New Delhi: India’s real estate sector could require nearly ₹50 lakh crore in capital over the next decade as urbanisation, rising household incomes and formal housing demand reshape the country’s property market. Yet, even as premium and luxury housing attract increasing investor attention, affordable housing continues to face a widening funding deficit, according to Anarock Capital’s report, Powering the Next Decade: India’s Real Estate Finance Transformation Story.

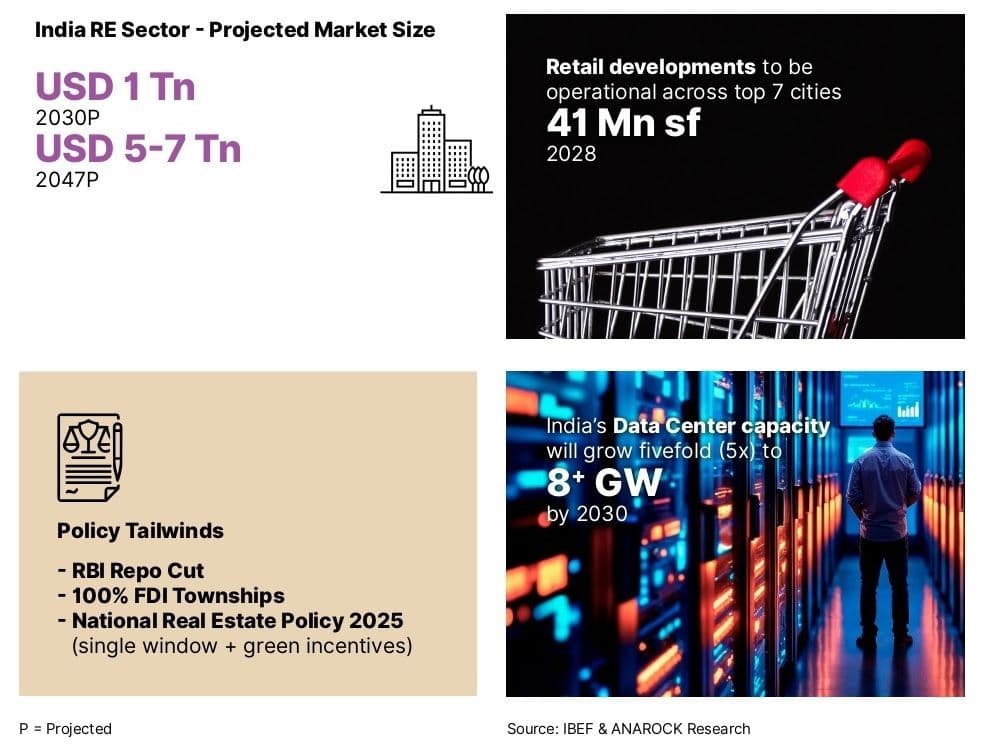

The report estimates that India’s real estate market could touch nearly $1 trillion by 2030 and potentially scale up to $5-7 trillion by 2047, powered by rapid infrastructure creation, expanding urban populations and deepening institutional participation in the sector. However, the financing architecture remains uneven, with capital heavily concentrated among top-tier developers and metropolitan markets.

“India’s real estate sector will absorb roughly ₹50 lakh crore of capital over the next decade. The question is no longer whether the demand is there — urbanisation, rising household incomes, and a generational shift toward formal housing have settled that argument. The question is whether the capital that funds this demand will be efficient, accountable, and broad-based, or whether the sector will repeat the structural failures of the 2018-19 NBFC cycle,” said Anarock Capital CEO Shobhit Agarwal, in the report.

