New Delhi: India’s alcobev sector is steadily entering a phase where premiumisation matters more than consumption growth. FY26 results reveal that companies with strong premium spirits portfolios captured the industry’s gains, while beer and wine producers were left battling regulatory constraints, cost pressures and limited pricing power. The divide suggests future growth will depend less on expanding the drinking base and more on extracting higher value from existing consumers.

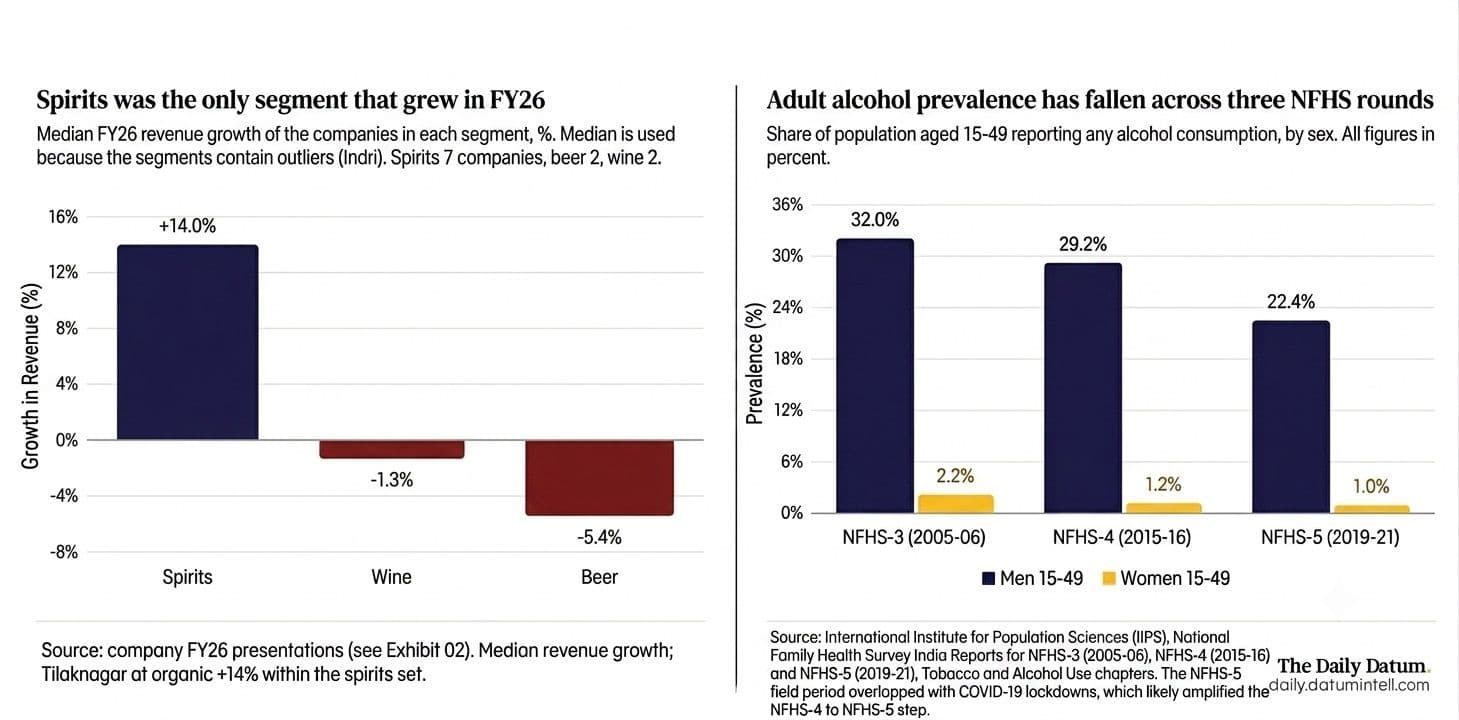

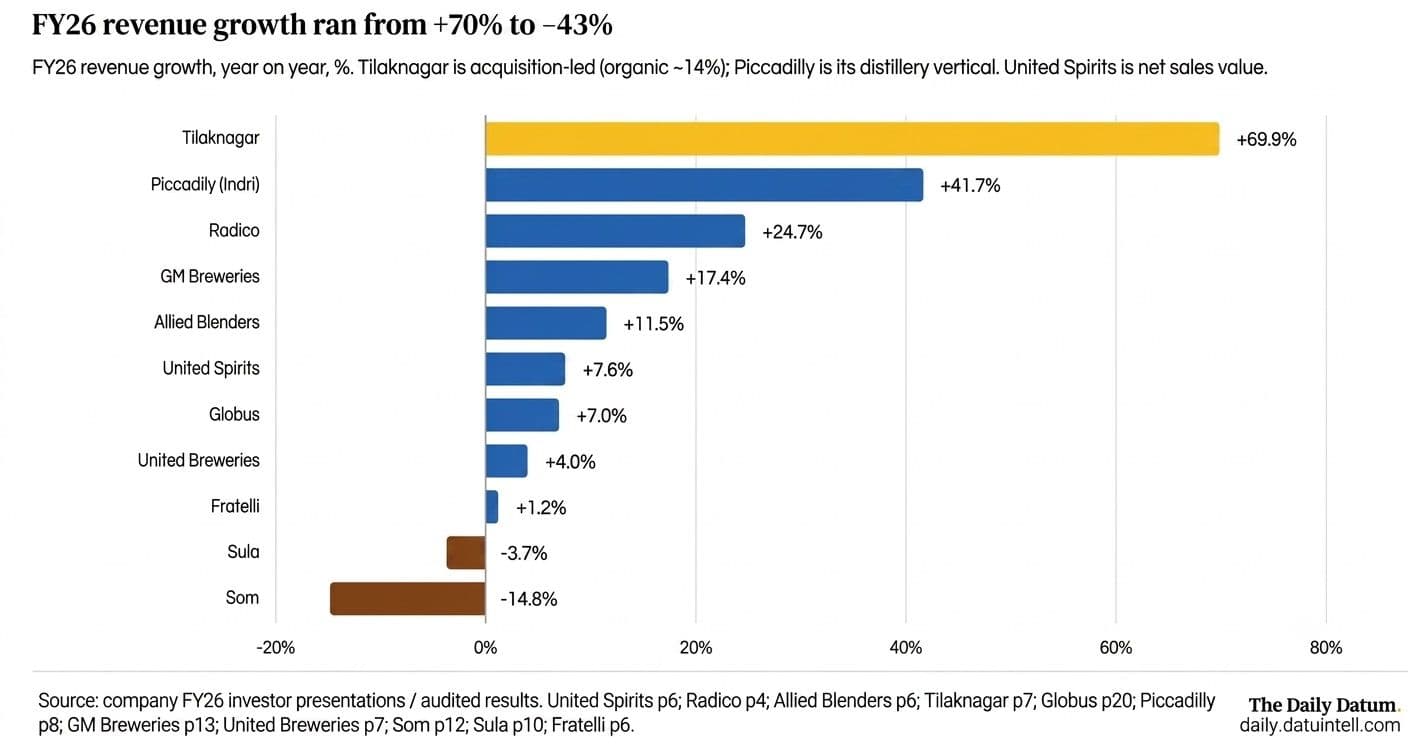

An analysis by The Daily Datum of 11 major alcobev companies shows that virtually all meaningful growth came from spirits. The numbers illustrate the shift. Tilaknagar Industries reported 70% revenue growth, aided by its acquisition of Imperial Blue. Piccadily Agro’s Indri-led distillery business expanded 42%, while Radico Khaitan and Allied Blenders & Distillers posted growth of 25% and 12%, respectively. At the other end of the spectrum, United Breweries grew revenue by just 4%, Sula Vineyards saw revenue decline 4%, and Som Distilleries reported a 15% drop.

The divergence is rooted in a fundamental demographic reality. India’s drinking population is not expanding at the pace many companies once anticipated. National Family Health Survey data show alcohol consumption among men aged 15-49 declined from 32% in 2005-06 to 22.4% in 2019-21, while consumption among women fell from 2.2% to 1%.

“The drinking base is not expanding; premium mix is the only revenue lever,” said the report. “If the population of drinkers is structurally shrinking, aggregate category volume cannot grow on prevalence. Revenue can only come from two places: more litres per drinker, or premium mix.”

That reality is reshaping corporate strategy across the sector. The battle is no longer centred on attracting new consumers. Instead, companies are focused on persuading existing drinkers to move from regular whisky to prestige brands, from standard beer to premium labels, and increasingly from imported products to locally produced luxury offerings.

