise and the fourth consecutive year of profitability for the sector.

The numbers reflect far more than an earnings milestone. They signal the emergence of a fundamentally stronger public banking system that is now better capitalised, operationally efficient and capable of sustaining India’s accelerating credit demand. The turnaround is particularly striking given that less than a decade ago, several PSBs were grappling with soaring non-performing assets (NPAs), weak governance structures, and repeated capital infusion requirements.

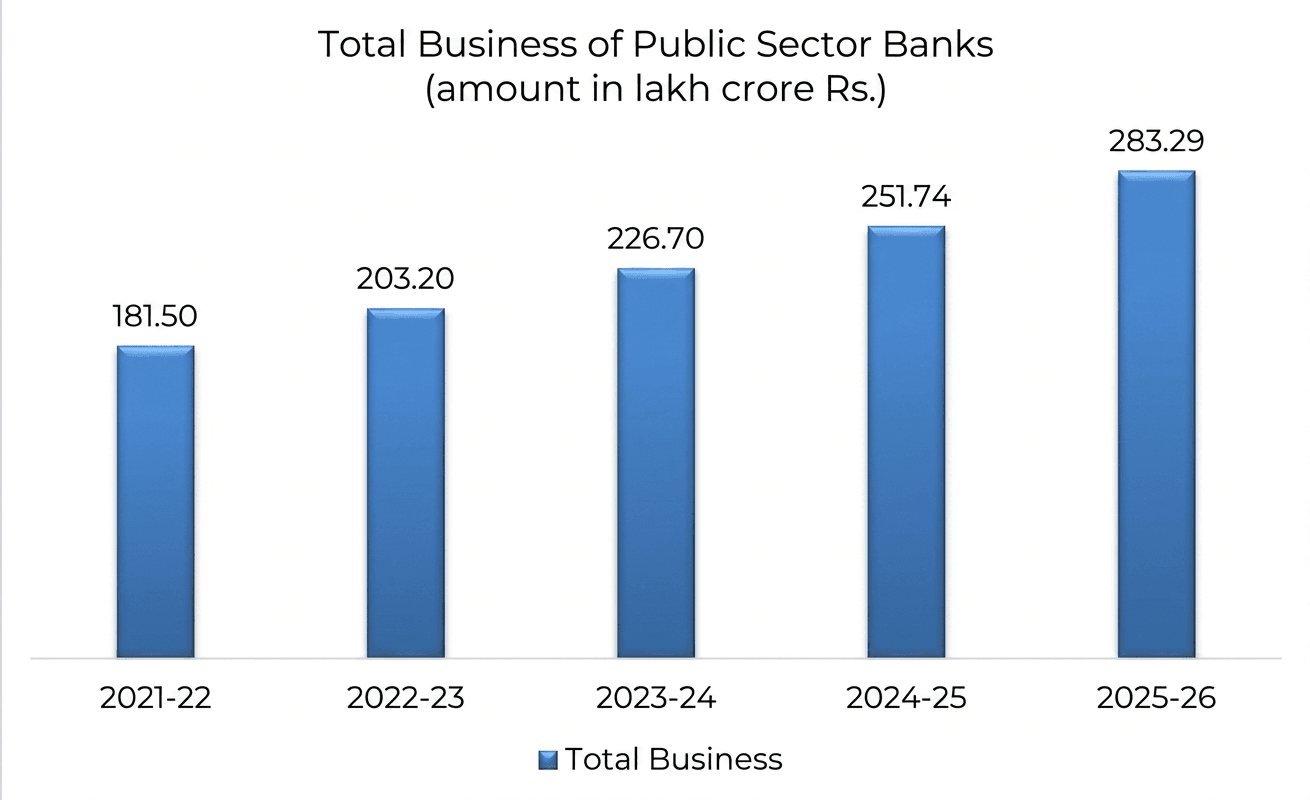

The latest financial data shows that the aggregate business of PSBs rose 12.8% year-on-year to ₹283.3 lakh crore as of March 31, 2026. Aggregate deposits increased 10.6% to ₹156.3 lakh crore, indicating strong depositor confidence despite heightened competition from private banks and small finance institutions. Gross advances expanded 15.7% to ₹127 lakh crore, reflecting broad-based credit growth across sectors of the economy.

The sharp improvement in profitability has been driven by a combination of healthier loan books, lower provisioning burdens, stronger recoveries and sustained expansion in high-yield retail and MSME lending. Aggregate operating profit climbed to ₹3.21 lakh crore during FY26, providing banks with a stronger earnings buffer and internal capital generation capacity.

The resurgence of PSBs also comes at a critical moment for the Indian economy, which is witnessing rapid infrastructure expansion, rising private investment and increased formalisation of credit demand. State-owned lenders continue to remain central to financing these growth ambitions, particularly in sectors where private lenders remain relatively cautious.

Credit Momentum

One of the most significant aspects of the FY26 performance has been the broad-based expansion in credit, especially in the retail, agriculture and MSME (RAM) segments. Retail advances grew 18.1% year-on-year, while agriculture loans rose 15.5%. MSME lending expanded by 18.2%, reflecting a sustained push towards financial inclusion, entrepreneurship and small business financing.

The strong credit momentum highlights how PSBs have repositioned themselves from legacy corporate lenders burdened by stressed infrastructure loans into diversified banking institutions with stronger retail franchises and deeper rural penetration. The RAM portfolio has increasingly become the growth engine for PSBs, helping improve margins while reducing concentration risks associated with large corporate exposures.

The growth in retail lending has been aided by rising demand for housing loans, vehicle finance and personal credit, supported by urban consumption recovery and digital banking expansion. Meanwhile, the agriculture segment has continued to receive policy support amid rising rural credit requirements and increasing mechanisation in farming activities.

