New Delhi: The Global Trade Research Initiative (GTRI) has called for closer scrutiny of tariff concessions granted under the India-UAE trade agreement, warning that the framework is accelerating gold imports into India and increasing pressure on the country’s trade balance and foreign exchange reserves.

The trade policy think tank has urged the government to reassess preferential duty benefits on bullion imports routed through Dubai, arguing that India’s growing dependence on imported gold poses a significant macroeconomic challenge at a time of global financial uncertainties.

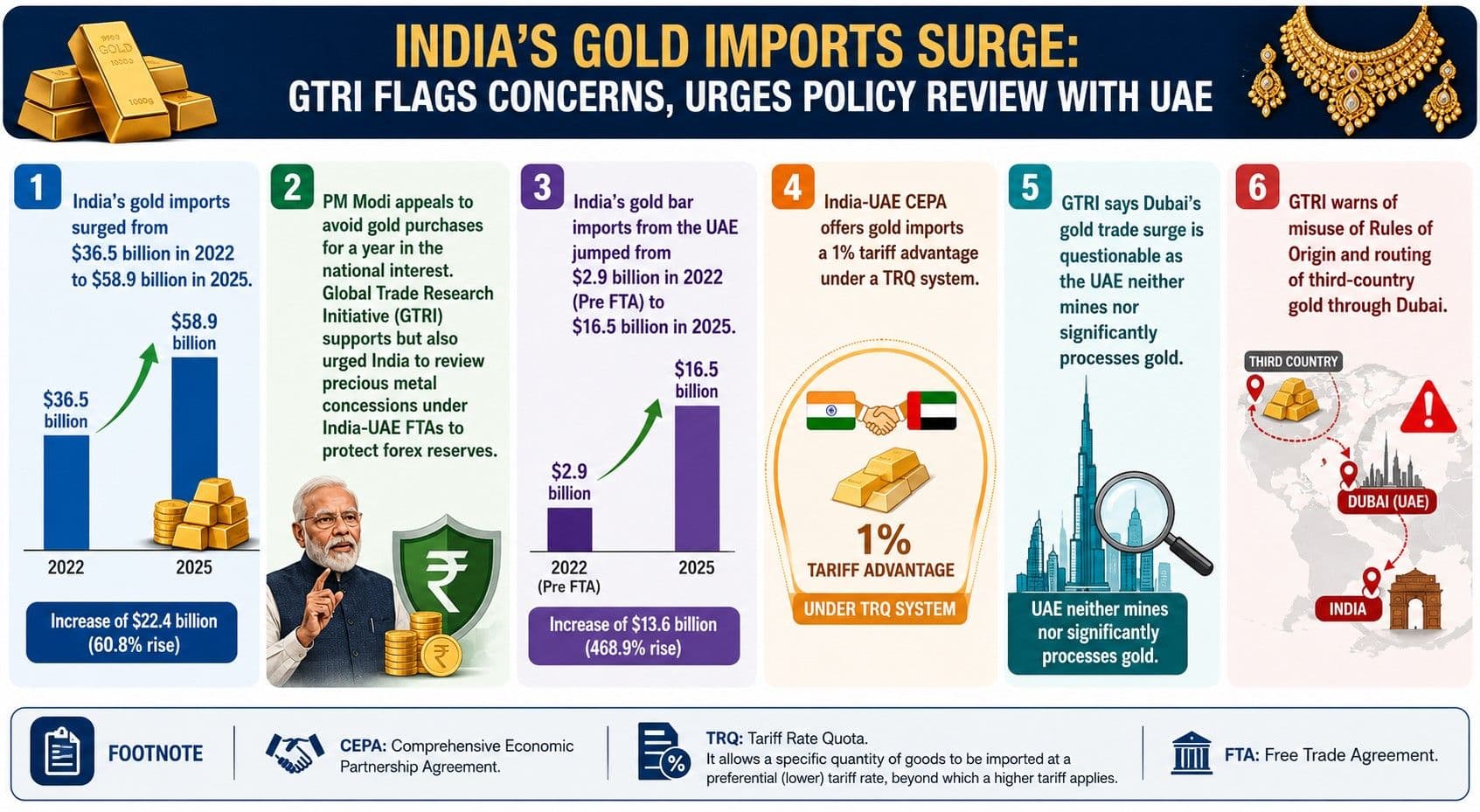

The warning comes amid Prime Minister Narendra Modi’s appeal to citizens to avoid non-essential gold purchases for a year, including jewellery bought for weddings and social functions. Speaking on May 10, Modi linked household spending behaviour to the country’s broader economic resilience and called for restraint in discretionary consumption of imported commodities.

