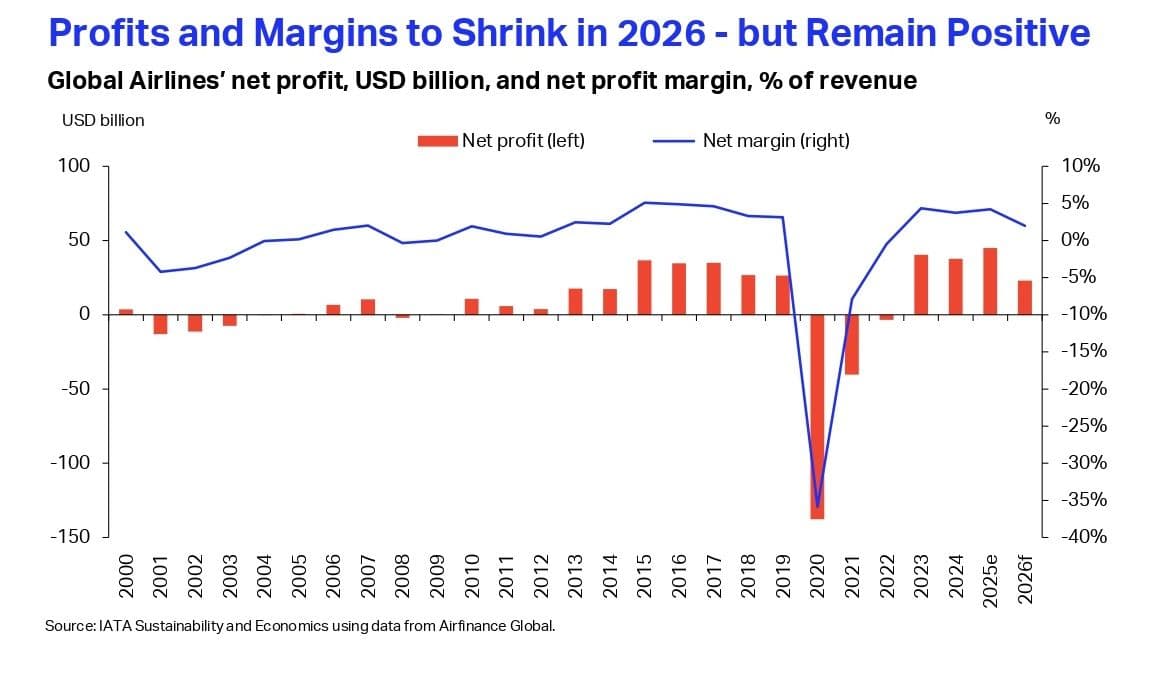

New Delhi: The global airline industry is heading for another year in the black despite an unprecedented surge in jet fuel prices and severe disruption across Middle Eastern air corridors. The sector’s ability to generate profits, however, has been sharply diminished, with airlines now expected to earn just $23 billion in 2026 — nearly half the earlier forecast of $45 billion — underlining how quickly geopolitical shocks can erase the industry’s already-thin margins, according to IATA’s latest forecasts.

The revised outlook points to total airline revenues of $1.17 trillion in 2026, translating into a net profit margin of merely 2%. The dramatic downgrade by IATA follows the outbreak of war involving the US and Iran, which has triggered a sharp spike in energy prices, disrupted key international flight routes and added fresh uncertainty to an industry that has historically struggled to generate sustainable returns.

The numbers reveal a sector that remains operationally agile but financially vulnerable. Airlines are expected to carry more than 5.1 billion passengers this year, supported by a 2.1% increase in global passenger traffic and record-high load factors of 84%. However, stronger traffic volumes are no longer translating into proportionately higher profits. According to IATA’s projections, the industry’s net earnings per departing passenger are expected to decline to just $4.5 in 2026, down from $9.1 a year earlier, highlighting the razor-thin economics of commercial aviation.

The biggest challenge confronting airlines is a sharp mismatch between rising revenues and even faster-growing costs. Industry revenues are expected to rise by around 9.5% in 2026, helped by improved passenger and cargo yields. However, overall expenses are forecast to jump 13.1%, wiping out much of the benefit from higher fares.

Fuel remains the largest source of financial pressure. The global airline fuel bill is expected to climb to $351 billion, pushing fuel’s share of total operating expenses to 31.4%. While some carriers have benefited from fuel-hedging strategies, the surge in oil prices following the Middle East conflict has significantly weakened the industry’s earnings outlook.

