New Delhi: Gold’s spectacular rally may have paused, but the precious metal remains one of the world’s most closely watched assets as investors weigh whether the recent correction marks the end of a historic bull run or merely a breather before another surge.

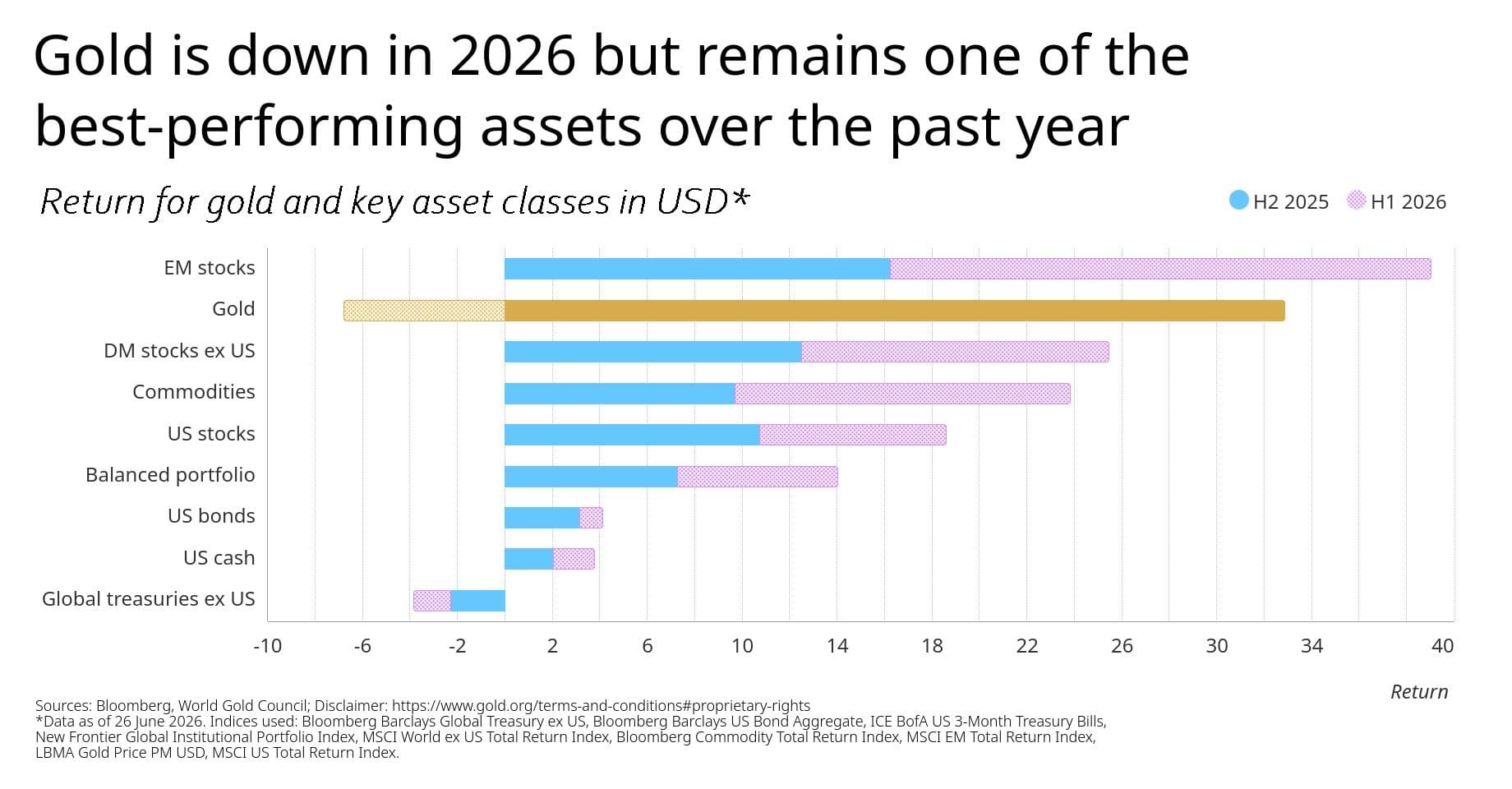

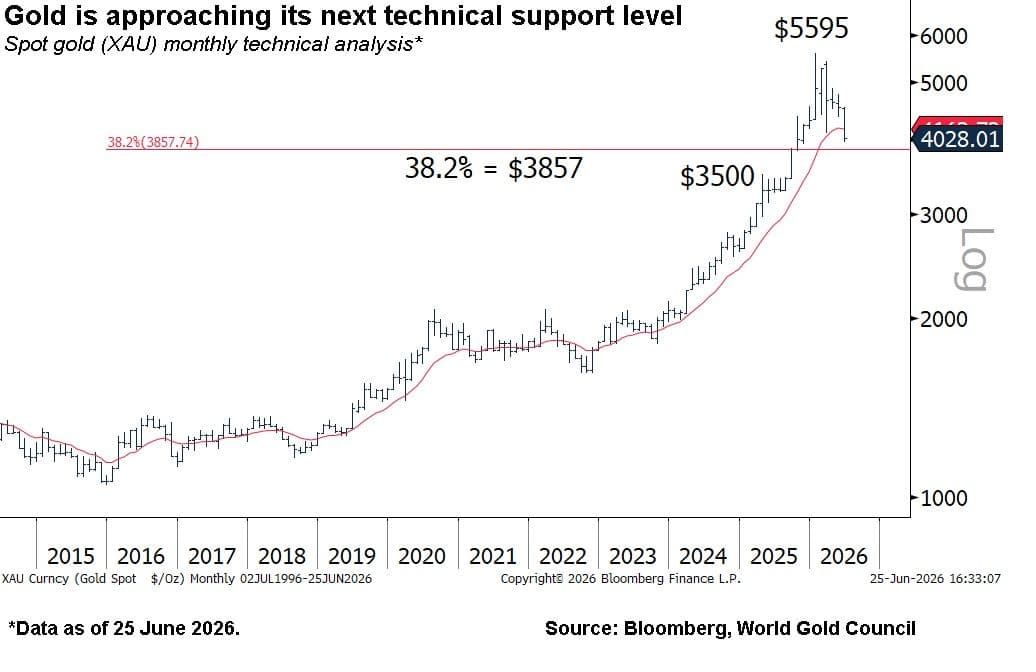

After climbing to an all-time intra-day high above $5,500 an ounce in January, gold tumbled below $4,000 in late June, capping one of the most volatile six-month periods in recent history. Despite the correction, bullion continues to outperform most traditional asset classes over the past 12 months, underlining its enduring appeal during periods of geopolitical uncertainty and financial market turbulence.

The World Gold Council’s Gold Mid-Year Outlook 2026 suggests the metal has entered a decisive phase where macroeconomic developments, monetary policy, geopolitical tensions and structural buying patterns will determine whether prices remain range-bound or resume their long-term climb.

Unlike previous cycles, the report argues that gold is no longer being driven primarily by US monetary policy or the dollar. Instead, multiple demand centres across Asia, sustained purchases by central banks and evolving investor behaviour have transformed the way prices are discovered in global markets.

The report highlights that the current gold price broadly reflects expectations of moderate global economic growth, cooling but elevated inflation and limited additional monetary tightening by major central banks. Under such conditions, bullion is expected to fluctuate within a relatively narrow range of around ±5% during the second half of 2026 unless fresh catalysts emerge.

“At current levels, gold’s price is broadly in line with a global backdrop of moderate growth, cooling but still elevated inflation, and expectations of further — but limited — central bank tightening. Under these conditions, gold will likely stay relatively range-bound (±5%). But the stage is set for a possible breakout.”

