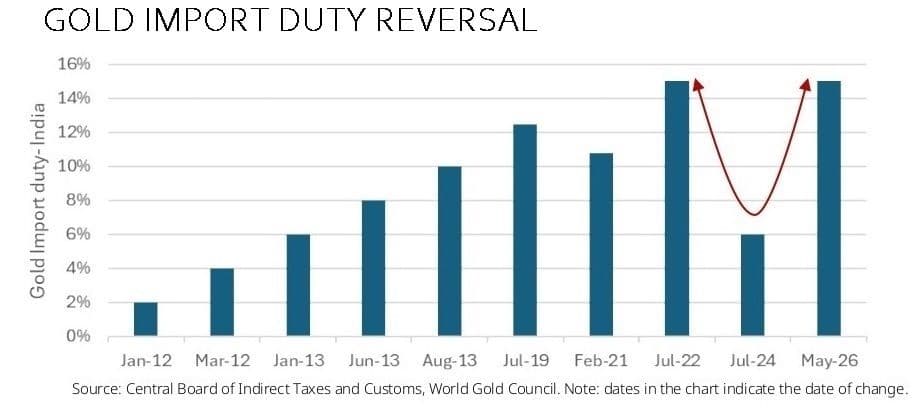

New Delhi: The Government of India’s sudden decision to raise gold import duty from 6% to 15% has sent shockwaves through the country’s bullion trade, triggering an immediate jump in domestic prices and raising concerns over demand destruction in the world’s second-largest consumer of the yellow metal.

The move, announced amid rising geopolitical uncertainty in West Asia and pressure on the rupee, effectively reverses the July 2024 duty cut and marks one of the sharpest policy pivots in recent years. The Weekly Markets Monitor of the World Gold Council notes that the government’s objective is to conserve foreign exchange reserves at a time when elevated crude oil prices and global inflation risks are widening external vulnerabilities.

“India sharply raised gold import duty from 6% to 15% last week – fully reversing the July 2024 cut – as a part of a broader push to conserve foreign exchange reserves amid geopolitical uncertainty and INR pressures,” says the report. “The move triggered an immediate rise in the local gold price, which are already up more than 60% y-on-y. The hike further squeezes affordability and could weigh on consumer demand.”

The timing is critical. Gold prices globally remain volatile, with investors reassessing inflation trajectories, US interest rates and geopolitical tensions. According to the report, gold suffered its worst weekly decline since March, falling 4.5% to $4,528 an ounce as rising US bond yields and a stronger dollar weighed on investor sentiment.

For India, however, the bigger issue is domestic affordability. With retail prices already at record highs, jewellers fear the latest duty increase could defer wedding and festive purchases, particularly in rural markets where discretionary spending remains under pressure.

Pressure Builds on Demand and Trade

The report indicates that weakening Indian demand may already be influencing global price behaviour. “Inflation fears, driven by higher oil prices, pushed US Treasury yields up, pressuring gold alongside a stronger dollar,” says the report. “Remaining weakness, captured in ‘residuals’, likely reflects a potential decline in Indian demand after recent policy and import duty changes.”

That observation is significant because India remains central to physical gold consumption trends. Any sustained slowdown in buying could alter global demand dynamics at a time when institutional investors are already trimming exposure in parts of Asia.

The report notes that Asian investors reduced futures longs and sold exchange-traded funds, even as North American investors continued to add ETF exposure. The divergence suggests that while Western investors still view gold as a hedge against geopolitical instability, Asian consumers are becoming increasingly sensitive to elevated prices.

India’s macroeconomic backdrop also complicates the outlook. The report says the country’s exports rose 14% year-on-year in April, led by electronics and petroleum products, but higher crude imports pushed the trade deficit to $28.4 billion. A higher gold import duty may therefore be less about bullion itself and more about reducing pressure on the current account.

Yet history suggests sharp tariff increases can produce unintended consequences. Past duty hikes triggered a surge in unofficial imports and smuggling networks, particularly across India’s western and eastern borders. Traders now fear the latest move could once again push part of the market underground, reducing transparency while hurting organised retailers.

Global Signals Turn Unfavourable

Beyond India, the broader global backdrop is also turning more difficult for bullion.

The report says rising US inflation and elevated energy prices are reinforcing expectations that interest rates may stay higher for longer. “Yields have re-emerged as a key driver of gold,” according to the report. “Persistently elevated geopolitical risks – as the US and Iran are still far from a deal – could keep inflation concerns high. Both may push yields higher and create near-term headwinds for gold.”

Technical indicators are also flashing caution signals. The report states that gold has “again seen a decisive rejection” of its 55-day moving average, while support near the 200-day average at around $4,342 an ounce is becoming increasingly important.

At the same time, US bond yields are testing the upper end of their three-year trading range. According to the report, a sustained rise beyond current levels could intensify pressure on bullion prices globally.

The dollar’s rebound is adding another layer of stress. The report says the DXY index has moved back above short-, medium- and long-term averages, increasing the risk of further gains in the US currency. Since gold is priced in dollars internationally, a stronger greenback generally reduces purchasing power for importing nations such as India.

The Market Ahead

The next phase for India’s gold market will depend on three variables: domestic demand resilience, the trajectory of global gold prices and the government’s tolerance for unofficial imports.

If international prices remain elevated while the rupee weakens further, Indian consumers could face an extended period of record-high retail prices. That may force households to reduce discretionary jewellery purchases or shift towards lighter products and recycled gold.

The report suggests the global environment is unlikely to offer immediate relief. US inflation remains sticky, oil prices are firm and central banks continue to monitor geopolitical risks closely.

For policymakers, the challenge will be balancing external account stability with the realities of India’s deep-rooted gold economy. While the higher duty may temporarily curb imports, sustained price pressure risks reviving parallel supply channels and weakening formal trade volumes.

India’s gold market has entered a more volatile and policy-sensitive phase, and the consequences are likely to extend well beyond bullion counters.

(Cover photo by Jingming Pan on Unsplash)