Premiumisation Deepens

From automobiles and smartphones to hospitality, premiumisation has been a recurring theme in India’s consumer industries. In alcoholic beverages, however, the trend is proving particularly powerful because volume growth has become increasingly difficult to achieve.

Across the industry, premium portfolios grew faster than broader product ranges. Allied Blenders reported 27% growth in Prestige & Above volumes, while Radico’s equivalent portfolio expanded 22%. United Breweries recorded 21% growth in premium beer volumes even as overall category growth remained modest. United Spirits reported Prestige & Above net sales growth of 8.6%, exceeding total sales growth of 7.6%.

Yet one of the most striking findings is the limited transparency around premiumisation. While nearly every company highlights growth in premium brands, very few disclose how much of their business those brands actually represent.

“Every company premiumised; only Radico and Sula will say how much,” the report noted. “The premium tier grew faster than the total everywhere. The right question is how much of sales is actually premium.”

Radico disclosed that Prestige & Above products accounted for 45.6% of total volumes in FY26, up sharply from 29% in FY20. Sula revealed that Elite & Premium wines contributed 78% of own-brand revenue. For most competitors, investors are left to infer the scale of premiumisation from growth rates rather than hard portfolio data.

The biggest beneficiary of the trend has been India’s emerging single malt whisky segment. Piccadily Agro’s Indri brand has rapidly evolved from a niche premium product into one of the most significant growth stories in the industry. The company’s distillery business generated ₹902 crore in revenue and delivered a 32% EBITDA margin during FY26.

“The single most striking story in the set is Piccadily’s Indri,” the report observed. “Its distillery business, almost entirely premium single malt, grew revenue 42% to ₹902 crore at a 32% EBITDA margin.”

The rise of Indian single malts also reflects broader shifts in consumer behaviour. Currency-driven increases in the price of imported Scotch have encouraged affluent consumers to explore domestic alternatives, while Indian distillers have spent years building capacity and improving quality. The result is the emergence of premium local brands capable of competing directly with imported products.

Winners & Losers

The industry’s performance in FY26 also highlights an increasingly important distinction: premiumisation and profitability are not the same thing.

Several spirits companies successfully converted premium growth into earnings expansion. Radico Khaitan’s EBITDA increased 52%, Allied Blenders reported 26% EBITDA growth, while Globus Spirits and Piccadily Agro also delivered strong profit gains. Even GM Breweries, operating largely in the value segment, generated one of the highest margins in the industry, demonstrating that disciplined execution can be as important as premium positioning.

By contrast, beer and wine producers found it far more difficult to translate premium demand into stronger earnings. United Breweries increased premium volumes but still experienced pressure on profitability due to state-level pricing controls and higher input costs. Sula’s margins contracted significantly despite a premium-heavy portfolio, while Fratelli struggled to convert strong gross margins into meaningful bottom-line performance.

“The other half of the field premiumised and still earned less,” the report said. “Premium mix is the entry ticket. The win still depends on pricing power, cost base and state policy reaching profit.”

This distinction may become increasingly important as investors assess the sector. Premium growth alone is no longer a differentiator because nearly every major player is pursuing the same strategy. What matters now is whether companies can convert premium positioning into sustainable earnings growth.

State-level regulation remains another critical variable. Alcohol remains one of India’s most fragmented consumer markets, with pricing, taxation and distribution determined largely by individual states. Companies including United Spirits, Som Distilleries and Fratelli have highlighted the impact of regulatory disruptions and pricing restrictions on growth and profitability.

Looking ahead, the industry appears to be entering a consolidation phase familiar to many consumer sectors. Large incumbents such as United Spirits will continue to leverage scale and distribution, while mid-sized players like Radico Khaitan and Allied Blenders seek growth through premium portfolios. Emerging challengers such as Piccadily Agro are attempting to redefine high-end categories altogether.

For investors, the central takeaway from FY26 is that India’s alcohol market is becoming less about volume and more about value. The consumer is drinking better rather than drinking more. That shift has created significant opportunities for premium spirits, particularly single malts and prestige whisky brands, while exposing the limitations of beer and wine categories facing weaker pricing power and regulatory complexity.

The sector’s next phase will likely be determined not by how fast premium products grow, but by which companies can transform that premium mix into durable profitability. In FY26, spirits proved they could. Beer and wine still have work to do.

(Cover photo by Luwadlin Bosman on Unsplash)