New Delhi: The global economy, which had only just regained its footing after successive shocks, now faces a renewed and potentially destabilising threat. The World Economic Outlook (WEO) report released by the International Monetary Fund has sounded a stark warning: the outbreak of war in West Asia has interrupted a fragile recovery and injected fresh uncertainty into an already volatile global economic landscape.

In its assessment, the IMF notes that the global economy had been navigating multiple headwinds over the past year, including higher trade barriers and persistent uncertainty. Yet these were partially offset by strong tailwinds, notably a surge in technology-related investments, accommodative financial conditions supported by a weaker US dollar, and continued fiscal and monetary policy support across major economies. The war has now emerged as a powerful counterforce, threatening to undo these gains.

The IMF report introduces a “reference forecast” rather than a conventional baseline, reflecting the unusually fluid and uncertain situation. This forecast assumes that the conflict will remain limited in duration, intensity and geographical spread, with disruptions easing by mid-2026 in line with commodity futures as of March 10. Even under this relatively optimistic assumption, the global growth outlook has dimmed.

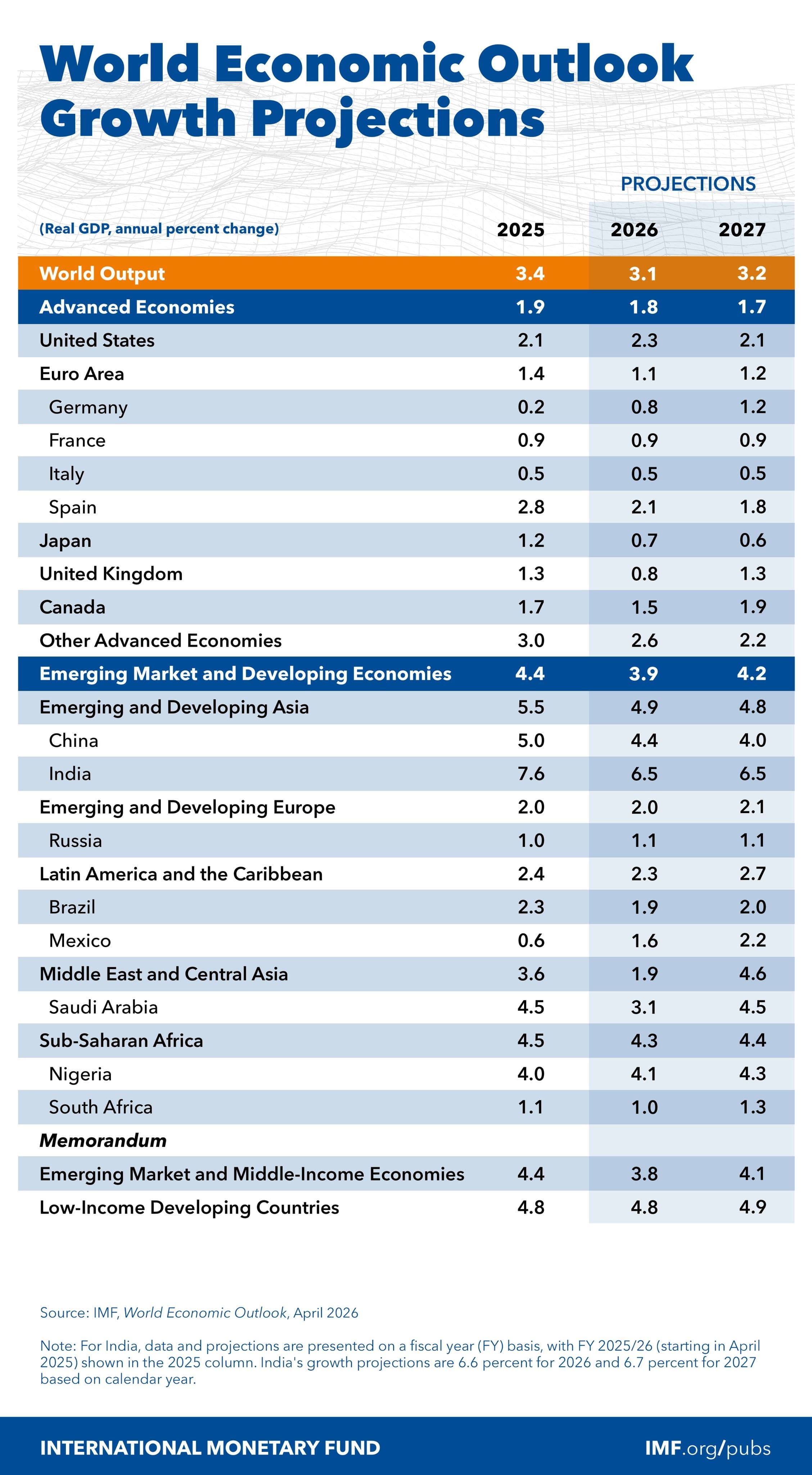

The IMF projects global growth at 3.1% in 2026 and 3.2% in 2027, a noticeable slowdown from the 3.4% recorded during 2024-25 and well below the historical average of 3.7% seen between 2000 and 2019. The 2026 forecast has been revised downward by 0.2 percentage points compared to the January 2026 update, while the 2027 projection remains unchanged.

Absent the war, the trajectory would have been markedly different. Pre-conflict projections indicated a potential upward revision of global growth to 3.4% for 2026, reflecting resilient economic momentum. The current downgrade, therefore, is largely attributable to disruptions stemming from the West Asia conflict, even as some mitigating factors — such as strong recent economic data and reduced tariff rates — offer limited offset.

Inflation, too, is expected to rise. Global headline inflation is projected to increase to 4.4% in 2026 before easing to 3.7% in 2027. Both figures represent upward revisions, underscoring the inflationary pressures unleashed by the conflict, particularly through energy and commodity markets.

IMF Chief Economist Pierre-Olivier Gourinchas outlined the fund’s assessment, saying, “The global economy was on a steady growth trajectory — around 3.3% in recent years — and we were looking to upgrade our projections. The war has stopped that momentum and we now project growth of 3.1% this year, under our reference forecast, with inflation rising to 4.4%, a sharp departure from the previous trend. The economic impact will depend on the duration and scale of the conflict and could be worse under our adverse and severe scenarios.”

