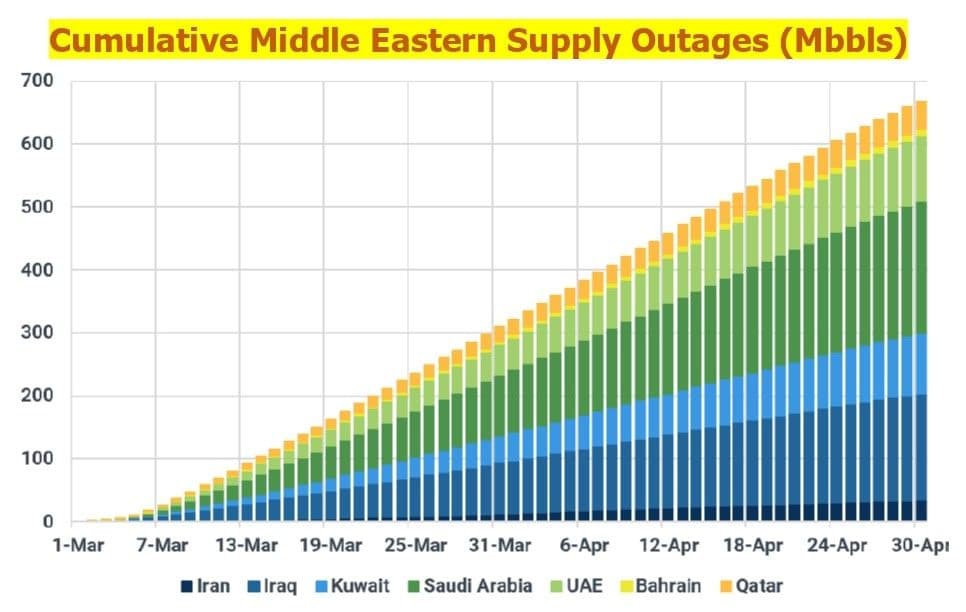

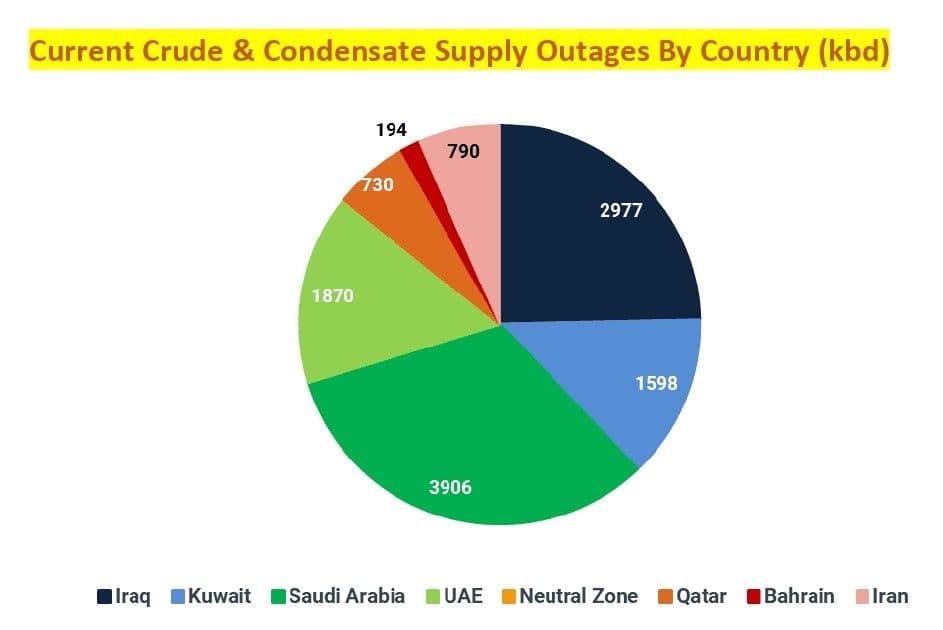

New Delhi: The global oil market is confronting a dual reality: acute short-term supply disruptions in West Asia alongside an urgent scramble for new long-term reserves. The latest data underscores how rapidly the geopolitical situation is tightening supply. According to a recent report by Kpler, cumulative crude and condensate supply losses in the Middle East surged to 430 million barrels as of April 10, reflecting what analysts describe as a severe and accelerating disruption cycle.

The Strait of Hormuz — one of the world’s most critical oil transit chokepoints — has seen only a handful of liquid tankers pass through in recent days, some carrying Iranian crude. This contraction in flows highlights the growing fragility of supply chains amid escalating regional tensions and ongoing attacks on oil infrastructure.

The scale of disruption is significant. “We estimate that Middle Eastern crude supply declined by an average of 9 Mbd in March compared to February levels, with a significant portion of the drop driven by Saudi Arabia, where crude output is currently hovering at only 6 Mbd, down from 10.1 Mbd in February,” Kpler said in its report. The sharp contraction reflects both physical damage to infrastructure and logistical bottlenecks that continue to ripple across export routes.

