New Delhi: India’s gold consumption trend is taking a decisive turn, with investment demand increasingly overshadowing traditional jewellery buying.

CareEdge Ratings’ latest report, ‘From Ornament to Asset: Investment share in India’s Gold Consumption’, highlights a fundamental shift in how Indians perceive and consume gold now. According to the report, this transition reflects not merely cyclical price movements but a deeper structural change driven by macroeconomic uncertainties and evolving financial preferences.

Globally, gold demand surged about 8% year-on-year to nearly 5,000 metric tonnes in CY25, marking an all-time high. India, long regarded as a jewellery-dominated market, is now mirroring global trends as investment-led consumption gains traction. The report notes that rising geopolitical risks, persistent inflation concerns, and currency uncertainties have repositioned gold as a strategic financial asset rather than a discretionary purchase.

“Global gold demand reached an all-time high in CY25, rising ~8% y-o-y to ~5,000 metric tonnes (MT), driven primarily by robust investment demand despite sharply higher gold prices and macroeconomic headwinds. Central banks continued large-scale gold accumulation for the fourth consecutive year, underscoring gold’s role in reserve diversification amid geopolitical challenges. Composition of gold consumption globally has undergone a structural shift with jewellery’s share falling significantly to ~33% in CY25 — well below its long-term average of ~50% — as consumers responded to elevated prices by reducing discretionary jewellery purchases,” notes the report.

Investment Demand Surges in India

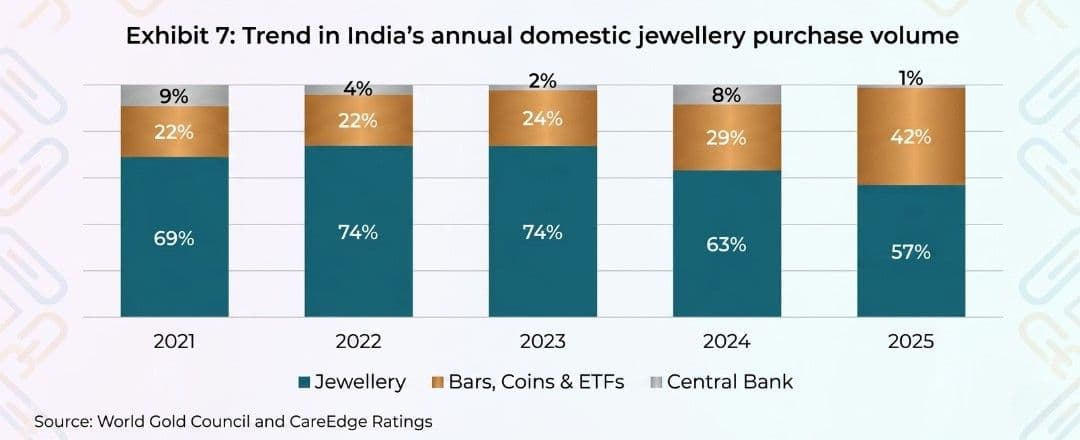

The most striking trend in India is the surge in investment demand, which has significantly altered the composition of gold consumption. Investment’s share rose sharply to 42% in CY25 from 29% a year earlier, signalling a behavioural shift among consumers who are increasingly treating gold as a hedge against uncertainty.

This transition has been fuelled by strong inflows into gold ETFs and rising bar-and-coin purchases, underscoring a growing preference for financialised gold. According to the report, this trend is unlikely to reverse soon, given the persistence of global volatility and the appeal of gold as a safe-haven asset.

