New Delhi: The global real estate market entered 2026 on a cautiously improving trajectory, but the escalation of the Iran-Israel war has injected a fresh layer of uncertainty into that recovery. Disruptions to energy supply routes, particularly through the Strait of Hormuz, have pushed oil prices higher, reignited inflation concerns and complicated the outlook for interest rates. For property markets, the implications have been immediate and tangible. Rising input costs, tighter financing conditions and heightened investor caution are beginning to weigh on transaction momentum just as activity had started to revive.

The market had begun to stabilise in 2025, even as structural shifts in capital allocation and sectoral preferences continued to reshape the investment landscape, says the March 2026 Global Capital Flows report by Colliers. According to the report, global real estate investment volumes increased by 8.2% year-on-year in 2025, marking a return to growth after a prolonged downturn triggered by aggressive monetary tightening. While this headline figure suggests a recovery, the underlying dynamics point to a market that remains uneven, with clear divergences across regions and asset classes.

Within this global context, India presents a distinct and increasingly important narrative. One that reflects both vulnerability to external shocks and the emergence of new domestic demand drivers.

India’s exposure to the ongoing conflict in West Asia is significant, given its reliance on imported crude oil. Elevated energy prices are already feeding into inflation, raising construction costs and putting pressure on project feasibility. Developers are contending with higher input prices for materials such as steel and cement, as well as increased logistics costs, all of which could slow the pace of new supply.

At the same time, inflationary pressures are likely to affect housing demand, particularly in interest rate-sensitive segments. As borrowing costs remain elevated and household budgets tighten, affordability constraints could weigh on residential sales in the near term.

Yet, as the broader trends highlighted in the Colliers report suggest, periods of disruption often trigger shifts in capital flows; and India is beginning to see the effects of such a reallocation. The geopolitical instability in the Gulf region has led to a reverse flow of both labour and capital back into India. Returning professionals and entrepreneurs are increasingly directing savings into domestic real estate, particularly in emerging urban centres.

This is contributing to a noticeable rise in demand in Tier-2 and Tier-3 cities, where affordability and improving infrastructure are attracting both end-users and investors. In contrast to the cautious sentiment in global institutional markets, these localised dynamics are providing a degree of resilience to India’s residential sector.

Beyond India, the Colliers Global Capital Flows report underscores the uneven nature of the recovery across major regions.

North America emerged as the strongest performer in 2025, with investment volumes rising by 15.4%, significantly ahead of the global average. The Colliers report notes that this recovery was consistent throughout the year, with most months recording higher activity than in 2024. This reflects both the depth of the US market and the relative speed at which investors adapted to higher interest rates.

In Europe, the Middle East and Africa, investment volumes increased by 8.6%, broadly in line with global trends. However, the Colliers report highlights that much of this growth was concentrated in the second half of the year, with a particularly strong fourth quarter indicating improving investor confidence.

Asia-Pacific, by contrast, recorded a more subdued 1.7% increase in investment volumes. The Colliers report points out that while the region showed early strength, activity declined toward the end of the year, falling by 10% compared to the same period in 2024. Nevertheless, transactions in core assets rose by around 8%, signalling continued confidence in prime markets.

Cross-border investment patterns further illustrate the shifting geography of global capital. As highlighted in the Colliers report, EMEA continues to dominate as the primary destination for international real estate investment, with seven of the top 10 global markets located in the region.

The United Kingdom retained its position as the largest recipient of cross-border capital, attracting $26.3 billion and accounting for 15.7% of global flows, according to Colliers. The United States followed with $24.1 billion, exceeding its five-year average share and reflecting renewed investor interest.

At the same time, the Colliers report notes that several traditional European strongholds, including Germany, Spain and the Netherlands, saw a decline in their relative share of activity. In contrast, markets such as France and Sweden gained ground, while Japan and Australia strengthened their position within Asia-Pacific.

Sectoral trends, as detailed in the Colliers analysis, point to an increasingly competitive investment landscape. Multi-family assets remained the largest sector globally, accounting for 24.9% of total activity. However, the gap with industrial and office assets has narrowed significantly, with shares of 22.7% and 21.3% respectively.

The report highlights that multi-family continues to be supported by strong demand fundamentals, particularly in the United States. Industrial assets remain buoyed by logistics and supply chain requirements, while office investment has shown signs of recovery, especially in EMEA and APAC, where it recorded a 16% increase in the latter half of 2025.

Retail has also regained momentum, now accounting for 15.6% of global investment activity, while hospitality remains comparatively smaller at 7.6%. One of the most notable trends identified in the Colliers report is the rise of data centres as a distinct asset class, capturing 4.8% of total investment and expected to expand further.

