New Delhi: The rupee’s relentless fall is no longer a routine currency adjustment. With the domestic unit inching dangerously close to the Rs 97/$ mark, concerns are now shifting from volatility to structural weakness. What was initially dismissed as a temporary reaction to geopolitical tensions has evolved into a sustained depreciation cycle, raising serious questions about India’s external stability, imported inflation risks and the Reserve Bank of India’s ability to defend the currency without rapidly depleting reserves.

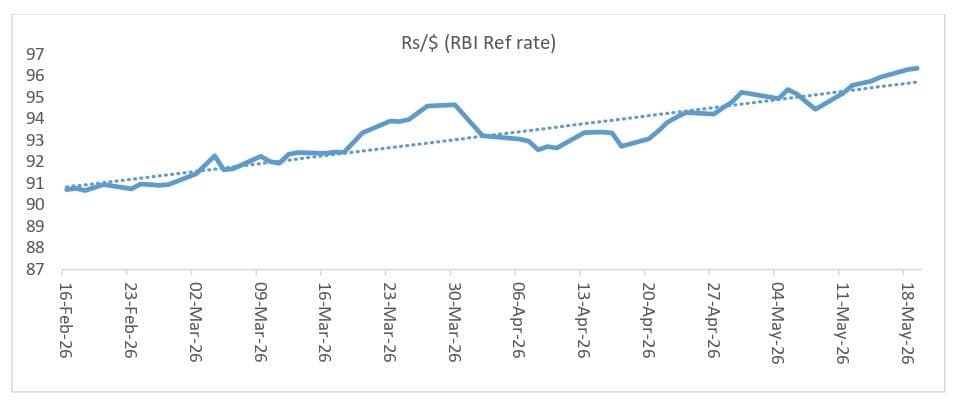

The pace of decline has been particularly striking. The rupee moved from the Rs 90-91/$ range in mid-February to the Rs 96-97/$ band by mid-May, reflecting what appears to be a calibrated but persistent weakening.

According to the report, What has driven the rupee of late?, published by Bank of Baroda’s Economics Research Department, the movement has unfolded almost one rupee at a time, with each higher trading band stabilising briefly before the next leg of depreciation began. “It does seem that the currency is being tested at one rupee at a time i.e. the level of 94 followed by 95 and 96 and 97 and so on. Once these levels are reached, turning around does not seem to be the route adapted.”

That observation captures the market mood succinctly. Currency traders increasingly believe the rupee is being managed through gradual depreciation rather than sharp intervention. The report notes that the annualised average daily volatility stood at 6.7%, but the broader trend remained unmistakably downward.

The concern is not merely about optics. A falling rupee directly raises India’s import bill, especially for crude oil, fertilisers and electronics. It also intensifies inflationary pressures at a time when domestic demand remains uneven and global uncertainty is elevated.

Oil & Outflows

The report identifies three principal drivers behind the rupee’s weakness — foreign portfolio investor flows, crude oil prices and geopolitical uncertainty linked to the ongoing West Asia war situation.

Interestingly, the dollar index, often seen as a dominant global currency indicator, did not emerge as statistically significant in the regression analysis conducted by the economists. “Theoretically the factors that have been driving the rupee are: changes in fundamentals which covers inflows and outflows of dollars, oil price movements, announcement effects of war affecting crude price and currency, and dollar index movements on daily basis,” according to the report.

However, the findings suggest India’s currency troubles are now being shaped more by domestic vulnerabilities and energy dependence than by broad-based dollar strength alone.

The sharp rise in crude prices has emerged as a particularly damaging factor. Brent crude hovering around $110 per barrel has amplified pressure on India’s trade deficit, forcing higher dollar demand from oil importers. “These results show that the change in crude oil price has a direct impact on the currency which will be a sentiment factor as this works through the trade bill when imports increase. Yet the psychological effect is sharp,” note the BoB economists.

That “psychological effect” may now be becoming self-fulfilling. Importers are front-loading dollar purchases fearing further rupee weakness, while exporters are delaying conversions in anticipation of better rates. Such behaviour typically accelerates currency depreciation.

Foreign institutional flows have also produced mixed signals. While same-day FPI inflows paradoxically appeared linked to rupee depreciation in the study, lagged flows behaved as conventional theory predicts.

“Inflows tend to make the rupee appreciate and outflows make rupee depreciate, which is in accordance with conventional wisdom,” says the BoB report.

The contradiction, according to the report, could stem from settlement timing mismatches in the market. Yet the broader takeaway remains clear — India’s currency remains highly vulnerable to volatile global capital movements.

RBI Running Thin

The more uncomfortable question now concerns the RBI’s intervention strategy and the sustainability of reserve deployment, the report stresses. India’s foreign currency assets, excluding gold, fell from $573.1 billion on February 27 to $552.8 billion by May 8, reflecting substantial central bank intervention to cushion the rupee’s decline.

The report says the first major reserve drawdown occurred immediately after the outbreak of war-related tensions, when the RBI aggressively sold dollars to stabilise the market.

“This was the first week of the shock which was cushioned by RBI selling dollars as well as revaluation of other forex assets in non-dollar currencies,” according to the report.

While India still possesses sizeable forex reserves by historical standards, the speed of depletion matters. Persistent intervention without a corresponding improvement in external balances can eventually weaken market confidence further. Currency markets often test central banks most aggressively when reserve defence appears prolonged and reactive.

The BoB report also offers a warning that policymakers may find difficult to ignore. “The market will be testing the Rs 97/$ level in the absence of any positive development on the war front. Going by the 5 session observation, it may not be too long before this level of Rs 97 is crossed.”

That prediction reflects a broader anxiety now gripping financial markets — that the rupee’s decline is no longer cyclical but increasingly structural. India’s dependence on imported energy, elevated global uncertainty, narrowing interest rate differentials and fragile foreign inflows are combining into a difficult macroeconomic mix.

For policymakers, the challenge is becoming sharper by the day. Allowing the rupee to weaken too rapidly risks imported inflation and investor anxiety. Defending it too aggressively risks exhausting reserves and tightening domestic liquidity. The balancing act is becoming narrower.

What is clear, however, is that the falling rupee is no longer just a currency story. It is rapidly turning into a referendum on India’s economic resilience in an increasingly unstable global order.