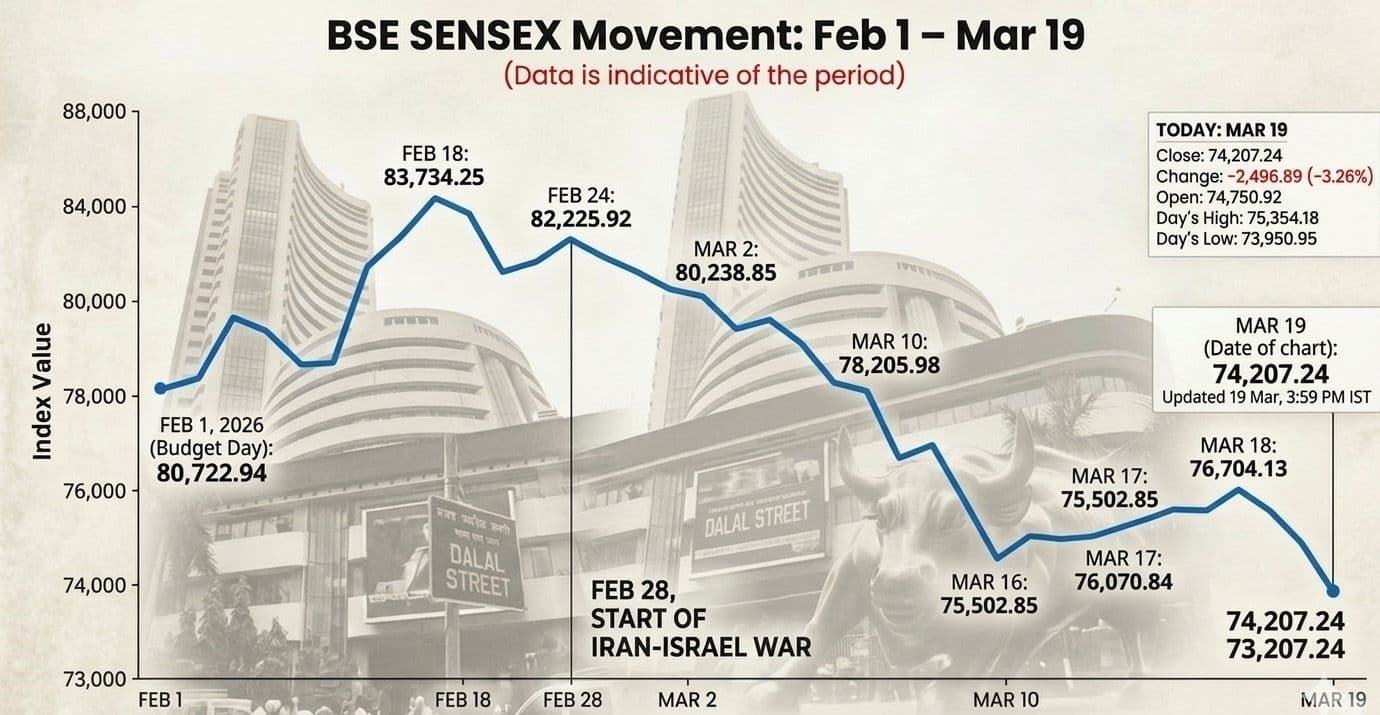

New Delhi: Market sentiment eroded sharply on Thursday, leaving investors rattled and risk appetite visibly impaired across Sensex and Nifty constituents. What unfolded on Dalal Street was not a routine correction but a disorderly repricing of risk triggered by a confluence of macro shocks and domestic uncertainty, exposing the market’s vulnerability to external variables at a time when valuations remain elevated.

The BSE Sensex plunged 2,497 points, or 3.26%, to close at 74,207, while the Nifty 50 dropped 776 points, or 3.26%, to settle at 23,002. Intra-day, the damage was even more severe, with the Sensex crashing as much as 2,753 points and the Nifty slipping below the 22,950 mark. The sell-off wiped out nearly ₹14 lakh crore in investor wealth in a single session, underlining the intensity of the risk-off sentiment gripping Dalal Street.