The MSME segment remains especially critical for India’s economic growth narrative. PSBs have significantly increased lending to small and medium enterprises through government-backed credit guarantee schemes, digitised loan processing and improved underwriting mechanisms. The strong expansion in MSME credit indicates improving confidence among small businesses and a wider revival in entrepreneurial activity.

Importantly, the latest figures suggest that PSBs are now growing without sacrificing balance sheet quality. Historically, rapid credit growth in public sector banks often translated into future asset quality deterioration. The FY26 data, however, points towards stronger underwriting discipline and tighter risk management frameworks.

Operational efficiency has also improved significantly. The aggregate cost-to-income ratio declined to 49.67%, reflecting tighter expense management and increasing gains from technology adoption, digital banking and process automation. PSBs, once perceived as laggards in digital transformation, have accelerated investments in mobile banking platforms, analytics-driven lending and digital customer acquisition.

This operational transformation has become increasingly important as PSBs face intense competition from private sector lenders and fintech companies. The ability to improve efficiency while simultaneously expanding credit has strengthened investor confidence in the sector’s long-term sustainability.

Asset Revival

The clearest evidence of the PSB turnaround lies in the dramatic improvement in asset quality. Gross NPA ratio declined to 1.93% as of March 31, 2026, while net NPA ratio fell to just 0.39%, representing historically low levels of stressed assets for the sector.

The reduction in bad loans marks a remarkable shift from the banking crisis years when PSBs were weighed down by massive corporate defaults, particularly in infrastructure, steel and power sectors. At the peak of the crisis, several state-owned banks had gross NPA ratios running into double digits, severely eroding profitability and constraining fresh lending.

The latest data indicates that PSBs have successfully repaired their balance sheets through aggressive recognition of bad loans, higher provisioning, recoveries under insolvency frameworks and stronger monitoring mechanisms. Fresh slippages during FY26 continued to decline, with the slippage ratio reducing further to 0.7%.

The recovery process has also gathered momentum. Total recoveries, including those from written-off accounts, stood at ₹86,971 crore during FY26. The recoveries reflect the increasing effectiveness of institutional mechanisms such as the Insolvency and Bankruptcy Code (IBC), stricter recovery frameworks and improved borrower discipline.

Another critical indicator of banking resilience is the provisioning coverage ratio (PCR). Every PSB maintained a PCR above 90% during FY26, demonstrating prudent provisioning practices and stronger preparedness against future stress. High provisioning buffers ensure that banks remain insulated from sudden asset quality shocks and improve confidence among investors and depositors alike.

The sharp decline in NPAs has had a direct impact on profitability. Lower provisioning requirements have enabled banks to retain a larger share of operating income as net profit. Combined with rising loan growth and improving margins, this has fundamentally altered the earnings profile of PSBs.

The turnaround also reflects years of structural reforms initiated by the government and regulators. Measures aimed at improving governance standards, strengthening credit appraisal systems, consolidating weaker banks and enhancing accountability have gradually restored financial stability in the sector.

Equally important has been the increasing use of technology in risk assessment and loan monitoring. Data analytics, centralised credit processing and early warning systems have helped banks identify stress faster and improve underwriting quality. This institutional strengthening has reduced the likelihood of a repeat of the large-scale corporate lending excesses seen in the previous decade.

Capital Strength

The stronger profitability and improved balance sheet quality have significantly enhanced the capital position of PSBs. Aggregate Capital to Risk Weighted Assets Ratio (CRAR) improved to 16.6% as of March 31, 2026, comfortably above the regulatory requirement of 11.5%.

The improvement has been supported by robust internal accruals, retained earnings and capital raising of ₹50,551 crore during FY26. The healthy capital buffers provide PSBs with adequate headroom to sustain future lending growth without immediate dependence on government recapitalisation.

This marks a major shift in the financial architecture of state-owned banking. For years, PSBs relied heavily on taxpayer-funded capital support to absorb losses arising from bad loans. Today, stronger earnings generation has enabled several banks to independently strengthen their capital base, improving both operational autonomy and market confidence.

The strengthened capital position assumes greater importance as India seeks to sustain high economic growth over the coming decade. Infrastructure financing, manufacturing expansion, renewable energy investments and rising consumer demand will require substantial credit support. PSBs, given their extensive branch networks and dominant market share in deposits, are expected to remain central to this financing cycle.

The government has consistently argued that reforms in governance, technology adoption, credit discipline and institutional accountability are now yielding visible results. The FY26 performance numbers appear to validate that argument. State-owned lenders are no longer merely surviving after a prolonged clean-up cycle; they are emerging as profitable and competitive financial institutions.

The broader macroeconomic backdrop has also aided the recovery. Stable economic growth, rising formalisation, healthy tax collections and stronger corporate balance sheets have contributed to lower credit stress across sectors. In addition, increased digital adoption has expanded banking penetration and reduced transaction costs.

Yet challenges remain. Sustaining high credit growth while preserving asset quality will require continued vigilance. Rising global uncertainty, geopolitical tensions and evolving interest rate cycles could create fresh stress pockets. Competitive pressure from private banks and fintech firms is also intensifying, particularly in retail and digital banking segments.

Nevertheless, the FY26 numbers represent a defining milestone for India’s public sector banking system. The record ₹1.98 lakh crore net profit is not merely an accounting achievement. It reflects the rebuilding of institutional credibility after one of the most difficult phases in Indian banking history.

Today, PSBs are significantly stronger than they were a decade ago — cleaner, better capitalised, technologically sharper and more profitable. As India advances towards its long-term ambition of becoming a developed economy under the Viksit Bharat 2047 vision, the revival of public sector banks may well prove to be one of the most consequential financial transformations of the past decade.