New Delhi: India’s digital payments landscape has entered a new phase where consumer behaviour is being shaped less by loyalty to a single payment mode and more by the context of spending.

The latest findings from the How India Pays 2025-26 report by Phi Commerce show that while UPI continues to dominate daily transactions, consumers are increasingly turning to credit cards and EMIs not only for discretionary purchases but also for routine and essential expenses.

The shift signals a deeper structural transformation in the country’s payments ecosystem. Consumers are now selecting payment instruments based on ticket size, urgency, convenience and cash-flow management, creating what industry executives describe as a “toolkit approach” to digital spending. The change is simultaneously reshaping merchant strategies, with businesses broadening payment acceptance to improve conversion and customer retention.

UPI Strengthens Grip On Essential Payments

The report is based on transaction data processed through the Phi Commerce payment gateway during FY26 and draws insights from more than 20,000 merchants across sectors including retail, healthcare, education, utilities, electronics and food and beverages.

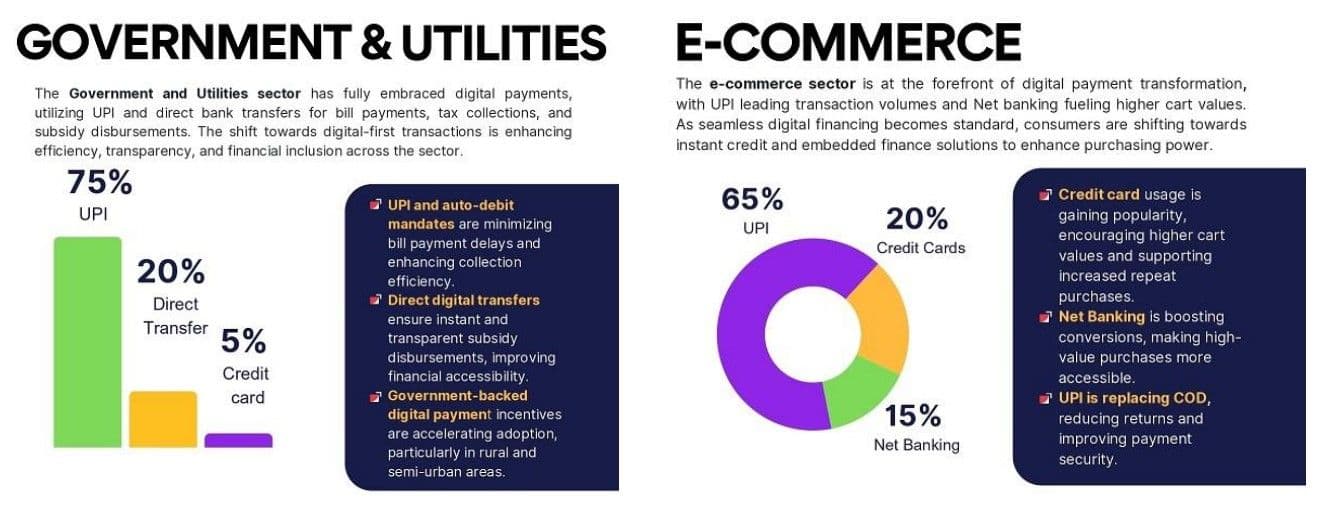

It underlines how UPI has moved far beyond low-value peer-to-peer transactions to become the default payment infrastructure for critical and high-value sectors. In education, UPI now accounts for 88% of transactions, overtaking net banking, which traditionally dominated fee payments and institutional transfers. Healthcare has witnessed a similar transition, with 72% of payments now routed through UPI, reflecting growing consumer confidence in using instant payment systems for large hospital and medical bills.

The findings reinforce the rapid maturation of India’s digital payments ecosystem, where speed and convenience are no longer the only drivers of adoption. UPI’s acceptance for high-friction sectors indicates that users increasingly view the platform as dependable infrastructure for essential payments.

Rajesh Londhe, co-founder and head of payments, Phi Commerce, said, “What we are seeing is a clear shift from default-driven to decision-driven payment behaviour in India. Consumers are no longer relying on a single method, such as UPI, for all transactions. Instead, they are actively choosing instruments based on context, using UPI for speed and convenience, while increasingly turning to credit cards and EMIs for planned and even routine expenses. Credit is no longer confined to big-ticket purchases; it is becoming embedded in everyday spending decisions.”

