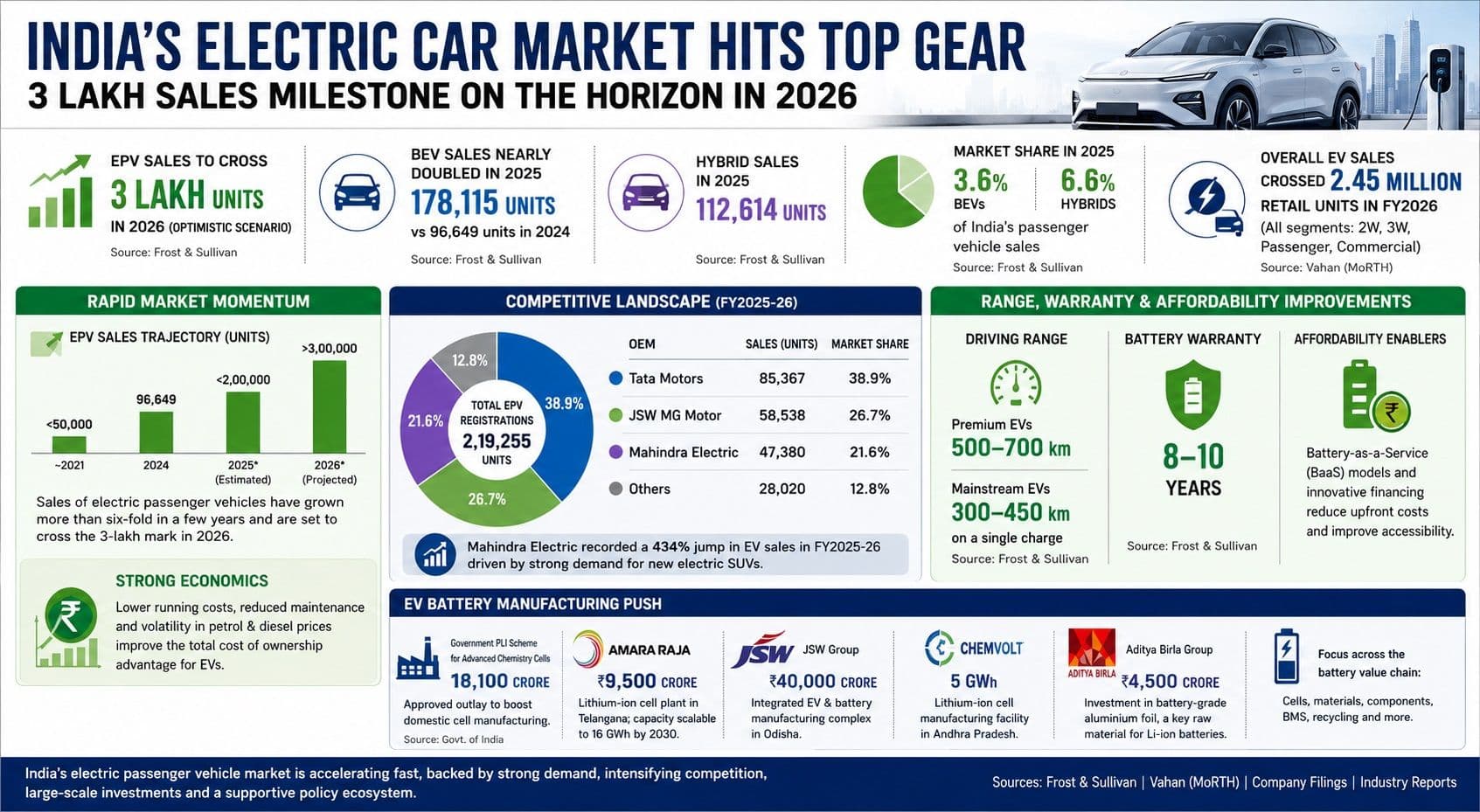

New Delhi: After years of gradual adoption, India’s electric passenger vehicle market is finally entering the mainstream. According to the latest Frost & Sullivan outlook, annual EPV sales are projected to exceed 3 lakh units in 2026 under its optimistic scenario, marking the first time the segment will cross the milestone as consumer acceptance, product availability and domestic manufacturing continue to strengthen.

The forecast comes after another year of rapid expansion. Battery electric vehicle (BEV) sales almost doubled to 178,115 units in 2025 from 96,649 units in 2024, while full-hybrid vehicle sales rose to 112,614 units. As a result, BEVs accounted for 3.6% of India’s passenger vehicle sales last year, with hybrids contributing another 6.6%, taking electrified powertrains to more than one in every 10 new passenger vehicles sold.

The pace of growth is striking considering annual electric passenger vehicle sales remained below 50,000 units only a few years ago. The market has expanded rapidly as battery costs moderated, model choices widened and charging infrastructure improved, making electric cars increasingly viable beyond early adopters.