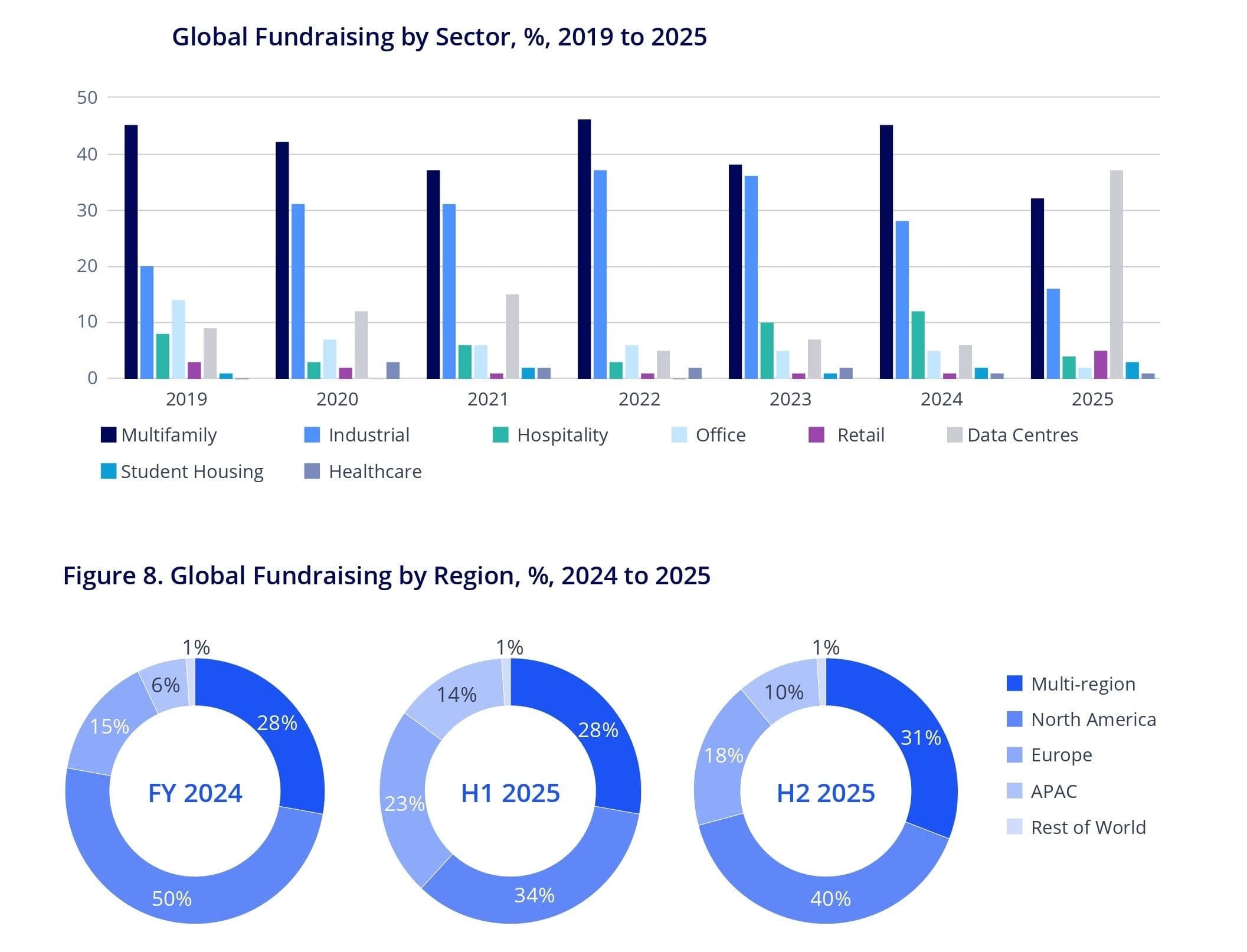

Fundraising activity provides further evidence of shifting investor priorities. The Colliers report notes that global real estate fundraising reached $222 billion in 2025, representing a 28.9% increase over the previous year and making it one of the strongest fundraising years since 2019.

A key feature of this rebound is the growing preference for higher-risk strategies. Opportunistic funds accounted for 33% of total capital raised, up from 25% in 2024, while value-add strategies declined to 22%. Combined, these approaches represented 55% of fundraising activity, reflecting a willingness among investors to capitalise on market dislocations.

The Colliers report also highlights a significant shift in sectoral allocations within fundraising. Data centres have emerged as the leading focus, capturing 37% of total capital raised, overtaking multifamily, which accounted for 32%. This underscores the increasing importance of digital infrastructure in global investment strategies.

Geographically, the distribution of fundraising has shifted as well. North America’s share declined from 50% in 2024 to 40% in 2025, while Europe and Asia-Pacific recorded substantial increases of 52% and 109% respectively, according to Colliers. This rebalancing is expected to support stronger investment activity in these regions in 2026.

On the capital supply side, the Colliers report identifies the United States as the largest source of global real estate investment, accounting for 25.4% of cross-border flows, albeit below its five-year average. Other markets, including Canada, the United Kingdom, Sweden, Norway and key Asian economies, have increased their share, indicating a broader diversification of capital sources.

The macroeconomic outlook remains a critical factor shaping real estate markets. The Colliers report suggests that economic growth in 2026 will remain positive but uneven, with Asia-Pacific expected to lead, while Europe and the Americas experience more moderate expansion.

At the same time, inflation and interest rate trajectories remain uncertain, particularly in light of the ongoing geopolitical tensions in West Asia. While some markets are seeing inflation ease, others continue to face upward pressure, complicating the path of monetary policy.

For real estate investors, the relationship between yields and borrowing costs will be central to decision-making. The Colliers report indicates that yield spreads are expected to improve modestly in 2026, although rising long-term bond yields could present a challenge to capital allocation.

Taken together, the findings of the Colliers Global Capital Flows report point to a market in transition. The recovery in 2025 has laid the groundwork for renewed activity, but the outlook for 2026 is being reshaped by geopolitical risks, shifting capital flows and evolving sectoral dynamics.

In this environment, the global real estate market is likely to be defined not by uniform growth, but by divergence across regions, sectors and investment strategies. For India, this divergence presents both challenges and opportunities, as domestic demand drivers and shifting capital flows interact with an increasingly complex global landscape.

(Cover photo by Sean Pollock on Unsplash)