New Delhi: India’s startup and private equity ecosystem is undergoing a structural reset as investors pivot from growth-at-all-costs strategies toward profitability, operational discipline and sustainable cash generation. Mega funding rounds are becoming rarer, exit routes are evolving and capital is increasingly flowing into sectors and startups with clearer earnings visibility and resilient domestic demand drivers.

The change reflects a broader recalibration underway across India’s private capital markets after years of abundant liquidity and aggressive valuations. Investors are now prioritising governance standards, scalable business models and operational efficiency as global uncertainty, slower IPO markets and tighter liquidity conditions reshape investment decisions.

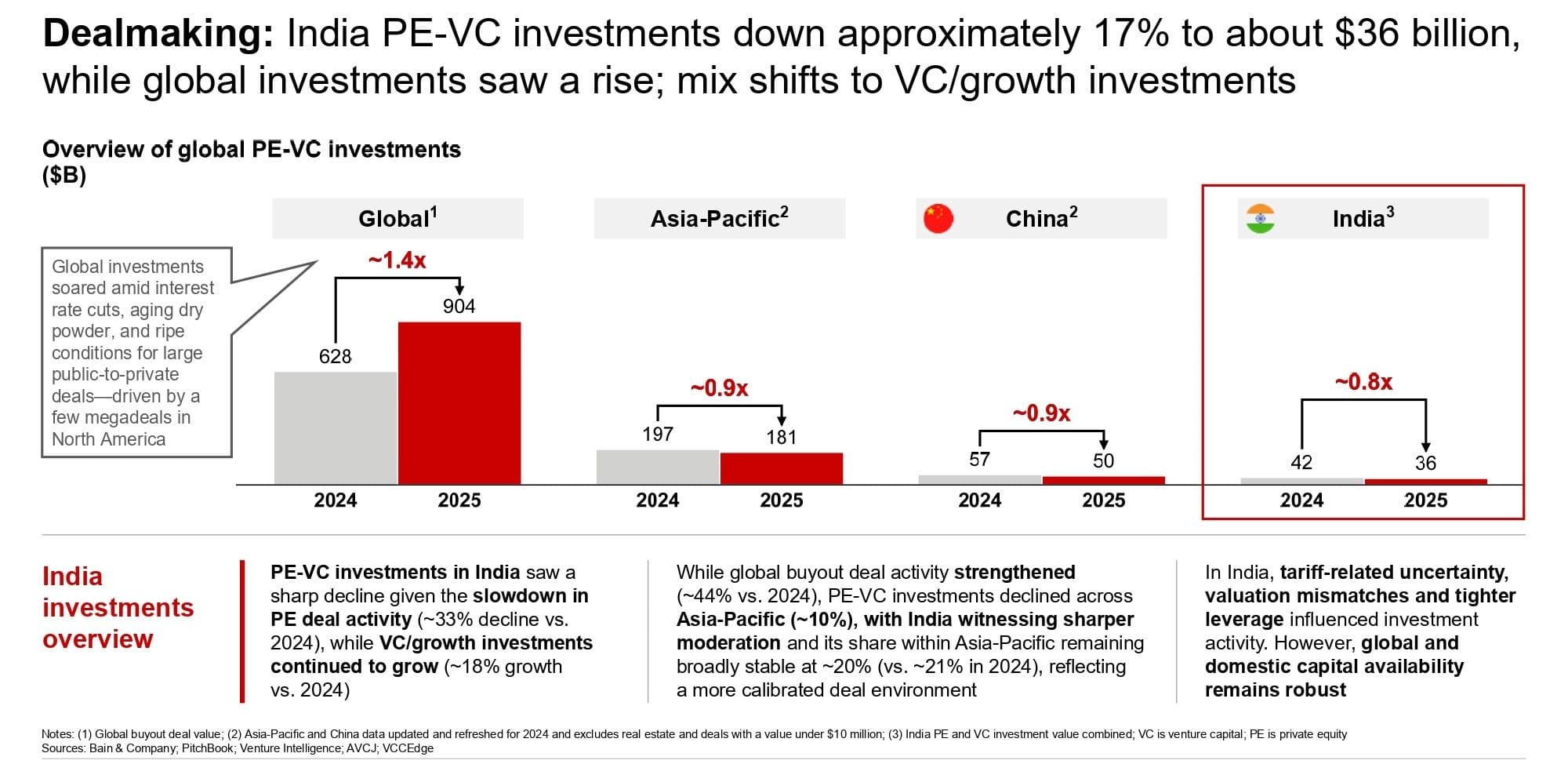

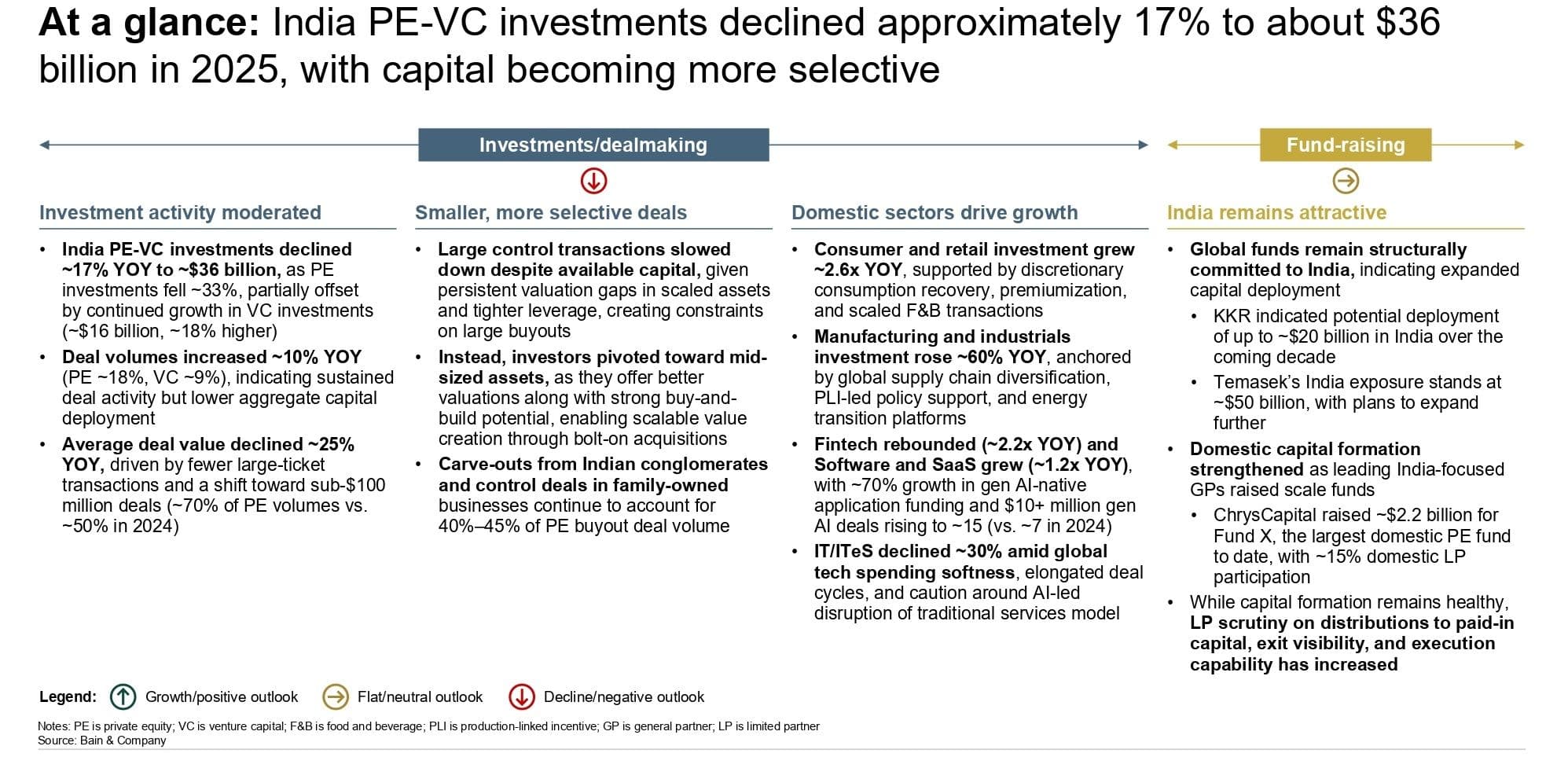

The India Private Equity Report 2026, by the Indian Venture and Alternate Capital Association and Bain & Company, said India’s PE-VC market entered a more disciplined phase in 2025, with total investments falling about 17% to $36 billion even as deal activity became broader and more diversified. The report said investors increasingly moved away from concentrated large-ticket bets and instead focused on smaller and mid-sized transactions where operational value creation and profitability pathways were clearer.

Capital Discipline Deepens

“Moderation in PE activity in 2025 reflects a reset toward disciplined capital deployment, rather than the onset of a structural downturn,” according to the report. It added that persistent valuation mismatches, slower exits and tighter leverage conditions had fundamentally altered investor behaviour.