“It (impact) will be highly uneven across countries, hitting countries in the conflict region, commodity-importing low-income countries, and emerging market economies hardest, through three channels: first, higher energy and food prices themselves; second, persistence in wage and price inflation; and third, a confidence shock that tightens financial conditions,” he predicted.

At the heart of the economic disruption lies a severe energy shock triggered by the conflict. The war has significantly disrupted oil and gas production and transportation, particularly through the Strait of Hormuz, the critical artery for global energy supplies. The near-closure of this strategic passage has sent energy prices soaring and constrained exports from some of the world’s largest producers.

The IMF report sharply revises down growth forecasts for West Asia and North Africa, projecting regional growth at just 1.1% in 2026, a dramatic fall from the 3.9% forecast in January. This marks a steep slowdown from the 3.2% growth recorded in 2025.

The economic toll is particularly severe for countries directly affected by the conflict. Iran’s economy is expected to contract by 6.1% in 2026, a downward revision of 7.2 percentage points. Qatar faces an even sharper contraction of 8.6%, reflecting extensive damage to its liquefied natural gas infrastructure, including the Ras Laffan facility, the world’s largest LNG processing site. Iraq’s economy is projected to shrink by 6.8%.

Other Gulf economies are also experiencing significant stress. Bahrain and Kuwait, heavily dependent on the Strait of Hormuz and directly targeted during the conflict, are expected to contract by 0.5% and 0.6%, respectively, reversing growth rates of over 3% in the previous year.

In contrast, countries with alternative export routes are somewhat better positioned. Saudi Arabia, supported by its East-West pipeline to the Red Sea, is projected to grow by 3.1%, albeit 1.4 percentage points lower than earlier estimates. The United Arab Emirates, which also has pipeline infrastructure bypassing Hormuz, is expected to grow by 3.1%, down from 5.8% in 2025.

The severity of the economic impact depends on multiple factors, including the extent of damage to energy infrastructure, reliance on the Strait of Hormuz, and the availability of alternative export routes. Import-dependent economies are also under strain due to rising energy and commodity prices. Egypt, for instance, has seen its growth forecast cut by 0.5 percentage points to 4.2%.

The IMF underscores that while a rebound is expected in 2027, contingent on the normalisation of energy production and transport, this assumption remains highly uncertain. Any prolongation or escalation of the conflict could significantly alter the recovery trajectory.