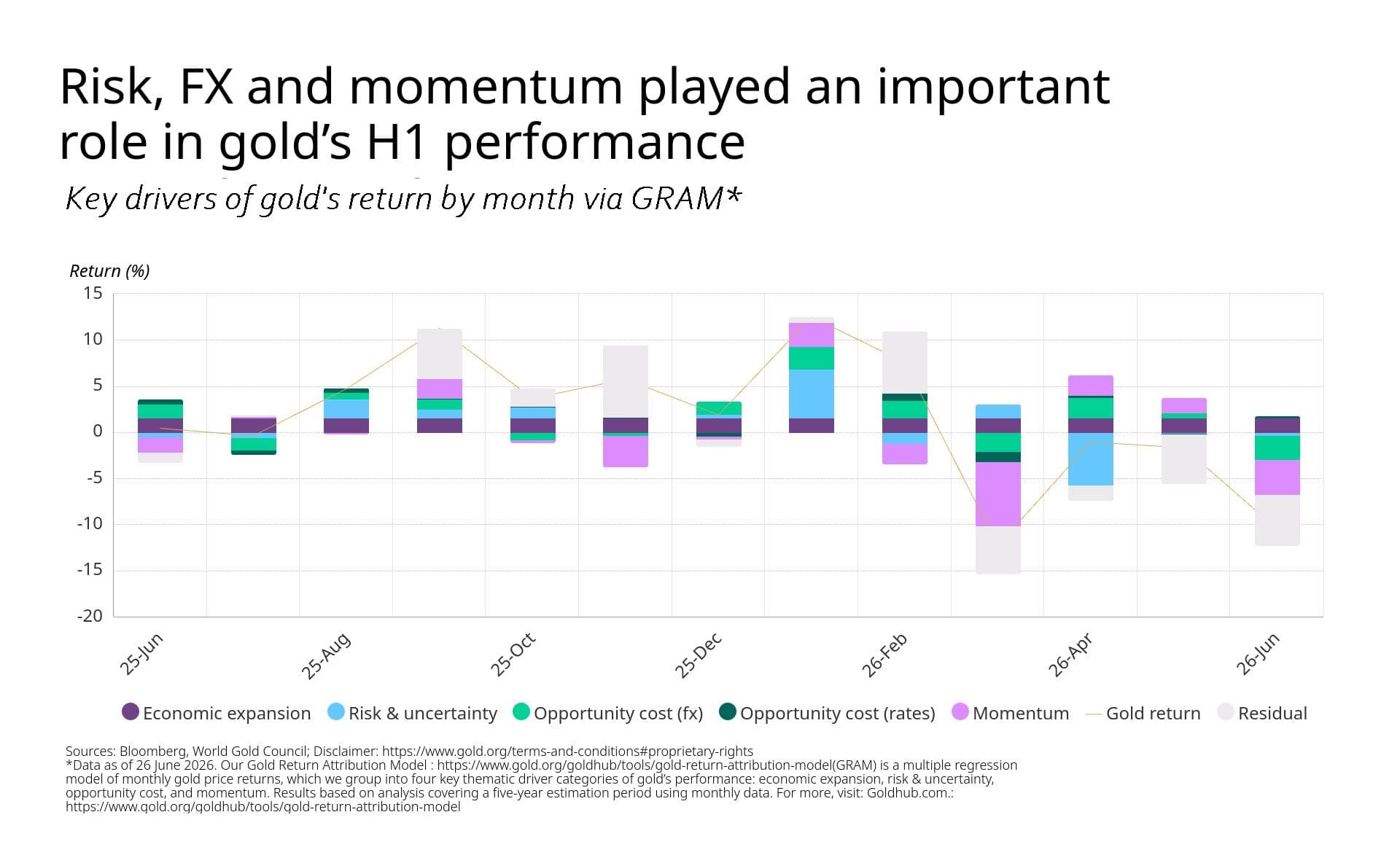

Volatility has also eased considerably after the spike witnessed during the US-Iran conflict, although it remains well above long-term averages. According to the report, geopolitical risk, investor positioning and momentum have together accounted for a significant share of gold’s performance this year, outweighing traditional drivers such as interest rates.

Asia Drives Demand

Perhaps the most significant structural change emerging from the latest outlook is the growing influence of Asian markets on global gold pricing.

The World Gold Council’s analysis of intraday trading patterns shows that much of gold’s recovery during recent market corrections occurred during Asian trading hours, while several sharp declines originated during US trading sessions. The shift suggests that Asian investors and consumers are becoming increasingly influential in determining global bullion prices, reflecting both stronger investment demand and the region’s expanding economic weight.

That changing market structure comes as investors increasingly question whether gold has already priced in the global economic outlook.

The report concludes that bullion remains fairly valued under prevailing macroeconomic assumptions. However, it identifies three powerful catalysts capable of reigniting the rally: a deterioration in global economic or geopolitical conditions, a reversal in interest-rate expectations and renewed participation from long-term institutional investors.

Should these factors materialise simultaneously, gold could climb back towards $4,500 an ounce, while stronger-than-expected shocks could propel prices towards $5,000 once again.

“The short answer is yes; but it requires a clear catalyst. This could come from three primary sources: worsening economic or geopolitical conditions, a reversal in interest-rate expectations, and long-term investor participation.”