The report also highlights how consumer behaviour now varies sharply by time of day and spending intent. UPI dominates daytime transactions, particularly in categories such as food and beverages, where payment volumes peak during midday hours. The trend reflects the platform’s continuing strength in high-frequency, low-friction retail consumption.

Credit and EMIs Move Into Everyday Spending

Even as UPI consolidates its leadership in instant payments, structured credit is rapidly emerging as a mainstream tool for managing household finances. The report shows that EMIs now account for 34% of transactions in government and utility payments, suggesting that consumers are increasingly financing even essential expenditures.

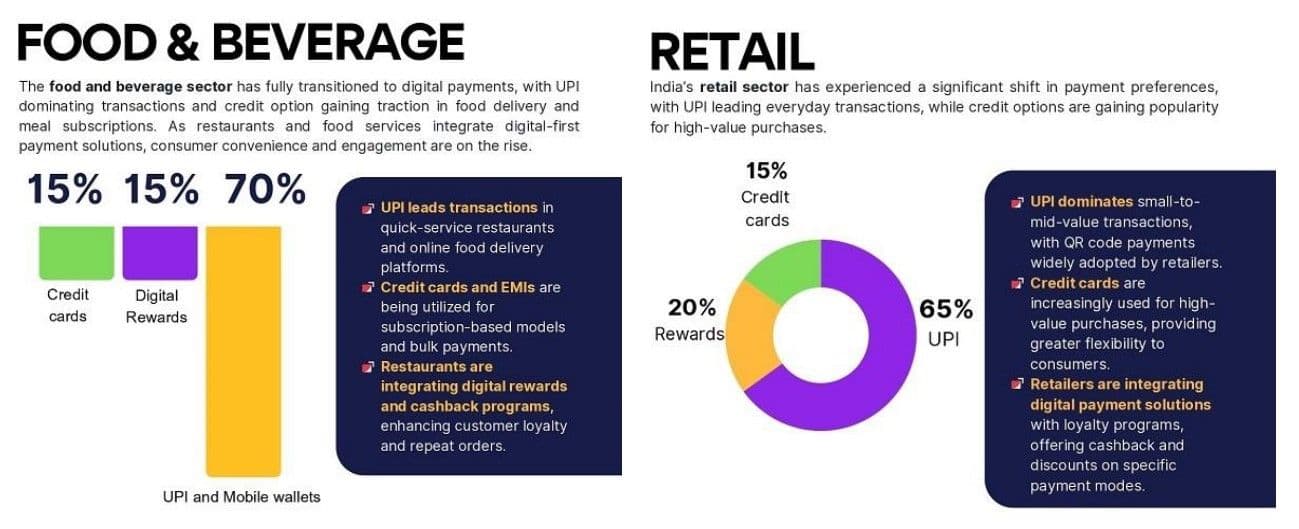

The trend is equally visible in discretionary categories. In electronics, EMIs contribute to 36% of purchases, reinforcing their role in enabling affordability amid rising consumer aspirations and tighter cash-flow management. Industry observers say this marks a decisive shift from episodic borrowing to embedded credit usage across recurring spending cycles.

The report further points to a strong evening preference for credit-based payments. Between 2000 hours and 2300 hours, credit cards account for 72% of high-value retail transactions as consumers increasingly prioritise rewards, deferred payment flexibility and spending optimisation.

The divergence between daytime UPI usage and evening credit card spending reflects a more mature digital economy in which payment choices are closely aligned with intent. Consumers are no longer “digital-only” in behaviour; instead, they are selectively combining UPI, cards, EMIs, wallets and vouchers depending on the nature of the transaction.

This evolution is also forcing businesses to rethink payment acceptance strategies. Merchants across retail, healthcare, education and e-commerce are expanding payment options to align with consumer preferences and reduce transaction drop-offs.

“As India’s payments ecosystem matures, the competitive advantage will lie with businesses that can align payment options with context. The ability to offer the right instrument at the right moment, whether for speed, affordability, or rewards, is emerging as a key driver of both customer experience and transaction success,” Londhe added.