New Delhi: India’s cotton economy has slipped into one of its most turbulent phases in decades, with falling domestic production, rising raw material costs, and persistent price distortions threatening the competitiveness of the country’s $180 billion textile industry.

The report, Economic Analysis of Cotton Supply, Pricing, and Trade Policy in India, prepared for the Confederation of Indian Textile Industry (CITI) with inputs from the Gherzi Textile Organization and the International Cotton Advisory Committee (ICAC), argues that India’s cotton pricing mechanism has drifted away from global benchmarks, creating structural stress across the textile value chain.

Incidentally, the report arrives at a critical juncture for India’s textile sector, which contributes 8% of merchandise exports and employs nearly 45 million people directly. While India remains the world’s second-largest cotton producer, the study warns that declining yields, import barriers and widening supply-demand deficits are eroding the country’s export competitiveness just as global rivals such as Vietnam and Bangladesh aggressively expand capacity.

“India’s cotton balance sheet over the past decade reveals a gradual but decisive shift from periodic surpluses to a structurally tighter market in which domestic production no longer fully supports the requirements of the textile value chain,” the report said. “This makes imports imperative to not only meet the current year’s consumption but also maintain a healthy ending stock.”

The report notes that cotton production has fallen sharply from a peak of 370 lakh bales in 2017-18 to a projected 291 lakh bales in 2025-26, while consumption is expected to rise to 328 lakh bales, leaving a deficit of 37 lakh bales. The imbalance follows a previous season in which demand exceeded supply by 25 lakh bales.

India’s cotton productivity remains another critical concern. National average yield stands at roughly 450 kg per hectare, significantly below the global average of around 800 kg per hectare. According to the report, low yields are inflating unit production costs despite relatively moderate cultivation expenses.

“Competitiveness is therefore influenced not only by input expenditure but also by output efficiency,” the report observed, warning that India’s long-term cotton strategy can no longer rely solely on acreage expansion or price support mechanisms.

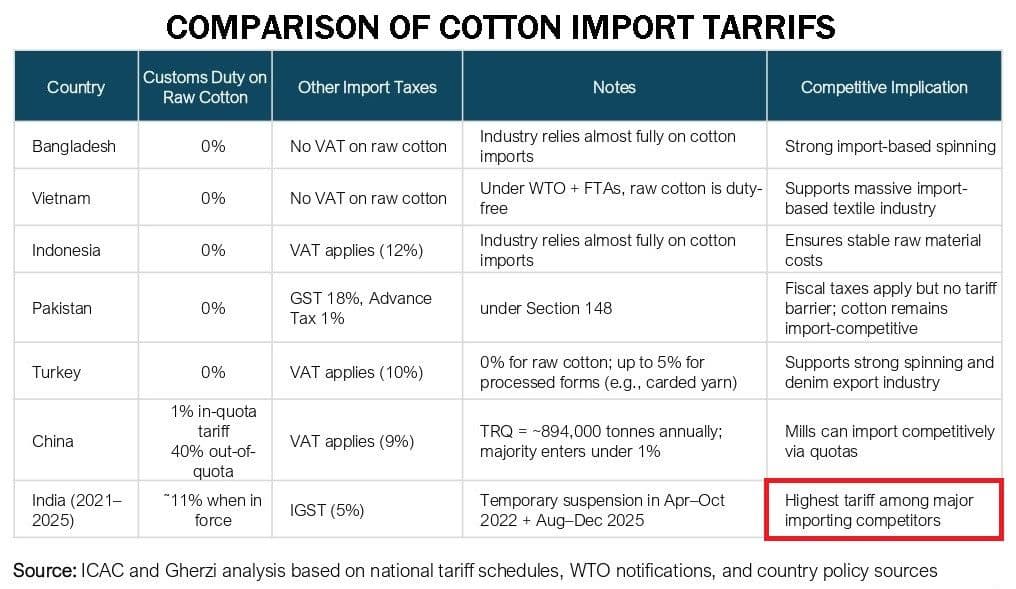

Import Duty Distortions

At the centre of the industry’s concern is the 11% effective import duty on cotton, introduced in 2021-22 and periodically suspended during supply shortages. The report argues that the tariff has fundamentally altered India’s cotton economics by disconnecting domestic prices from international benchmarks.