The report also notes that financial markets continue to underestimate the influence of geopolitical shocks. Historically, every 100-point monthly increase in the Geopolitical Risk Index has lifted gold prices by about 2.5%, reinforcing bullion’s traditional role as a hedge during periods of heightened uncertainty.

At the same time, investors remain alert to the implications of the upcoming US midterm elections, evolving Federal Reserve policy and persistent inflation risks. Even though markets currently expect at least one additional rate increase before year-end, the report argues that a shift towards more dovish expectations could once again strengthen gold’s appeal relative to fixed-income assets.

Central Banks Cushion

Even if macroeconomic conditions remain supportive of risk assets, the World Gold Council believes structural demand is likely to prevent a sharp and prolonged decline in bullion prices.

Among the biggest pillars of support is central bank buying, which has fundamentally altered the global gold market over the past four years. Official institutions have collectively purchased an average of nearly 1,000 tonnes annually since 2022, helping absorb supply and reinforcing investor confidence. While several central banks sold or swapped small quantities during the first quarter, the report expects the official sector to remain a net buyer through 2026, although the pace of accumulation may moderate.

The report estimates that an additional 20-30 tonnes of purchases above the long-term annual average of around 600 tonnes could increase gold prices by roughly 1%. Beyond the direct impact on demand, such buying also sends a powerful signal to institutional investors about the metal’s strategic role in reserve management.

Long-term investors are emerging as another important force reshaping the bullion market. Sovereign wealth funds, pension funds, insurance companies and endowments have steadily increased their allocations to gold, reducing the market's dependence on short-term speculative flows.

China’s decision last year to allow some of its largest insurance companies to invest in gold marks another milestone in the diversification of institutional demand. According to the report, these buy-and-hold investors could provide an important stabilising influence if prices come under renewed pressure during the second half of the year.

“Our analysis suggests that, all else equal, an additional 20t-30t increase in reserves above the long-term average of around 600t per year should translate into approximately a 1% increase in the gold price. This effect comes not only from the central bank purchases themselves but also from the positive signal it sends to investors.”

The report nevertheless cautions that downside risks cannot be ignored. Stronger-than-expected global growth, rising bond yields, renewed dollar strength and improving investor confidence could reduce safe-haven demand. Technical factors may also amplify any correction, particularly if key price support levels are breached. However, historical patterns indicate that significant declines have generally attracted fresh buying from consumers, investors and central banks, limiting deeper drawdowns over time.

India Shapes Outlook

India, the world’s second-largest gold market, occupies a pivotal position in the World Gold Council’s outlook, with domestic policy decisions expected to have an outsized influence on global demand during the remainder of the year.

Unlike China, India depends almost entirely on imports to meet domestic consumption. That makes gold purchases sensitive not only to consumer sentiment but also to government policy aimed at managing the current account deficit and preserving foreign exchange reserves.

Following disruptions to oil supplies during the US-Iran conflict, New Delhi raised gold import duty sharply from 6% to 15% and simultaneously encouraged consumers to moderate purchases. According to the report’s econometric analysis, the higher import duty alone is expected to reduce Indian jewellery, bar and coin demand by 50-60 tonnes, representing roughly a 10% annual decline.

Although the World Gold Council believes this policy shift has largely been reflected in current prices, it warns that a broader slowdown in India’s economy could further dampen consumer demand. Rising defaults in the country’s rapidly expanding gold-backed loan market could also increase recycled supply, creating additional pressure on prices.

Even so, the broader message remains constructive.

Rather than signalling the end of gold’s remarkable rally, the report argues that the market is entering a consolidation phase in which prices are broadly aligned with prevailing macroeconomic expectations. Under the base-case scenario, bullion is likely to trade within a narrow band around current levels. Yet the balance of risks still favours upside if geopolitical tensions escalate, inflation proves more persistent than expected or central banks shift towards easier monetary policy.

With structural demand from official institutions, Asian investors and long-term asset owners continuing to strengthen, gold appears increasingly insulated from the sharp corrections that characterised earlier market cycles. For investors navigating an uncertain global economy, the metal’s role as both a portfolio diversifier and strategic hedge remains firmly intact.

As the second half of 2026 unfolds, the next decisive move in gold may depend less on daily price swings than on how governments, central banks and global investors respond to an increasingly fragmented geopolitical and economic landscape. The World Gold Council’s assessment suggests that while volatility is likely to persist, the foundations supporting bullion remain considerably stronger than headline price movements alone would imply.

(Cover photo by Zlaťáky.cz on Unsplash)