New Delhi: India is set to lose some momentum in FY27 as rising energy costs, a weaker monsoon and slowing global growth combine to weigh on economic activity, according to S&P Global Ratings.

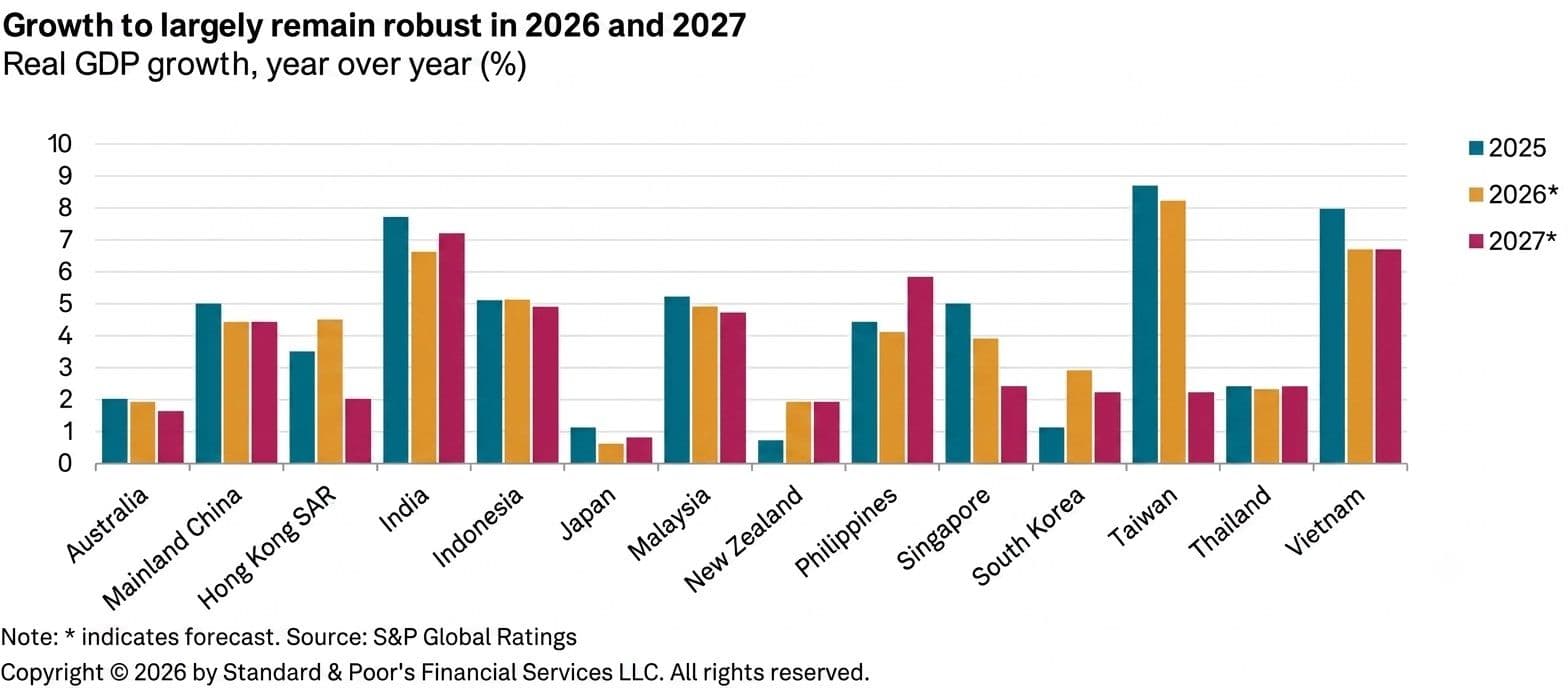

In its report, Economic Outlook Asia-Pacific Q3 2026: AI-Exposed Markets To Outperform, released on Wednesday, S&P Global Ratings projected India’s real GDP growth to slow to 6.6% in the financial year ending March 2027, down from 7.7% in FY26. While the forecast remains among the strongest in the world, it underscores the growing impact of external shocks on one of the fastest-growing major economies.