The energy shock is also expected to slow the broader global economy, creating a second layer of pressure on airlines. Global GDP growth is projected to ease by around half a percentage point to 2.5% in 2026, while inflation could accelerate to 5%, squeezing household purchasing power and potentially dampening discretionary spending on travel.

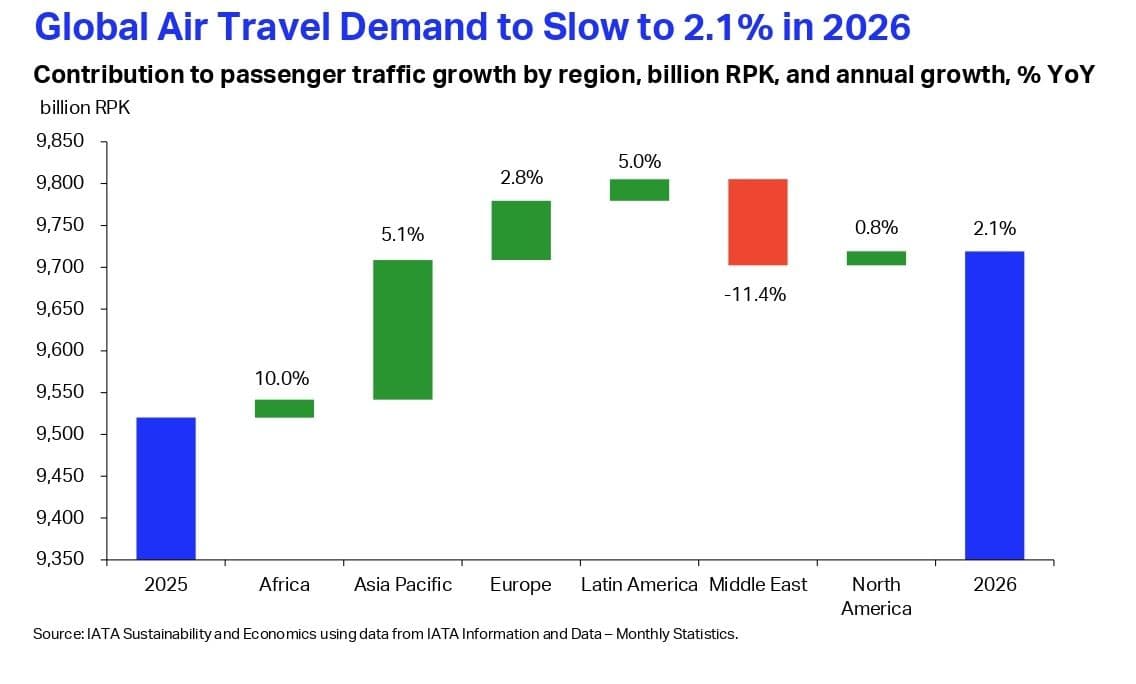

As a result, global air passenger demand is expected to expand at a much slower pace than the post-pandemic boom years, says IATA. Revenue passenger kilometres (RPK), the industry’s key measure of traffic demand, are forecast to grow just 2.1% year-on-year in 2026, it adds.

The impact of the Middle East conflict will be most severe within the region itself. Passenger traffic in the Middle East is expected to contract 11.4% as airspace restrictions, operational disruptions and the loss of transfer traffic weigh heavily on airlines.

Elsewhere, the picture is mixed. Africa is forecast to register the fastest growth at 10%, although from a relatively small traffic base. Asia-Pacific is expected to expand by 5.1% and will contribute more than half of global passenger growth, reinforcing its role as the aviation industry’s key engine of expansion.

European airlines are projected to see passenger traffic increase by 2.8%, partly benefiting from rerouted long-haul traffic displaced by Middle Eastern disruptions. The region is also witnessing a stronger shift towards leisure travel and visits to friends and relatives closer to home.

Latin America is expected to post 5% growth, supported by comparatively resilient economies, while North America is likely to record a modest 0.8% rise as a maturing market and a slowing US economy limit domestic travel growth.

Despite the sharp deterioration in earnings, the industry’s ability to remain profitable amid a war-driven energy crisis demonstrates its adaptability, says IATA. Its latest outlook, however, also exposes a deeper structural weakness: aviation remains one of the world’s most shock-sensitive industries, where even record passenger volumes and strong aircraft utilisation struggle to produce durable returns.

The sector has never achieved a net profit margin above 5%, leaving airlines with limited financial buffers to withstand the next geopolitical conflict, economic downturn or supply shock. The resilience of global aviation may once again be evident in 2026, but its long-term robustness remains a far more difficult challenge.

(Cover photo by Rocker Sta on Unsplash)