The report said average deal sizes declined nearly 25% year-on-year as investors became more selective about deploying capital into late-stage startups and highly priced assets. Traditional buyout investments dropped about 33%, while growth and venture investments rose around 18%, signalling a preference for calibrated expansion rather than speculative scaling.

This shift has become visible across sectors. Investors increasingly favoured consumer-facing and manufacturing businesses benefiting from India’s domestic consumption story and supply-chain diversification trends. Consumer and retail investments jumped 158% in 2025, driven by demand for scalable brands such as Haldiram's, Theobroma and Belgian Waffle Co. The report said rapid expansion through quick commerce, premiumisation and higher discretionary spending among millennials and Gen Z consumers helped attract fresh capital.

In consumer technology, however, investors displayed greater caution. Funding into consumer tech fell 13% after the exuberance of previous years, though scaled businesses such as Lenskart, Urban Company and OYO remained firmly on investor radar because of stronger unit economics and clearer profitability trajectories.

“Consumption remains a growth engine in India… the upgrade story remains alive and well, supported by rising incomes and a growing middle class,” said leading global investment firm KKR in February 2026.

Manufacturing and industrials also emerged as a major investment theme as investors chased businesses linked to electronics, electric mobility and supply-chain localisation. Companies such as JBM Ecolife Mobility, Vertelo and Raphe mPhibr attracted investor attention amid rising demand for EV infrastructure, semiconductor ecosystems and advanced manufacturing.

The report noted that investors increasingly view India as a strategic manufacturing alternative amid geopolitical tensions and global supply-chain realignments. Public infrastructure spending, policy support through production-linked incentive schemes and the expansion of electronics manufacturing services have further strengthened the investment case for domestically aligned businesses.

Exit Markets Recalibrate

Even as investors became more selective on funding, exit activity remained relatively resilient. PE-VC exits rose about 3% to $34 billion in 2025, although the number of exits declined sharply to 290 from 360 in the previous year, according to the report. Investors increasingly diversified exit routes beyond IPOs as public markets turned volatile and valuation expectations weakened.

Public market exits declined around 28% to $14 billion, largely because block trades and secondary transactions weakened sharply. However, strategic sales and buybacks gained momentum as companies and investors sought alternative liquidity pathways. Strategic sales accounted for 21% of total exit value in 2025 compared with 16% a year earlier.

Among the most prominent exits was Schneider Electric India’s $6.4 billion buyback from Temasek Holdings, one of the largest transactions of the year. Healthcare deals also gathered pace, including strategic exits involving J B Chemicals and AGS Health. Paytm, Groww and Zomato featured among significant public-market and block-trade exits, reflecting investor preference for liquid, scaled digital businesses with stronger revenue visibility.

“The 2025 exit environment reflects structural evolution as public markets are rewarding disciplined execution over aggressive growth narratives,” noted Blume Ventures in February 2026, according to the report.

The softer IPO environment also forced several companies, including boAt, OfBusiness and PayU, to recalibrate listing plans and fundraising expectations amid weaker market sentiment and valuation pressure.

Profitability Becomes King

The report said investors are increasingly prioritising startups with sustainable margins, disciplined expansion strategies and stronger governance frameworks. Limited partners are also becoming more demanding, with nearly 60% of funds surveyed saying investors now place greater emphasis on track record, distributions and execution capability before committing fresh capital.

“As investors, we’re cautious on export-oriented businesses for now but domestic consumption remains a solid anchor. We see rural consumption holding up better than urban in recent months,” Investcorp said in October 2025, as mentioned in the report.

The report added that investors are now actively searching for businesses capable of delivering operational improvements rather than relying on valuation expansion alone. This has increased interest in profitable consumer platforms, financial services firms and AI-led infrastructure businesses.

AI is also emerging as a core investment theme. The report said funds are embedding AI tools into portfolio companies to improve productivity, sharpen underwriting and accelerate revenue growth. Data centre operators, semiconductor-linked businesses and AI infrastructure providers are expected to attract significant capital over the next few years as India scales digital capacity.

Companies linked to the AI and digital infrastructure ecosystem, including electronics manufacturing and advanced semiconductor supply chains, are expected to benefit from this next wave of investment. Investors are also closely tracking emerging opportunities in specialised cooling systems, AI-ready data centres and power infrastructure as enterprise AI adoption gathers pace.

The report said India remains one of the most attractive long-term investment destinations globally, with nearly 90% of the world’s top 30 funds maintaining active exposure to the country. Yet the era of easy capital appears decisively over. Investors are no longer rewarding startups merely for scale or rapid expansion. The new benchmark is clear profitability, disciplined execution and the ability to survive in a more demanding capital environment.