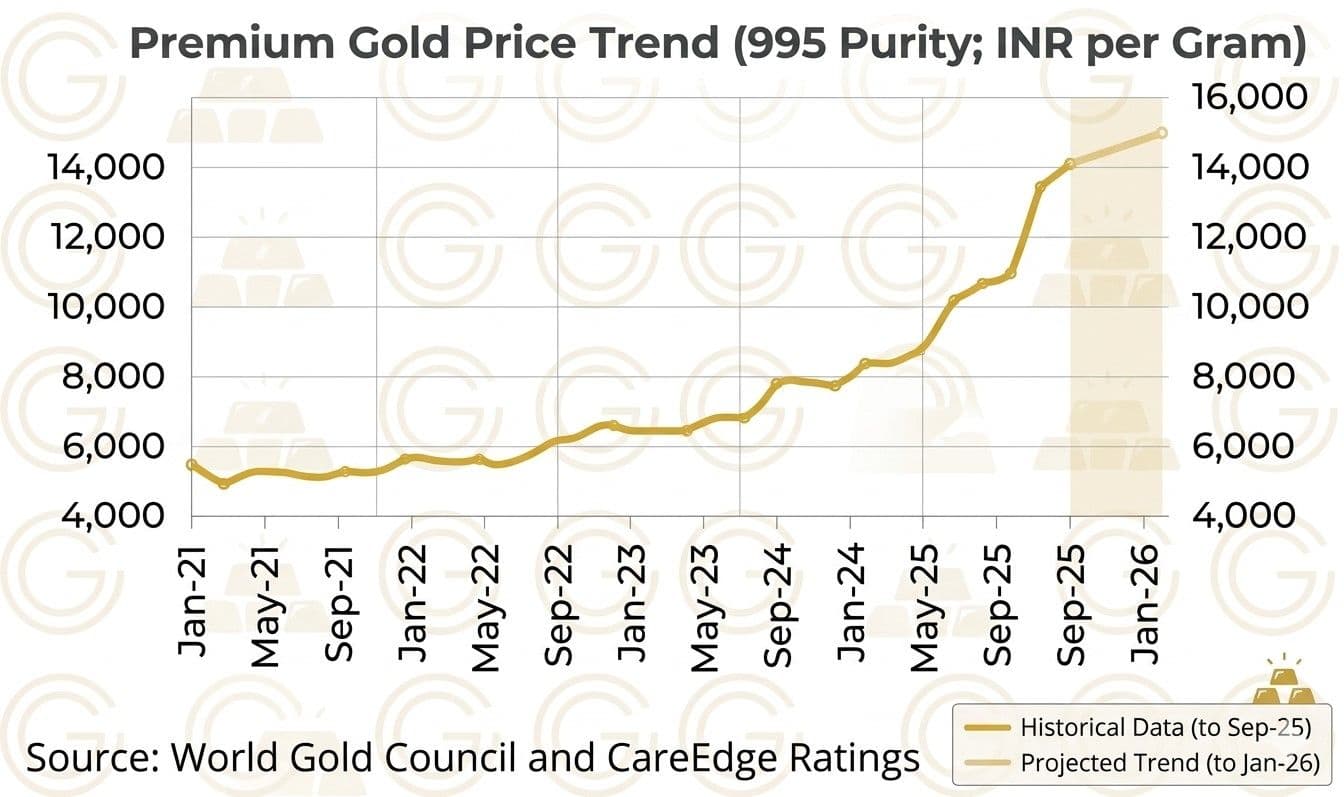

“Investment demand surged to record levels globally and in India led by gold ETFs and bar-and-coin buying, reflecting safe-haven demand, diversification motives and geopolitical uncertainty. Investment share in India’s gold consumption rises to 42% in CY25 from 29% in CY24. Gold prices have entered a more durable high-price regime supported not by short-term speculative flows but by structural demand shifts, sustained official sector buying and persistent global macroeconomic and geopolitical uncertainty,” says the report.

The report further indicates that Indian investors added 37.5 tonnes to gold ETFs in CY25 — more than the combined investment of the previous decade — highlighting the scale of this shift.