“If possible, avoid buying gold for one year,” the PM said, framing the issue not merely as a matter of personal consumption but as an economic responsibility tied to national stability during a volatile global environment.

India’s gold imports have risen sharply in recent years, underlining the scale of the concern. Gold bar imports (under HS7108) increased from $36.5 billion in 2022 to $58.9 billion in 2025, according to trade data cited by GTRI. Since India imports nearly all the gold it consumes, rising demand for bullion has become a persistent source of pressure on the current account deficit, especially during periods of rupee weakness and elevated global commodity prices.

Economists have long argued that excessive gold imports create macroeconomic vulnerabilities because they require substantial dollar outflows without contributing meaningfully to productive industrial activity. Unlike imports linked to manufacturing or infrastructure, gold purchases are largely consumption-driven and therefore add limited long-term economic value while worsening trade imbalances.

Large-scale bullion imports also affect currency stability by increasing demand for foreign exchange. At a time when central banks across the world are focused on preserving reserves and protecting domestic currencies from external shocks, rising gold imports can reduce policy flexibility for emerging economies like India.

India-UAE Trade Deal Under Focus

GTRI’s concerns have intensified following significant changes in India’s gold import structure after the India-UAE Comprehensive Economic Partnership Agreement (CEPA) came into effect in May 2022. Under the agreement, India granted tariff concessions on gold imports from the UAE through a Tariff Rate Quota (TRQ) mechanism that allows specified quantities of bullion to enter at duties lower than the standard import rate.

Initially, the quota covered 120 tonnes of gold annually, but the limit is scheduled to rise to 200 tonnes from 2027 onwards. Analysts estimate that the quota could eventually account for nearly one-fourth of India’s total gold imports.

The pricing advantage under the agreement became even more pronounced after the Indian government reduced the standard gold import duty from 15% to 6% in the 2024 Union Budget. As a result, gold imported from the UAE under the concessional quota now effectively enters India at a duty of 5%, giving Dubai-based suppliers a clear competitive edge over other exporters.

The government has simultaneously expanded import access by permitting private firms and jewellers to directly import bullion through the India International Bullion Exchange (IIBX) at the GIFT City in Gujarat. The move was aimed at strengthening India’s role in global bullion trading, but it has also contributed to a sharp rise in trade volumes routed through Dubai.

The impact of these policy changes has been dramatic. India’s gold bar imports from the UAE climbed from $2.9 billion in 2022 to $6.7 billion in 2023 before surging further to $16.5 billion in 2025. Dubai’s share in India’s total gold imports increased from 7.9% before the trade agreement to 28% in 2025, reflecting how rapidly the UAE has emerged as a dominant gateway for bullion shipments into India.

Concerns Over Routing, Rules of Origin

The sharp rise in imports through Dubai has triggered concerns among trade analysts because the UAE itself is not a major gold producer. Experts believe a significant portion of the bullion entering India may actually originate in third countries before being routed through Dubai to benefit from lower tariffs available under the CEPA framework.

This has raised questions about the effectiveness of Rules of Origin provisions that determine whether products genuinely qualify for preferential treatment under free trade agreements (FTAs). GTRI has warned that some imports may involve only minimal or artificial processing in the UAE before being exported to India as ‘UAE-origin’ gold eligible for concessional duties.

GTRI founder Ajay Srivastava has recommended tighter origin verification norms and a broader review of precious metal concessions under India’s FTAs. He has also proposed excluding gold, silver, platinum and diamonds from future trade agreements to prevent further pressure on India’s trade balance and foreign exchange reserves.

The issue is expected to trigger a wider debate within policymaking circles over how India should balance strategic trade partnerships with macroeconomic priorities. While FTAs are intended to boost trade integration and strengthen diplomatic ties, critics argue that excessive concessions on high-value consumption imports can create unintended economic risks.

With gold continuing to occupy a central place in Indian household savings and cultural traditions, policymakers face the difficult challenge of managing demand without disrupting consumer sentiment. Modi’s appeal and GTRI’s intervention together indicate that concerns over rising bullion imports are now moving beyond trade policy discussions and entering the centre of India’s broader economic debate.