The correction was not limited to frontline indices. Broader markets mirrored the decline, with the Nifty Midcap 100 falling 3.2% and the Nifty Smallcap 100 shedding close to 3%. Every major sectoral index ended in the red, pointing to a broad-based liquidation rather than a sector-specific correction. Banking, IT, auto, FMCG and PSU stocks all came under heavy selling pressure, signalling a widespread shift in investor positioning.

The synchronized decline across large caps, midcaps and small caps, alongside uniform sectoral weakness, signals not a rotation but a liquidity-driven unwind. In such phases, correlations converge toward one, and fundamentals temporarily take a back seat to flows.

At the core of the correction lies a sharp deterioration in the global macro matrix. Brent crude’s spike above $116 per barrel, driven by the escalation of the Iran-Israel war, has introduced a first-order shock to India’s macro stability. For an economy structurally dependent on imported energy, this is not merely a terms-of-trade issue but a multi-channel transmission risk. Higher crude feeds directly into inflation expectations, compresses corporate margins, widens the current account deficit, and exerts downward pressure on the rupee. Each of these variables independently warrants a higher risk premium; together, they create a compounding effect.

The external liquidity backdrop has simultaneously tightened. The US Federal Reserve maintained its policy stance but delivered a distinctly hawkish undertone by flagging energy-driven inflation risks. The implication is clear: the timeline for monetary easing in the US is likely to be pushed out. For emerging markets, including India, this translates into a prolonged phase of constrained global liquidity, reinforcing foreign portfolio outflows.

HDFC Bank ‘Shock’

These macro pressures were amplified by a critical domestic trigger. The abrupt resignation of chairman Atanu Chakraborty from HDFC Bank injected a governance overhang into the market’s most systemically important stock. The resulting 8% drawdown in HDFC Bank was not merely a stock-specific correction but a systemic shock, given its heavy index weight and its role as a proxy for financial sector stability. The reassurance from interim Chairman Keki Mistry failed to arrest the slide, indicating that investors are demanding a higher governance risk premium.

Financials, which typically anchor market stability, instead became the epicentre of the sell-off. Weakness in HDFC Bank spilled over into peers such as ICICI Bank and State Bank of India, dragging the broader banking index lower. Simultaneously, IT stocks including Infosys and TCS corrected on concerns of slowing global demand, while consumption-facing names like Hindustan Unilever repriced to reflect margin pressures from input cost inflation. The absence of defensive pockets underscores the indiscriminate nature of the selling.

Foreign institutional investors (FIIs) remain a persistent overhang. Fourteen consecutive sessions of net selling point to a structural repositioning rather than tactical profit booking. In an environment where global risk-free rates remain elevated and geopolitical uncertainties are high, capital is rotating toward safer assets. Domestic flows, while resilient, are insufficient to fully counterbalance sustained FII outflows during risk-off phases of this magnitude.

Future Tense

What next is contingent on variables largely exogenous to India. The trajectory of crude prices will be the single most critical determinant. A sustained elevation above current levels would force a reassessment of India’s FY26 macro assumptions, including inflation, fiscal math and earnings growth. Equally important is the evolution of the Federal Reserve’s policy stance; any further delay in rate cuts will tighten financial conditions globally and cap upside in emerging market equities.

From a market structure perspective, volatility is unlikely to mean-revert quickly. The sharp unwinding suggests that leverage — both explicit and implicit — was higher than perceived. As positions are recalibrated and risk models reset, markets could remain range-bound with episodic drawdowns. Valuation multiples, particularly in segments that were pricing in aggressive growth assumptions, may continue to compress.

That said, the current phase does not yet signal a breakdown in India’s structural investment thesis. Domestic growth drivers —consumption resilience, public capex and financial sector depth — remain intact. However, the market is moving away from easy, liquidity-fuelled gains to a phase where fundamentals and macro factors matter more. In this environment, stock performance will vary more widely, and broad, market-wide rallies will be harder to sustain.

For investors, the imperative is to recalibrate expectations rather than capitulate. The repricing underway is a function of higher global risk premiums, not a collapse in underlying earnings capacity. If crude stabilizes and global liquidity conditions cease to tighten further, markets could find a base. Until then, caution will dominate positioning, and volatility will remain the defining feature of Dalal Street.