Saudi Arabia remains at the epicentre of the disruption. Output has been revised down to an average of 7 Mbd in March, with current levels closer to 6 Mbd after attacks reportedly cut production capacity by 600 kbd. Export volatility has followed. Loadings from Yanbu have fluctuated sharply, with a 10-day moving average dropping from 4.7-4.8 Mbd in late March to around 4.1 Mbd in early April, before partially recovering to 4.5 Mbd. Temporary spikes above 6 Mbd — including peaks of 7 Mbd on April 1 and April 5 — appear to reflect cargo timing distortions rather than sustainable capacity, given the terminal’s estimated limit of 5-5.5 Mbd.

Iraq has offered only limited relief, says Kpler. While crude supply exceeded expectations at 1.55 Mbd in March, supported by elevated domestic crude runs and crude burning, production has since slipped to around 1.3 Mbd.

The broader regional picture remains one of tightening supply under sustained geopolitical pressure, notes the Kpler report.

Structural Gap: Why Exploration Is Back

Even as markets grapple with immediate supply shocks, the industry faces a deeper structural imbalance. The upstream sector is staring at a looming supply gap that cannot be bridged by existing assets alone. A peer group of 30 of the world’s largest exploration and production companies is expected to see production declines averaging nearly 40% between 2025 and 2040.

The implications are profound. Today’s onstream fields are projected to fall short by 300 billion barrels of the nearly 1,000 billion barrels required to meet cumulative demand through 2050 under a base-case scenario, absent reserve upgrades. Exploration, long deprioritised during the energy transition push, is once again central to the industry’s strategy.

The value proposition is compelling. “Our analysis shows that the industry created $54 billion of value after deducting $97 billion of spend on exploration from 2021 to 2025, using a long-term Brent price of $65/bbl (real). At $85/bbl Brent, value creation more than doubles to $120 billion,” said Simon Flowers, Chairman and Chief Economist at Wood Mackenzie.

Recent discoveries are reinforcing that case. Companies have tended to underestimate early valuations, only to revise them sharply higher as more data becomes available. “As more information has come to light, we’ve just doubled our initial $2.8 billion development valuation (ex-E&A spend) to $5.7 billion for BP’s (100% equity) giant Bumerangue oil, gas and condensate find in Brazil, announced in August 2025. That on its own lifts industry value creation in 2025 to over $10 billion, in line with the industry’s five-year average,” Flowers noted.

Big Oil’s High-Stakes Frontier Push

The resurgence in exploration is being led by a narrow cohort of players with the capital, technical expertise and risk appetite to operate in increasingly complex environments. High-impact exploration is now concentrated in ultra-deep water frontier plays, often in water depths exceeding 1,500 metres.

The field of operators is limited. The seven major international oil companies dominate, alongside a handful of national oil companies such as Petrobras, Petronas and Türkiye’s TPAO. Independents including Murphy, Apache and Woodside participate but at a smaller scale, drilling fewer wells.

What distinguishes the current cycle is a growing willingness among operators to take large equity stakes in frontier projects to maximise upside. This strategy is exemplified by BP’s full ownership of the Bumerangue discovery and Eni’s initial 100% stake in Egypt’s Zohr gas field.

At the same time, new capital structures are emerging. National players such as QatarEnergy are increasingly active as non-operating partners, backing exploration campaigns across Brazil, Namibia, Cyprus and the Republic of the Congo. This hybrid model is helping spread risk while sustaining capital flows into high-cost, high-reward ventures.

Despite cost pressures — including a near doubling of rig day rates — exploration spending has remained resilient. Industry investment averaged $19 billion across 633 wells between 2021 and 2025. A dip to $16 billion and 388 wells in 2025 is viewed as temporary. “In our view, the dip to $16 billion on 388 wells in 2025 is an aberration. The resilience of investment reflects the long-term nature of the sharp end of the upstream value chain,” Flowers said.

Frontier Risks & the Road Ahead

The renewed push into frontier exploration is not without setbacks. The early months of 2026 have been sobering, with the first four high-profile wells all coming up dry, a reminder of the inherent risks in high-impact exploration. “…that’s the game, and players know the risks,” notes Flowers.

Yet the pipeline remains active. Among the 23 wells identified as key prospects this year, several stand out for their scale and strategic significance. Petrobras is drilling Morpho, an 800-mmboe potential play-opener in Brazil’s Foz do Amazonas basin. Greenland’s eastern coast is being tested through the OPW1 and OPW6 licences, targeting 800 mmboe and 338 mmboe respectively. Equinor’s S-M-1378-1 well in Brazil’s Santos Basin aims to replicate the success of pre-salt microbial carbonate plays, while Murphy’s Bubale-1 prospect in Côte d’Ivoire targets 440 mmboe.

These efforts underscore a broader industry recalibration. In the short term, geopolitical instability in West Asia — marked by infrastructure attacks, constrained tanker flows and volatile production — continues to tighten global supply and inject uncertainty into pricing. In the long term, the industry is being forced into a high-risk, high-reward exploration cycle to secure future volumes.

The convergence of these dynamics is reshaping the global energy landscape. Supply shocks are no longer isolated events but catalysts accelerating structural change, pushing companies to balance immediate resilience with long-term resource capture.

(Cover photo by Bob Milliar on Unsplash)