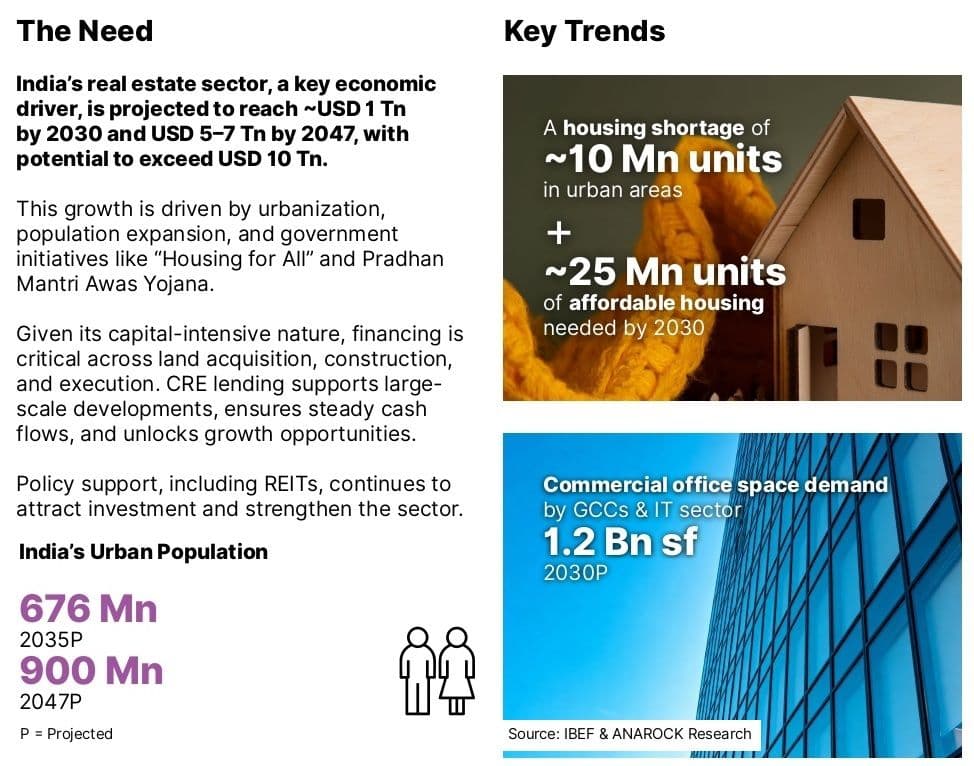

The report said affordable housing remains chronically underserved despite carrying the country’s largest demand-supply mismatch. India is expected to require nearly 25 million affordable housing units by 2030, while urban housing shortages are already estimated at around 10 million units. Yet, affordable homes priced below ₹40 lakh accounted for only 10% of new housing supply in the first quarter of 2026, down sharply from 26% in 2021.

At the same time, premiumisation of the housing market has accelerated. Homes priced above ₹1.5 crore contributed 53% of new launches during Q1 2026, underscoring the shift in developer focus toward higher-margin projects. According to the report, average residential prices across the top seven cities rose 7% year-on-year to ₹9,456 per sq ft, with NCR recording the sharpest increase at 15%.

The report said the funding ecosystem has become more institutional and regulated after the disruptions caused by demonetisation, RERA implementation, the IL&FS collapse and the DHFL crisis. Banks have selectively returned to commercial real estate lending, while Alternative Investment Funds (AIFs), REITs and private credit platforms have emerged as dominant financing channels.

“Affordable housing — the segment with the largest demand–supply gap and the highest social return — remains chronically underfunded by formal capital. Tier II & Tier III developers are still locked out of institutional lending. Capital concentrates in the same five cities and the same fifteen sponsors,” said the report.

Funding Divide Deepens

According to Anarock, mortgage financing remains the backbone of India’s property market, with total outstanding individual housing loans crossing ₹38 lakh crore by February 2026. However, institutional capital has increasingly gravitated toward Grade-A commercial assets, luxury residential projects, logistics parks and data centres, leaving mass housing projects struggling for liquidity.

The report highlighted that nearly 80% of the overall commercial real estate lending book remains concentrated in Mumbai Metropolitan Region, NCR and Bengaluru. Smaller cities and regional developers continue to face limited access to formal credit due to stringent underwriting norms and restrictions on land financing.

“Real estate financing in India today looks fundamentally different from what it did a decade ago. It is more institutional, more regulated, and more accountable. But the next phase will not be won by adding more vehicles for the same set of borrowers. It will be won by extending the financing stack — to the affordable segment, to the smaller developer, to the cities outside the top five,” Agarwal said in the report.

The report observed that banks’ exposure to commercial real estate has grown at a 13% CAGR over the past five years, reaching over ₹5.2 lakh crore in H1 FY26. However, banks remain reluctant to fund land acquisition and approval-stage projects, forcing developers to rely on higher-cost AIF and NBFC funding structures.

That funding imbalance has become especially visible in the affordable housing segment. The report noted that more than 4.5 lakh homebuyers remain affected by stalled affordable and mid-income housing projects across India, with stressed inventory estimated at over ₹4.8 lakh crore in 2024.

While the government-backed SWAMIH Fund has revived several stalled projects, the report argued that structural financing bottlenecks remain unresolved.

“The SWAMIH Fund was a meaningful intervention for stalled projects, but it does not address the upstream problem: institutional capital still treats most of the Indian real estate market as un-bankable. This is no longer a capital availability problem. It is a capital architecture problem,” the report said.

Institutional Shift Accelerates

The report said India’s real estate financing ecosystem is undergoing a structural transition led by REITs, AIFs, sovereign capital and private credit funds. Listed REITs now collectively account for nearly ₹2.1 lakh crore in market capitalisation, while global institutional investors continue to increase allocations toward income-generating office, warehousing and logistics assets.

Office leasing across the top seven cities touched a record 58.2 million sq ft in 2025, while warehousing stock expanded more than threefold over seven years to 605 million sq ft. India’s data centre capacity is also projected to exceed 8 GW by 2030, opening up a major financing opportunity for institutional investors.

The report said developers with strong balance sheets, lower leverage and completed inventory are likely to attract capital more easily as lenders become increasingly risk-conscious under tighter RBI norms.

“Geopolitical headwinds may create short-term friction — higher costs, tighter liquidity, cautious capital flows — but they are unlikely to alter India’s long-term real estate story. As global supply chains rewire in India’s favour and the AI economy takes root, the country is uniquely positioned to convert external disruption into domestic opportunity,” the report said.

The report added that India’s long-term real estate growth story remains intact because of strong domestic demand, expanding infrastructure investment and a deepening formal financing ecosystem. However, unless affordable housing and smaller developers receive broader institutional funding support, the sector risks becoming increasingly skewed toward premium urban assets.

(Cover photo by Yash Parashar on Unsplash)