New Delhi: The formalisation of the Iran-US agreement (as much as we know of it) has triggered a rapid reassessment across global energy markets. While investors initially focused on the military implications of the de-escalation, commodity traders and policymakers quickly recognised that the deal could reshape oil supply, shipping routes, investment patterns and regional power dynamics.

By allowing Iranian crude to re-enter international markets under a structured sanctions-relief framework and by reducing the risk of disruption in the Strait of Hormuz, the agreement has the potential to alter the trajectory of global energy prices and the strategic calculations of major oil-producing nations.

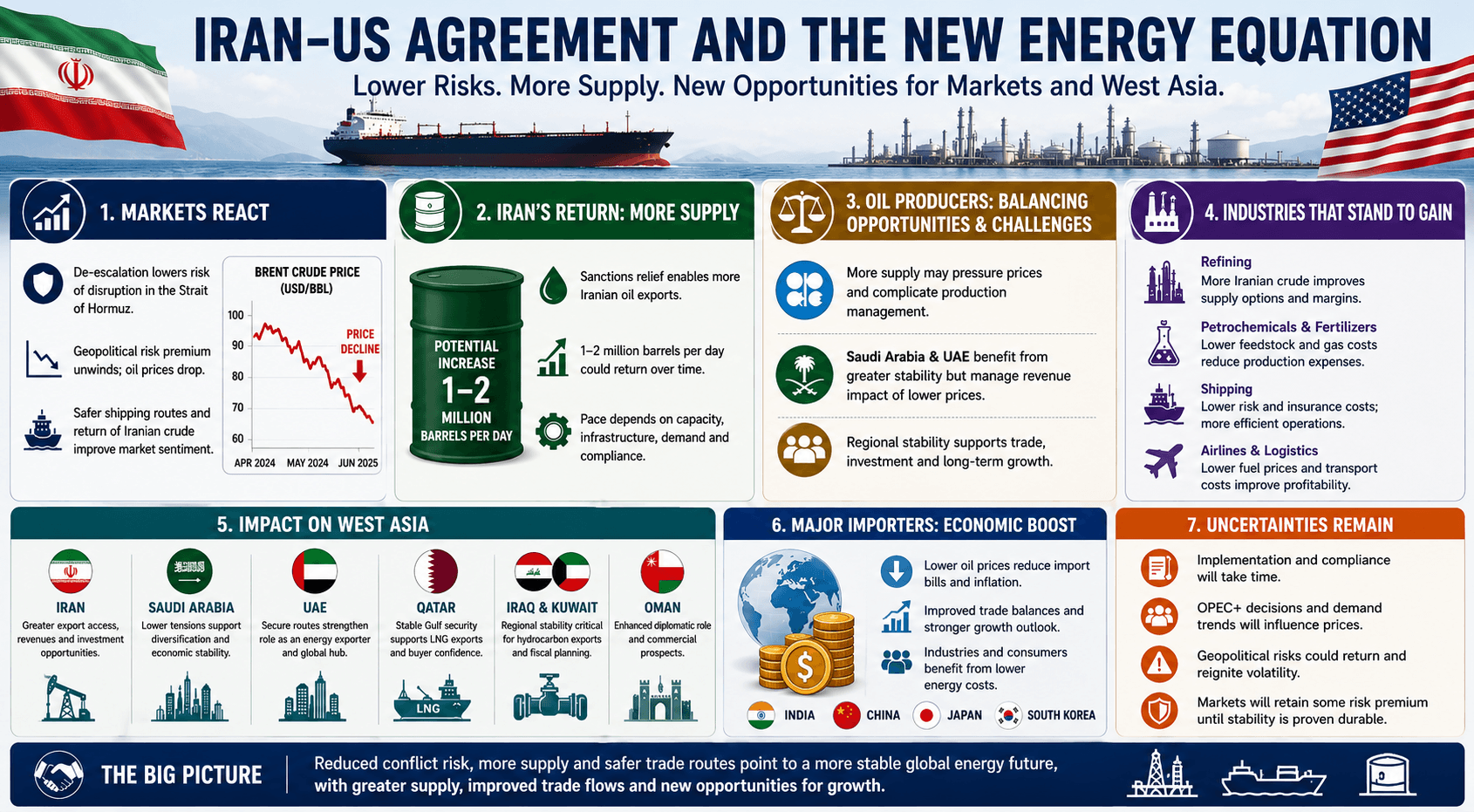

Geopolitical Premium Unwinds

The first response from the market has been a sharp unwinding of the geopolitical premium built into crude prices over the recent months. During the period of heightened tensions, traders priced in the possibility that military escalation could disrupt traffic through the Strait of Hormuz, a narrow maritime corridor through which roughly 20 million barrels of crude and petroleum products move every day. The waterway also carries a substantial share of global liquefied natural gas (LNG) shipments, making it one of the world’s most critical energy chokepoints.

As the agreement reduced the immediate threat to shipping lanes, benchmark crude prices retreated and financial markets responded positively. Investors interpreted the deal as lowering the probability of prolonged supply interruptions and reducing uncertainty across commodity markets. The immediate downward movement in crude prices reflected investors’ expectations of smoother maritime trade and an eventual increase in Iranian oil exports.

Iran occupies a significant position in the global hydrocarbon industry. It possesses some of the world’s largest proven reserves of both crude oil and natural gas. Before sanctions tightened over the past decade, the country exported well over two million barrels of oil every day. Although Iranian crude continued to reach some international buyers through indirect channels, sanctions on shipping, insurance and banking constrained official exports.