Jewellery Demand Holds Value, Loses Volume

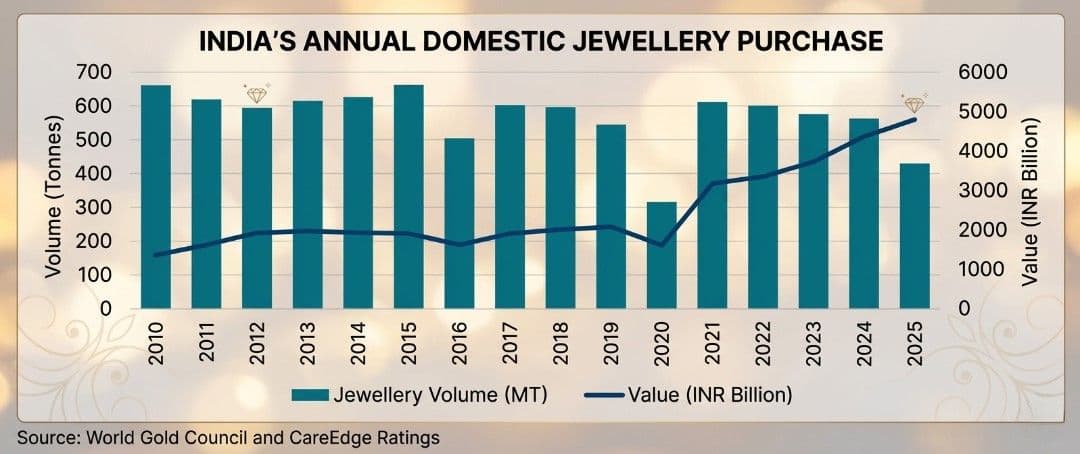

Despite the surge in investment demand, jewellery continues to hold cultural and economic relevance in India. However, the nature of demand is evolving. While overall spending on jewellery has remained robust, driven by weddings and festivals, volumes have declined sharply due to elevated prices.

Consumers are adapting by purchasing lighter and lower-carat jewellery, indicating price sensitivity without abandoning the asset altogether. This divergence between value and volume reflects a recalibration of consumption patterns rather than a collapse in demand.

“Indian jewellery demand remains resilient despite record gold prices with jewellery purchases rising ~10% y-o-y to Rs 4.8 lakh crore in CY25, reflecting consumers’ willingness to allocate higher wallet share to jewellery. Though on value basis demand remained resilient, volume has declined by 15% in CY25, which is reflective of the price-sensitive nature of jewellery demand, where preferences shifted towards lower-carat/lighter-weight jewellery,” according to the CareEdge Ratings report.

Over the longer term, jewellery’s share in India’s total gold consumption has dropped below 60%, compared to a historical average of around 70%, underscoring the scale of change underway.

“Gold consumption patterns are witnessing a structural shift, with jewellery accounting for less than 60% of India’s total gold purchases in CY25, compared to a long-term average of ~70%. Geopolitical uncertainty, momentum in gold prices and portfolio diversification preferences are expected to continue fuelling investment demand for gold, with its share in overall gold consumption is projected at 35-40% in FY27,” says the report.

Formalisation and Growth Momentum

The changing consumption pattern is also reshaping the business landscape for jewellers. Organised players are expected to benefit from rising formalisation, aggressive store expansion, and sustained consumer demand, even in a high-price environment.

The report projects strong revenue growth for branded jewellers, driven by market share gains and increased consumer trust in organised retail. At the same time, elevated gold prices are pushing up inventory requirements, leading to higher working capital needs across the sector.

Domestic organised jewellery retailers are expected to report revenue growth of over 35% year-on-year in FY26, driven by steady consumer appetite for jewellery despite rising gold prices, market-share gains from accelerated sector formalisation and planned store additions.

According to the report, “This momentum is likely to continue in FY27, with revenue growth projected at 20-25% year-on-year. Operating profit margin is also likely to expand by 180-200 bps in FY26 supported by inventory gains, which is likely to normalise to 6.5-7% in FY27 led by expectations of range-bound gold prices and front-loaded operating expenses on new stores.”

(Cover photo by Jingming Pan on Unsplash)