For years, Indian cotton traded at a discount of 3-5 cents per pound to the Cotlook A Index, the global benchmark for cotton pricing. That advantage has disappeared. Since April 2024, Indian cotton prices have remained consistently above global levels, placing domestic spinning mills at a disadvantage against competitors in Vietnam, Bangladesh, Indonesia and Pakistan, all of which allow duty-free access to imported cotton.

“The effective duty of 11% made imports prohibitive,” the report said. “This resulted in a drastic increase in the price of domestic cotton during the second half of cotton season 2023-24.”

The consequences are already visible across the textile chain. India’s cotton yarn exports have fallen from 1.3 million tonnes in 2015 to 1.1 million tonnes in 2024, while global market share has declined from 38% to 28%.

“When domestic prices move materially away from international benchmarks for extended periods, spinning mills face tighter margin management, particularly in export-oriented segments where yarn prices are determined by global competition,” the report noted.

The investment cycle has weakened sharply as well. Shipments of new ring spindles collapsed to 9 lakh units in 2024 from more than 20 lakh units annually in 2022 and 2023, reflecting deepening uncertainty in the spinning industry. Nearly 25% of India’s installed spinning capacity — around 14-15 million spindles — is estimated to be lying idle.

The report paints a particularly grim picture for MSME spinning mills concentrated in Tamil Nadu, Panipat and Kolkata, where high cotton prices have squeezed margins and weakened utilisation rates.

“Persistently high input costs have already led to a 15-20% decline in capacity utilization across spinning mills, with a sharper impact on MSME and export-focused units,” the report said. “If the current price differential continues, the industry risks a reduction of 20-25% in yarn exports, translating into an estimated $0.5-1.2 billion loss in textile export earnings on an annualized basis.”

The stress is spilling into ancillary industries too. India’s cotton recycling ecosystem, which reprocesses nearly 60 lakh bales annually into secondary raw material, has been hit by a 20% surge in cotton waste prices during 2025 despite softer lint prices.

Policy Reset Is Critical

The report strongly advocates a reset in India’s cotton policy architecture, arguing that existing interventions are no longer aligned with market realities.

“There is a need to withdraw import duty on cotton and allow the mills to have access to cotton at competitive prices,” the report said, adding that temporary duty suspensions have failed to provide long-term certainty for investment planning and export commitments.

The study proposes a broader institutional mechanism centred around the Cotton Corporation of India (CCI), including a strategic reserve system, dynamic selling policies and a price stabilisation framework linked to global benchmarks.

“From a policy standpoint, there is a need to better align domestic cotton pricing mechanisms with international market trends (Cotlook A prices) while continuing to protect farmers’ interests,” the report said. “A more balanced approach would help ensure the competitiveness of the textile industry without undermining the MSP framework.”

The report estimates that the CCI would require an annual buffer of around Rs 1,500 crore to supply nearly 100 lakh bales of cotton to domestic mills at internationally competitive prices.

At the same time, geopolitical disruptions are adding fresh urgency to the crisis. The ongoing West Asia conflict has sharply raised fertilizer, crude oil and fibre-related input costs, pushing cotton and man-made fibre prices up by 15-30% since February 2026.

“In view of such unprecedented global disruptions and their cascading impact on domestic cost structures, there is a need for a responsive policy mechanism to address sudden input cost shocks and ensure stability in raw material availability and pricing,” the report cautioned.

For India’s textile sector, the stakes are now larger than cotton alone. The industry’s ambition to achieve $100 billion in textile and apparel exports by 2030 increasingly depends on whether policymakers can restore competitiveness before global buyers shift sourcing permanently to rival manufacturing hubs.

(Cover photo by Trisha Downing on Unsplash)