“We project real GDP growth will slow to 6.6% in the fiscal year ending in March 2027, compared with 7.7% in fiscal 2026, amid the energy stress, expectations of a sub-par monsoon, and slowing global growth,” the report said.

The downgrade comes as Asia-Pacific economies grapple with a volatile energy landscape triggered by tensions in West Asia. Although an interim peace deal between the US and Iran has helped cool crude prices from recent highs, S&P believes the economic effects of the energy shock are far from over.

“The global economy seems to have persevered in the face of the Middle East conflict and resulting energy stress. Hard and soft activity indicators in most major economies have broadly held up so far,” the report noted. Yet it added that the strain is increasingly visible through higher industrial input costs, longer supplier delivery times and surging fertiliser prices that are beginning to feed into food inflation.

For India, the challenge is compounded by weather risks. The India Meteorological Department has forecast rainfall at 90% of the long-period average in 2026 because of El Niño conditions, raising concerns over agricultural output, rural incomes and food prices.

S&P warned that the broader energy shock is filtering through the economy in multiple ways. Across Asia-Pacific, higher fuel and energy costs are eroding household purchasing power, increasing production expenses and tightening financial conditions. Most economies in the region remain heavily dependent on Middle Eastern energy supplies, making them vulnerable to prolonged disruptions.

“Higher global energy prices filter through to consumers via increases in production costs of other products and services. The increase in energy prices generally erodes purchasing power and depresses domestic demand,” the report said.

The ratings agency expects global oil prices to remain elevated over the coming months before gradually easing and returning to pre-crisis levels only in early 2028. Its baseline forecast assumes disruptions around the Strait of Hormuz ease during the second half of the year. However, S&P cautioned that risks remain significant.

In a downside scenario where Middle Eastern energy supplies remain constrained for longer and shipping through the Strait of Hormuz stays restricted through most of 2026, average oil prices could be 20% higher than its baseline projection. Under such a scenario, India’s inflation and growth outlook would deteriorate further.

“The economic outlook for the Asia-Pacific would be significantly less favourable than our baseline forecast,” S&P said. It estimated that consumer inflation in India, China and Japan would be 0.5-0.6 percentage points higher in the third quarter of 2026, while GDP growth could be 1.0-1.3 percentage points lower during the same period.

Inflation is already expected to accelerate in India as companies pass on higher energy costs to consumers and fuel price increases work their way through the economy. “We project consumer inflation will rise to 5.1% this fiscal year as manufacturers pass on higher energy costs to consumers, alongside recent increases in administered prices such as for petrol, diesel, and cooking gas,” the report said.

The projected inflation surge marks a sharp jump from the roughly 2% average retail inflation recorded in FY26. S&P expects the Reserve Bank of India to respond with a 25-basis-point repo rate increase in the second half of FY27, signalling that policymakers may need to prioritise price stability over growth support.

Even so, India’s macroeconomic position remains relatively resilient. S&P noted that measures by the government and the RBI to encourage foreign capital inflows have helped stabilise the rupee despite rising energy import bills and a widening current account deficit.

The ratings agency expects the rupee to average ₹93.5 against the dollar during FY27, stronger than its current levels.

India’s outlook also contrasts with developments elsewhere in Asia. While economies such as Taiwan, South Korea and Vietnam are benefiting from a powerful AI-driven technology export boom, India is among the countries where the drag from higher energy costs outweighs the gains from the global technology cycle.

“This contrasts with the downward revision to growth forecasts we have made since end-2025 for India, Japan, New Zealand and the Philippines, where the impact of the energy stress dominates,” the report said.

Despite the near-term slowdown, S&P remains optimistic about India’s medium-term trajectory, forecasting growth to rebound to 7.2% in FY28 before moderating slightly to 7% in FY29.