The momentum is mirrored across the broader automobile industry. According to Vahan retail registration data, India’s overall EV market — including two-wheelers, three-wheelers, passenger vehicles and commercial vehicles — crossed 2.45 million retail sales in FY2026, underscoring the speed at which electrification is spreading across vehicle categories.

Consumer economics continue to improve. Although electric cars still command a higher upfront purchase price than comparable petrol or diesel models, running costs remain substantially lower. Continued volatility in petrol and diesel prices is expected to further strengthen the total cost of ownership advantage for EVs, particularly for high-mileage urban users and commercial fleet operators.

Technology is also removing some of the biggest barriers to adoption. Premium EVs now deliver driving ranges of 500-700 km, while mainstream models offer 300-450 km on a single charge. Battery warranties have extended to 8-10 years, and innovative financing structures such as Battery-as-a-Service (BaaS) are reducing upfront ownership costs by separating battery ownership from vehicle purchase.

Competition Reshapes Industry

The rapid expansion of India’s electric passenger vehicle market is fundamentally altering the competitive landscape.

For nearly four years, Tata Motors dominated India’s electric passenger vehicle segment. That dominance is gradually giving way to a more balanced market as established automakers and new entrants accelerate investments and launch dedicated EV platforms.

Industry registration data for FY2025-26 show Tata Motors remained the market leader with 85,367 electric passenger vehicle registrations, translating into a 38.9% market share. However, competition has intensified sharply. JSW MG Motor captured 26.7% of the market, while Mahindra Electric accounted for 21.6%.

Mahindra emerged as the fastest-growing major manufacturer, recording a 434% jump in EV sales during FY2025-26 as its new electric SUV portfolio gained traction. The changing market shares illustrate how India’s EV industry is transitioning from a single-player market into a genuinely competitive ecosystem.

Consumers are expected to be the biggest beneficiaries. More than a dozen new electric passenger vehicle launches are planned over the next two years across hatchback, crossover, SUV and premium segments. Greater competition is likely to accelerate innovation, improve localisation, expand consumer choice and place downward pressure on prices.

Automakers are backing those ambitions with unprecedented investments. Tata Motors recently announced plans to nearly double passenger vehicle sales to over 1.2 million units annually by FY31, from around 640,000 units currently. The company plans to invest ₹330-350 billion across its passenger vehicle and EV businesses between FY26 and FY30, with electric vehicles already contributing around 14% of its passenger vehicle sales.

International manufacturers are also expanding their India strategies as the country emerges as both a high-growth domestic market and a potential export hub for electric vehicles amid global supply chain diversification.

Fleet demand is adding another layer of momentum. Ride-hailing companies, leasing firms, corporate mobility providers and businesses pursuing decarbonisation targets are steadily increasing electric vehicle purchases as lower operating costs improve long-term fleet economics.

Battery Race Intensifies

Behind India’s EV boom lies an equally significant transformation in battery manufacturing.

Battery packs account for nearly one-third to 40% of an electric vehicle’s production cost, making localisation critical for improving affordability and reducing import dependence. To accelerate domestic manufacturing, the government launched the ₹18,100-crore production linked incentive (PLI) scheme for advanced chemistry cells, encouraging companies to establish large-scale battery manufacturing facilities within India.

The investment pipeline is expanding rapidly.

Amara Raja Energy is investing approximately ₹9,500 crore to build an advanced lithium-ion battery manufacturing facility in Telangana, with planned capacity scaling to 16 GWh by 2030. JSW Group has announced an investment of around ₹40,000 crore for an integrated electric vehicle and battery manufacturing complex in Odisha, while ChemVolt Global is developing a 5 GWh lithium-ion cell manufacturing plant in Andhra Pradesh.

The supply chain is expanding beyond battery cells. Aditya Birla Group is investing nearly ₹4,500 crore to manufacture battery-grade aluminium foil, a key component in lithium-ion batteries, highlighting the emergence of an integrated domestic battery ecosystem.

Lower battery costs are expected to remain the biggest catalyst for mass-market EV adoption. Global lithium prices have retreated significantly from their 2022 highs, while wider adoption of lithium iron phosphate (LFP) chemistry is enabling manufacturers to offer safer batteries with longer life cycles at lower costs.

Challenges nevertheless remain. Charging infrastructure outside major urban centres continues to lag demand, financing costs remain elevated compared with mature EV markets and battery raw material supply chains remain exposed to geopolitical uncertainty. Consumer concerns over resale values and battery degradation are gradually easing but have not disappeared entirely.

The projected crossing of the 3 lakh-unit annual sales milestone represents far more than another industry record. It signals that India’s electric passenger vehicle market is entering a new phase where growth will increasingly be driven by competitive products, expanding domestic manufacturing and improving economics rather than subsidies alone.

With automakers investing hundreds of billions of rupees, battery manufacturers building giga-scale factories and consumers embracing electrified mobility at an accelerating pace, India is laying the foundations for one of the world’s fastest-growing electric passenger vehicle markets over the remainder of the decade.

(Cover photo by Oxana Melis on Unsplash)