New Delhi: The global aviation industry has run into its first serious turbulence since the pandemic recovery, and the trigger lies squarely in geopolitics. Data released by the International Air Transport Association (IATA) for March reveals a sharp and unexpected slowdown in passenger demand, with the Middle East conflict delivering a severe systemic shock to global air traffic flows.

Total demand, measured in revenue passenger kilometres (RPK), rose just 2.1% year-on-year, a dramatic moderation from 6.1% growth in February and the weakest post-pandemic expansion. This slowdown came despite resilient demand elsewhere, underscoring the disproportionate impact of the war-driven collapse in Middle Eastern aviation. Industry-wide traffic reached 754 billion RPK, but the momentum has clearly faltered.

Capacity, measured in available seat kilometres (ASK), contracted 1.7%, reflecting a cautious supply response amid operational uncertainty. Yet, paradoxically, the global passenger load factor (PLF) rose to a record 83.6% for March, indicating that flights that did operate were fuller than ever.

At the heart of this disruption lies a collapse of unprecedented scale. Passenger traffic carried by Middle Eastern airlines plunged 58.6%, while international traffic from the region dropped 60.8%, driven by widespread airspace closures linked to the US-Israel-Iran conflict. The result has been not just a regional crisis, but a global reconfiguration of aviation flows.

Collapse of Global Hub System

The Middle East has long functioned as the world’s most critical aviation bridge, connecting Asia, Europe and Africa through high-capacity hub airports. The sudden contraction in this network has sent shockwaves across the global system.

International passenger traffic, which accounts for 62.8% of global demand, fell 0.6% year-on-year — the first decline since March 2021. This contraction occurred despite strong growth in every other region, highlighting how deeply the global system depends on Middle Eastern transit hubs.

Capacity on international routes fell even more sharply, down 6.2%, pushing load factors to a record 84.1%. But this apparent efficiency masks underlying stress: airlines are flying fewer routes with higher occupancy, rather than expanding networks.

The data shows that the Middle East’s disruption is not merely a regional downturn but a structural break. With capacity in the region down 54.7% and load factors falling 6.3 percentage points to 68.3%, the traditional hub-and-spoke model centered on Gulf carriers has effectively been partially dismantled, at least temporarily.

“Demand for air travel continued to grow in March despite disruptions in the Middle East. The nearly 61% decline in international traffic by carriers in the region restrained global growth to just 2.1%. Outside the Middle East, demand grew by around 8%, which underlines the underlying strength of the recovery,” said Willie Walsh, IATA Director General.

“However, what we are witnessing is not just a cyclical dip but a structural shock to global connectivity. The Middle East’s role as a transit hub has been severely impaired, forcing airlines worldwide to rethink route economics and network strategies. This is not easily reversible in the short term.”

The implications are far-reaching. Airlines in Europe, Asia Pacific and Africa are being forced to reroute flights, increase direct services, and absorb higher operational costs, all while navigating constrained airspace and volatile fuel markets.

The Great Traffic Diversion

Even as the Middle East faltered, other regions have stepped in to absorb displaced demand, creating a patchwork of winners and losers in global aviation.

Asia Pacific emerged as the strongest beneficiary, with passenger demand rising 11.5% and load factors reaching a record 87.2%. International routes in the region saw particularly strong gains, with load factors hitting an extraordinary 91.2%. Traffic between Europe and Asia surged 29.3%, as airlines bypassed Middle Eastern hubs and introduced more direct services.

European carriers posted a robust 7.5% increase in total traffic, while North American airlines grew more modestly at 2.3%. African airlines led global growth with a 20.6% surge, albeit from a smaller base, while Latin American carriers expanded 8.4%.

“The disruption has effectively rerouted global traffic flows. We are seeing unprecedented growth in direct long-haul routes, particularly between Europe and Asia, and between Asia and North America. Airlines are rapidly adapting, but this comes at a cost in terms of fuel burn, crew utilisation, and scheduling complexity,” Walsh noted.

“The beneficiaries are those regions with strong point-to-point demand and flexible fleet deployment strategies. Asia Pacific carriers, in particular, have capitalised on the situation, recording some of the highest load factors ever seen.”

At the route level, the shifts are even more striking. Traffic within Asia rose 12.3%, while the Asia-North America corridor expanded 12.2%. The Southwest Pacific-Asia route grew 21.1%, reflecting diverted ‘Kangaroo Route’ traffic. Meanwhile, the Middle East-Asia corridor collapsed by 55.9%, illustrating the scale of disruption.

