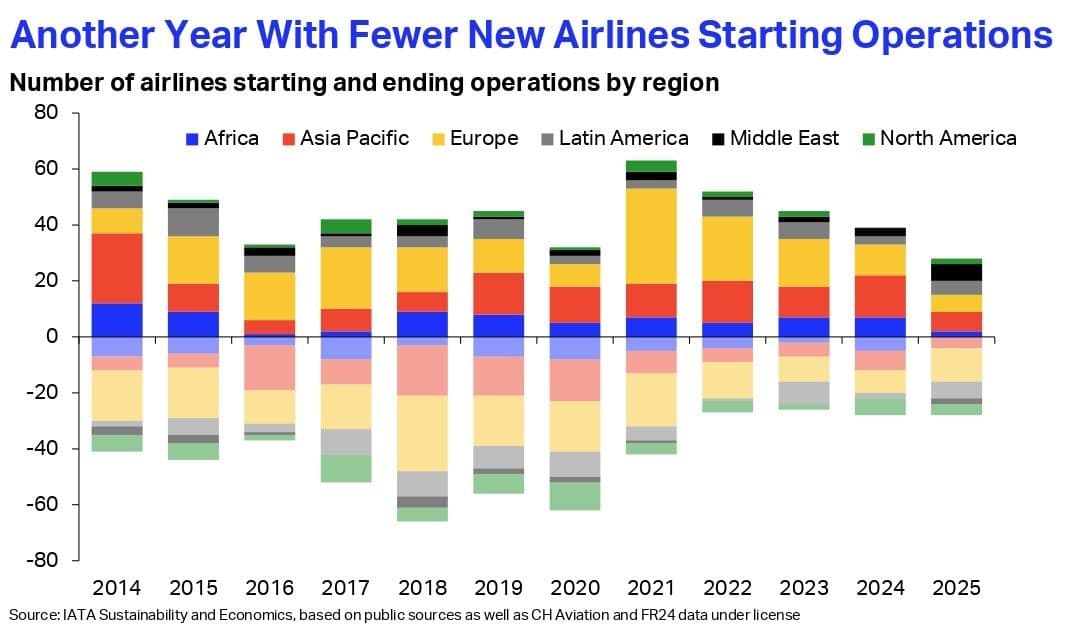

New Delhi: The number of new airlines commencing operations fell sharply in 2025, reaching the lowest level in more than two decades, according to latest data released by International Air Transport Association (IATA). Only 28 new airlines entered the global market during the year, marking the smallest number of launches since 1999 and extending a steady decline that began after a post-pandemic peak in 2021.

According to IATA, the spike in new airline launches seen in 2021 was largely artificial, driven by post-Covid restructurings, re-brandings, and restarts that temporarily inflated market entry figures. Since then, the trend has reversed, with fewer operators willing or able to launch new airlines despite a recovery in demand fundamentals.

The IATA data show that global air travel demand grew by 5.3% in 2025, measured in revenue passenger kilometres (RPK), while air cargo demand expanded by 3.4%, measured in cargo tonne kilometres (CTK). Load factors across both passenger and cargo markets reached record highs during the year.

According to IATA, these indicators suggest that the slowdown in new airline creation is not the result of market saturation. Instead, IATA attributes the decline to a combination of structural and external constraints. Persistent shortages of aircraft, engines, and spare parts have limited fleet availability and driven up costs, creating significant barriers to entry for new carriers. Supply-chain disruptions have continued to affect aircraft manufacturers and maintenance providers, while geopolitical tensions and shifting trade and aviation policies have increased uncertainty for long-term strategic planning.

In addition, IATA notes that regulatory and certification requirements have become more complex and stringent in many jurisdictions, further raising the financial and operational hurdles associated with launching a new airline. Together, these factors have created an environment in which strong demand does not automatically translate into favourable conditions for new market entrants.

At the same time, airline exits stabilized in 2025. According to IATA, 28 airlines ceased operations during the year, exactly matching the number of new entrants. This balance between entries and exits suggests that the global airline industry has entered a period of relative stability compared with the heightened volatility of the early 2020s.

However, IATA cautions that margins across the industry remain thin. Of the airlines that exited the market in 2025, 21 were full-service carriers, four were low-cost carriers, and three were leisure airlines. While many surviving airlines have strengthened their balance sheets, restored traffic volumes to pre-pandemic levels, and improved operational efficiency, vulnerabilities persist, particularly among network carriers facing high fixed costs and ongoing fleet challenges.

According to IATA, the current equilibrium reflects an industry that has largely recovered from the immediate shocks of the pandemic but continues to face structural constraints that limit growth in airline numbers, even amid robust demand.

Cover photo by Eva Darron on Unsplash