Beyond regional disruptions, the conflict poses systemic risks to the global economy. The IMF report warns that under a worst-case scenario, characterised by sustained spikes in oil, gas and food prices, global growth could fall below 2% in 2026. Such an outcome would bring the world perilously close to a recession, a phenomenon witnessed only four times since 1980, most recently during the COVID-19 pandemic.

In this adverse scenario, oil prices could average $110 per barrel in 2026 and rise further to $125 in 2027. Inflation could surge to around 6%, forcing central banks to tighten monetary policy through higher interest rates, thereby further dampening economic activity.

Even under less extreme conditions, the impact of the conflict is expected to be highly uneven across countries. Emerging market and developing economies, particularly those that are commodity importers or already burdened with structural vulnerabilities, are likely to bear the brunt of the shock. The growth forecast for these economies has been revised downward by 0.3 percentage points for 2026, while projections for advanced economies remain broadly unchanged.

The transmission channels of the shock are multifaceted. Higher energy and food prices directly raise costs for households and businesses. Persistent inflation can lead to wage-price spirals, entrenching inflationary expectations. At the same time, heightened uncertainty and geopolitical tensions can trigger a loss of confidence, tightening financial conditions and reducing investment.

The report also highlights additional downside risks. Geopolitical tensions could escalate further, potentially triggering the largest energy crisis in modern history. Trade disputes may intensify, particularly around critical resources such as rare earth elements, which play a vital role in global supply chains. A reassessment of profitability in emerging technologies like artificial intelligence could dampen investment and lead to financial market corrections.

Fiscal vulnerabilities add another layer of risk. Rising public debt and eroded fiscal buffers could push up long-term interest rates, further tightening financial conditions. Institutional erosion, including diminished central bank independence, could undermine monetary policy credibility and destabilise inflation expectations.

Policy Imperatives

The IMF report calls for a comprehensive and coordinated policy response. At the core of this response is the need to preserve price and financial stability while safeguarding fiscal sustainability.

“Central banks need to communicate clearly their readiness to act if needed. However, if the conflict is short-lived and inflation expectations remain well-anchored, they can afford to wait and assess. With very little room left, fiscal policy must act prudently,” said Gourinchas.

Fiscal policy must strike a delicate balance. Targeted, timely, and temporary support should be provided to protect vulnerable populations from the impact of rising prices. However, such measures must be financed within existing budget constraints or accompanied by credible plans for fiscal consolidation. Governments are encouraged to mobilise revenues, improve spending efficiency, and prudently manage windfall gains to rebuild fiscal buffers.

Financial regulators are advised to strengthen oversight, conduct rigorous stress testing, and ensure adequate capital and liquidity buffers within the banking system. In cases of excessive exchange rate volatility, temporary interventions may be warranted, provided they are aligned with broader macroeconomic policies.

Beyond immediate stabilisation measures, the report emphasises the importance of addressing structural imbalances. Domestic reforms aimed at enhancing productivity, improving resource allocation, and reducing distortions can simultaneously support growth and reduce external imbalances. Trade restrictions, the report cautions, are unlikely to resolve these imbalances and may, in fact, exacerbate them.

International cooperation emerges as a key theme. In an increasingly fragmented global landscape, coordinated efforts are essential to restore stability in trade and financial systems. Predictable and transparent policy frameworks can help rebuild confidence and support economic integration.

The report also notes that increased defence spending, while potentially boosting short-term economic activity, carries significant risks. It can fuel inflation, strain fiscal balances, and crowd out essential social spending, potentially leading to social unrest.

The report also points to a potential upside scenario. Accelerated investment in AI and technological innovation could, if effectively harnessed, drive productivity gains and support long-term growth. However, this will require complementary policies to foster business dynamism and ensure inclusive growth.

“Risks are firmly to the downside, including a further escalation of the war, new trade tensions or a re-assessment of the profitability of AI investments. On the other hand, a swift resolution of the war, productivity gains from a faster adoption of AI or easing in trade tensions could uplift the global economy,” suggested Gourinchas.

As the global economy navigates this turbulent phase, whether the current shock proves to be a temporary setback or a more enduring disruption will depend not only on the course of the conflict but also on the resilience and adaptability of policymakers worldwide.