Load factors on key routes such as Europe-Asia and Asia-North America exceeded 90%, indicating strong demand but also tight capacity. This suggests that while passengers are still flying, they are doing so on fewer, more crowded routes.

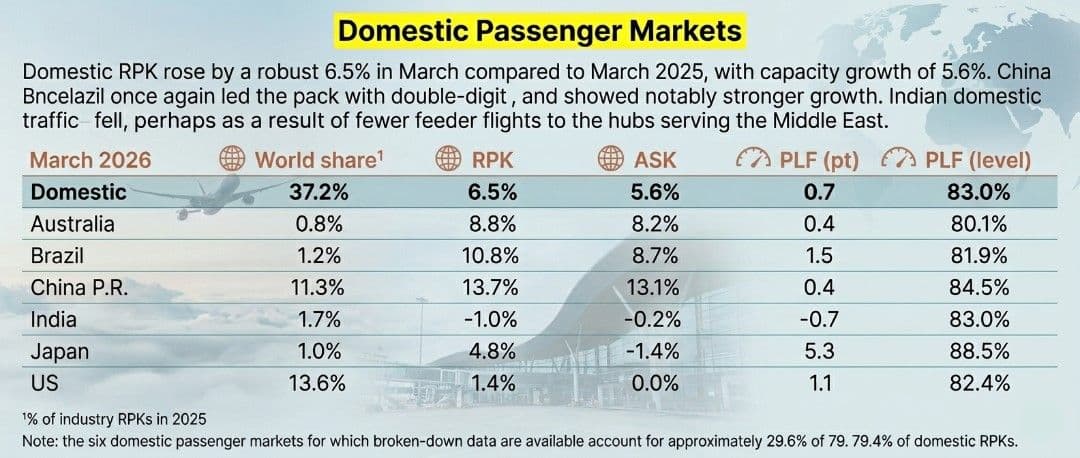

Domestic Resilience

Amid the international disruption, domestic markets have provided a crucial buffer for global aviation. Domestic passenger traffic grew 6.5% year-on-year, supported by strong performance in major markets such as China and Brazil.

China led the domestic recovery with a 13.7% surge in traffic, driven partly by extended Lunar New Year travel. Brazil followed with 10.8% growth, marking its fourth consecutive month of double-digit expansion. Australia and Japan also recorded solid gains, with Japan’s load factor jumping to 88.5%.

However, not all markets shared in this resilience. India stood out as the only major domestic market to contract, with traffic falling 1.0%. This decline reflects the country’s heavy reliance on Middle Eastern hubs for international connectivity, particularly for labour traffic to the Gulf.

“The domestic market has become the backbone of global aviation in the current environment. It is less exposed to geopolitical disruptions and provides airlines with a stable revenue base. However, markets that are structurally linked to international transit flows, such as India, are more vulnerable,” Walsh said.

“The decline in Indian domestic traffic is a clear example of how interconnected the global aviation system is. When international hubs are disrupted, the ripple effects are felt far beyond the immediate region.”

Looking ahead, the industry faces additional headwinds. Global scheduled seat capacity is expected to decline 0.7% in April, with Middle Eastern capacity projected to fall a staggering 38.4%. While a modest recovery is expected in May, with global capacity growth returning to around 2.0%, the Middle East will remain significantly constrained, with capacity still down 18.3%.

“Everybody’s watching what’s happening with jet fuel… both supply and pricing. On the supply side, we could see shortages in regions dependent on Gulf supplies, particularly Asia and Europe. At the same time, high fuel costs are feeding into ticket prices, and while demand has held up so far, there is a real question about how long that resilience can last,” Walsh warned.

“Airlines are being tested on multiple fronts — operational, financial, and strategic. Stabilising fuel supply and ensuring regulatory flexibility, especially around airport slots, will be critical in navigating the months ahead. The summer travel season looks strong, but the risks are clearly elevated.”

Fragile Recovery

The March 2026 data marks a turning point for global aviation. What had been a steady, broad-based recovery has been abruptly disrupted by geopolitical conflict, exposing the industry’s deep structural dependencies.

While demand remains fundamentally strong — growing 8% outside the Middle East — the system is under strain. Capacity constraints, rerouted traffic, rising costs, and regional imbalances are reshaping the aviation landscape in real time.

The collapse of Middle Eastern traffic is not just a regional crisis, it’s a global shock that has revealed the fragility of interconnected networks. As airlines adapt, the industry is entering a new phase. One, defined less by recovery and more by resilience.

The skies remain busy, but the routes have changed. And so has the risk calculus.

(Cover photo by Omar Prestwich on Unsplash)