The new arrangement changes that equation considerably. The removal or easing of restrictions on financial transactions, tanker operations and insurance services could enable Iran to increase formal exports over time. Energy analysts estimate that between one and two million barrels per day could eventually be restored to global supply, although the pace will depend on production capacity, infrastructure upgrades, market demand and the implementation of the agreement’s compliance mechanisms.

OPEC Faces Challenges

This prospect presents both opportunities and challenges for the Organization of the Petroleum Exporting Countries and its allies. OPEC+ has spent years balancing production cuts and output increases to maintain stability in oil prices. A substantial increase in Iranian exports could complicate those efforts by adding fresh supply to an already competitive market.

Saudi Arabia and the United Arab Emirates may find themselves navigating a delicate balance. Both countries have invested heavily in maintaining spare production capacity and have played leading roles in OPEC+ production management. While lower prices could reduce export revenues, a more stable regional security environment would benefit their broader economic interests by reducing geopolitical risks and supporting trade.

The impact extends well beyond oil producers. Refining companies are among the likely short-term beneficiaries of the agreement. Iranian crude grades have traditionally been attractive to many Asian refiners because of their quality characteristics and pricing advantages. Greater availability of these supplies could improve operational flexibility and enhance refining margins.

Petrochemical manufacturers may also gain from the resulting changes in feedstock costs. Lower prices for crude-derived products and natural gas liquids could reduce production expenses for plastics, chemicals and industrial materials. Fertiliser producers, particularly those dependent on natural gas inputs, could experience similar advantages if regional gas markets stabilise.

The shipping sector stands to benefit from lower operational risks. During periods of conflict, war-risk insurance premiums increased significantly, freight costs rose and several commercial vessels were forced to alter routes or delay shipments. A reduction in security concerns surrounding the Arabian Gulf region should gradually lower insurance charges and improve shipping efficiency. However, industry experts note that insurers and shipping companies typically require sustained periods of stability before fully adjusting risk assessments.

Airlines and logistics companies could emerge as additional winners. Aviation fuel prices are closely linked to crude markets, and lower oil prices generally improve profitability for carriers. Freight operators and global supply chains would also benefit from reduced transportation costs and more predictable maritime operations.

The effects on upstream energy companies are likely to vary. Large integrated oil firms with significant refining and trading operations may offset weaker crude prices through gains elsewhere in their businesses. Independent exploration and production companies, however, could face pressure on revenues if oil benchmarks remain lower for an extended period.

Regional Economic Winners

Among the countries of West Asia, Iran is positioned to secure the most immediate economic gains. Greater access to export markets, international finance and shipping services could strengthen government revenues and encourage investment in the country's energy infrastructure. Nevertheless, these benefits remain dependent on the durability of the agreement and continued adherence to its provisions.

Saudi Arabia faces a more complex strategic landscape. The kingdom’s economic diversification agenda relies partly on robust hydrocarbon revenues, meaning lower oil prices could affect fiscal planning. At the same time, reduced regional tensions would support investment, trade and long-term economic development, creating incentives for maintaining stability.

The United Arab Emirates is similarly placed to gain from calmer regional conditions. As both a major energy exporter and an international logistics hub, the UAE benefits from secure maritime trade routes and predictable commodity markets. Lower geopolitical risks strengthen its position as a centre for finance, shipping and global commerce.

Qatar’s interests are closely tied to natural gas exports. As one of the world’s leading LNG suppliers, the country depends heavily on uninterrupted navigation through the Strait of Hormuz. A stable security environment enhances confidence among buyers and supports long-term supply contracts.

Iraq and Kuwait also have significant stakes in the outcome. Their economies rely heavily on hydrocarbon exports transported through Gulf shipping routes, making regional stability an important factor in fiscal and economic planning.

Oman occupies a distinctive position. Its longstanding diplomatic role in regional affairs, combined with its strategic location near major shipping corridors, means that reduced tensions could enhance both its geopolitical importance and commercial prospects.

For major importing economies such as India, China, Japan and South Korea, the agreement could generate substantial economic benefits. These countries collectively account for a large share of Gulf energy imports. Lower oil prices would reduce import bills, ease inflationary pressures and improve trade balances. Industries ranging from manufacturing to transportation could experience lower operating costs, potentially supporting broader economic growth.

Uncertainties Still Remain

Despite the optimism surrounding the agreement, several uncertainties remain. Energy markets rarely adjust in a straight line after major geopolitical developments. The restoration of Iranian production capacity, the rebuilding of commercial relationships and the normalisation of shipping and insurance markets will take time. Production decisions by OPEC+, demand trends in Asia and the pace of global economic growth will also influence price movements.

Moreover, geopolitical risks have not disappeared entirely. Future disagreements over compliance, shifts in domestic politics or renewed regional tensions could quickly reintroduce volatility into energy markets. For this reason, traders are unlikely to eliminate the geopolitical risk premium completely, even if immediate concerns diminish.

The broader significance of the Iran-US agreement lies in the fact that it changes expectations about future energy security rather than merely affecting current supply. The return of Iranian exports, safer navigation through the Gulf and improved commercial confidence collectively point towards a more stable energy environment. Markets have responded accordingly by lowering prices and reassessing risk.

Whether this transition proves durable will depend on the successful implementation of the agreement and the willingness of regional and global stakeholders to preserve stability. In the short term, however, the message from energy markets is clear. The reduction of conflict risk has shifted attention away from fears of scarcity and towards the prospect of greater supply, improved trade flows and a more balanced global oil market. The quick reaction may be measured in falling crude prices, but the deeper story is one of changing geopolitical assumptions that could influence the global energy system for years to come.