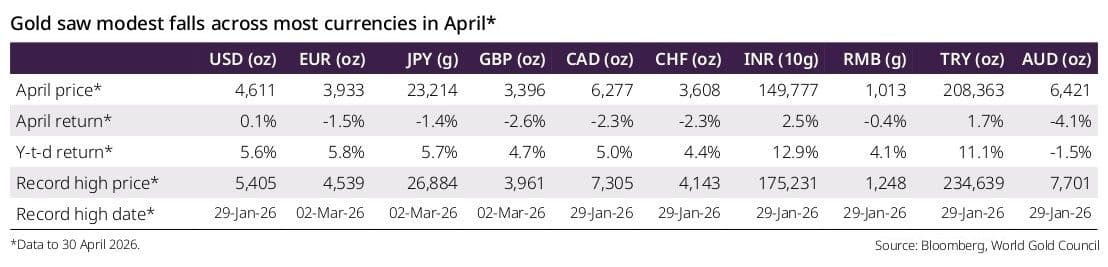

New Delhi: Global gold prices ended April largely unchanged as investors shifted back towards risk assets despite continuing geopolitical tensions in the Middle East. The metal closed at $4,611 an ounce (roughly Rs 12,350- Rs 12,400 per gram), with weaker performance across most major currencies as equity markets rebounded and volatility eased.

The latest Gold Market Commentary: The Return of Transitory, published by the World Gold Council, said markets were increasingly treating the Strait of Hormuz crisis as a temporary disruption rather than the beginning of a prolonged economic shock. That shift in sentiment reduced immediate safe-haven demand for bullion even as structural risks persisted.

“Markets appear to be treating the Middle East crisis and Hormuz shutdown as transitory, a word that carries baggage after 2021-22. The shock has been large, but markets are not extrapolating it into a meaningful shift in inflation or growth… yet. US near-term inflation breakeven rates (two-year) spiked as the crisis intensified, but have since retraced much of that rise. US equities have rallied strongly on a return of risk appetite; options markets appear relaxed too,” says the WGC report.

It noted that a sharp drop in market volatility weighed on gold during April. However, strong inflows into exchange-traded funds (ETFs), particularly from Europe, along with a weaker US dollar, prevented a steeper correction in bullion prices. European investors accounted for the bulk of ETF buying amid concerns that the region could face deeper economic fallout if disruptions in the Strait of Hormuz intensified.

Higher Rates, Stronger Equities Pressure Bullion

A key headwind for gold remains the changing interest rate outlook in the United States. Investors are increasingly pricing in a “higher-for-longer” Federal Reserve stance as economic resilience and stronger corporate earnings reduce expectations of aggressive rate cuts.

“Gold is technically vulnerable, but the long-term uptrend is not yet broken. March’s decline held key support near the 200-day average and $4,075/oz retracement level, but the rebound has stalled below the 55-day average. A renewed 200-day test looks likely; only a sustained break below $4,075/oz would confirm a more serious technical top,” says the report.

The report added that easing volatility premiums in both equity and bond markets had diminished gold’s immediate appeal as a defensive asset. At the same time, stronger earnings expectations for US companies strengthened the relative attractiveness of equities.

“Taken together, the near-term setup is not especially friendly. Gold is technically vulnerable, rate-cut expectations have moved out, and markets are treating the shock as temporary. Absent a fresh catalyst, this could remain a weak period for gold.”

Despite those pressures, gold has continued to outperform in some emerging market currencies. Prices in India rose 2.5% during April and are up 12.9% year-to-date, reflecting both currency weakness and persistent domestic investment demand.

Oil Risks, Stagflation Fears Keep Support Intact

While financial markets appear calm, the report warned that investors may be underestimating the longer-term inflationary consequences of prolonged energy supply disruptions. Oil futures continue to imply significantly higher prices through the end of the year, raising concerns over stagflation risks globally.

“But the calm could prove fragile. If the shock is less temporary than markets assume, gold could regain support quickly. On a global level, stagflation risks are edging up even if markets have faded the immediate inflation scare. Brent and WTI are pricing December contracts at a 22-25% premium compared to before the crisis,” says the report.

It cited estimates from J P Morgan suggesting that global oil inventories could hit operational floor levels by September if the Hormuz disruption remains unresolved. Such a scenario could trigger disorderly energy pricing and wider economic damage, conditions historically supportive for bullion.

The World Gold Council also highlighted the possibility of renewed financial market stress from leveraged Treasury trades and broader deleveraging risks. Gold futures positioning, however, remains relatively neutral, leaving room for investors to rebuild exposure if uncertainty intensifies again.

Structural Drivers Continue to Favour Gold

Beyond short-term market swings, the report maintained that several long-term drivers continue to support the gold market. Central bank purchases remain robust, debt burdens across advanced economies continue to rise and concerns around reserve diversification away from the US dollar persist.

“But the crisis has also reinforced many of the structural reasons investors own gold in the first place: inflation uncertainty, geopolitical risk, unreliable bond diversification, fiscal pressure and gradual reserve diversification. A catalyst - exogenous or perhaps via a weaker price – will be needed to re-establish the structurally supported uptrend,” says the report.

It argued that even modest diversification away from dollar-denominated reserves could have an outsized impact on gold demand over time. It also reiterated that bonds may no longer provide reliable diversification benefits during inflation-led shocks, reinforcing gold’s strategic role in institutional portfolios.

For now, bullion markets remain caught between easing short-term panic and mounting long-term macroeconomic risks. Investors appear willing to ignore geopolitical instability as long as growth and earnings remain resilient. But if inflation reaccelerates or energy markets tighten further, gold’s current pause could quickly turn into another powerful rally.