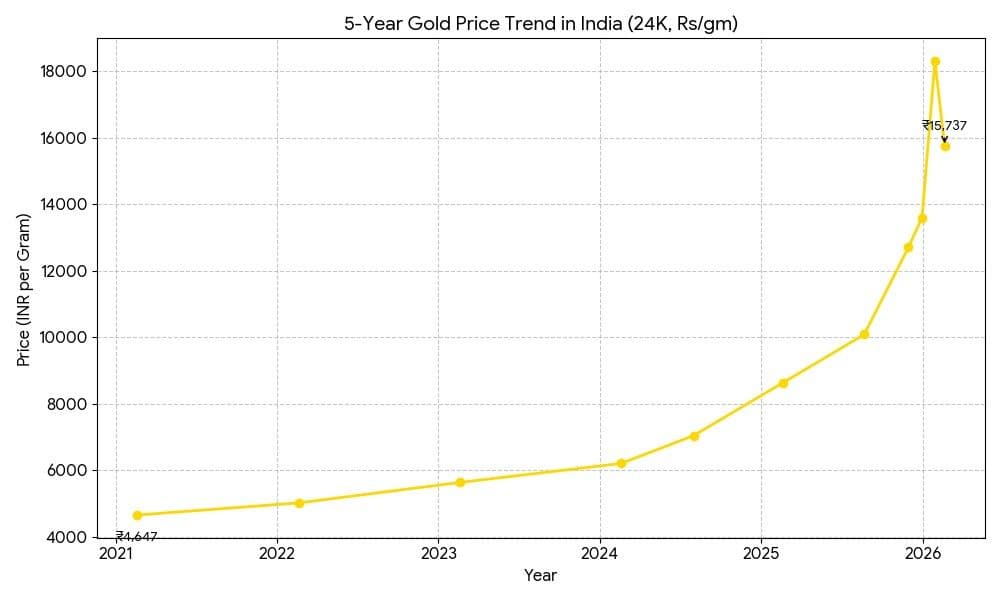

New Delhi: Gold’s blistering run into early 2026 has hit a speed bump. After scaling fresh lifetime highs in late January, the yellow metal corrected sharply as global markets recalibrated interest-rate expectations and the US dollar rebounded. For Indian investors who closely monitor bullion rates, whether for portfolio diversification or as a hedge against volatility, the key question now is not what caused the dip, but what lies ahead.

The trigger for the pullback was a sudden shift in expectations around US monetary policy. When US President Donald Trump nominated Kevin Warsh as the next chair of the Federal Reserve, markets initially interpreted the move as signalling a more hawkish stance. That translated into a stronger dollar and firmer US Treasury yields. Unlike bonds, which pay interest, or dividend-yielding stocks, gold does not generate any regular income. That means when government bond yields rise, investors can earn higher, relatively safe returns elsewhere. As a result, holding gold becomes less attractive because the “opportunity cost” of owning it increases: investors are effectively giving up guaranteed interest income to hold an asset that offers no yield. This tends to put downward pressure on gold prices.

At the same time, gold is priced globally in US dollars. When the dollar strengthens, buyers using other currencies need to spend more of their local currency to purchase the same ounce of gold. This makes gold more expensive outside the United States, which can reduce international demand and further weigh on prices.

The reaction was swift, but it also came at a time when positioning in gold was already stretched. Through 2025, the metal had delivered one of its strongest annual performances in recent memory. According to data cited by the World Gold Council, total global gold demand in 2025 crossed 5,000 tonnes for the first time, while the overall value of demand surged 45% year-on-year to about $555 billion. Gold set more than 50 record highs during the year. In such an overheated environment, even a moderate policy surprise was enough to trigger profit-taking.

Yet, a correction does not automatically invalidate the broader investment case. If anything, the foundations supporting gold remain visible, though they are evolving.

Sovereign Purchases

One structural pillar is central bank buying. The World Gold Council has reported that official sector purchases remained historically elevated in 2025 at over 800 tonnes, even if they were slightly below the previous year’s pace. Countries such as Poland and Kazakhstan were among the largest net buyers, while aggregate full-year net purchases exceeded 300 tonnes.

Indian reports tracking Reserve Bank of India disclosures have also highlighted continued incremental additions to gold reserves as part of diversification away from dollar assets. For retail investors, sustained central bank demand provides a floor that did not exist to the same degree a decade ago.

Investment flows are another crucial driver. Global gold ETFs added hundreds of tonnes in 2025, and January 2026 saw record inflows into physically backed funds, with assets under management rising to fresh highs. Indian market coverage has pointed out that domestic gold ETFs and sovereign gold bond inflows strengthened whenever prices corrected, reflecting a “buy-on-dips” approach among urban investors. This pattern suggests that volatility is being absorbed rather than triggering widespread capitulation.

At the macro level, gold’s trajectory will hinge on two variables: US real interest rates and the dollar’s direction. The late-January rally was fuelled by expectations of US rate cuts and concerns about fiscal sustainability. The subsequent reversal showed how quickly sentiment can change when markets believe policy may stay tighter for longer. If US inflation proves sticky and rate cuts are delayed, gold could remain range-bound or face intermittent pressure. Conversely, any renewed softness in the dollar or a clearer easing cycle could re-energize the rally.

For Indian buyers, there is an added layer: the rupee-dollar equation. Even when international prices cool, a weaker rupee can cushion domestic gold rates. In recent years, currency depreciation has amplified global gains for Indian investors. That dynamic means local prices may not mirror every global correction one-for-one.

Another longer-term theme shaping gold’s outlook is portfolio construction. Since the post-pandemic inflation shock, equities and bonds have at times moved in the same direction, undermining the traditional 60:40 diversification model. Surveys referenced by global banks and carried in Indian financial media show that gold allocations among large fund managers remain modest on average, often below 3%, with a significant proportion reporting zero exposure. Even a gradual shift towards 5%–10% allocations in diversified portfolios could translate into meaningful incremental demand over time.

What Lies Ahead

So what is next for gold?

The most likely near-term outcome is not a smooth upward or downward trend, but heightened volatility. Gold’s recent moves have shown how heavily concentrated investor positions can amplify price swings in both directions. When too many traders are positioned the same way, even small shifts in sentiment or data can trigger sharp rallies as short positions are covered — or equally sharp corrections as profits are taken.

In this environment, short-term price movements are likely to react quickly to each major US data release. Inflation readings can alter expectations about future interest rates; employment data can influence views on economic strength and policy tightening; and even subtle changes in tone from the Federal Reserve can reshape rate-cut or rate-hike expectations. Because gold is highly sensitive to interest-rate outlooks and the dollar, each of these signals can produce outsized market reactions.

In the medium term, however, the broader environment continues to favour gold. Central banks are steadily diversifying their reserves, geopolitical tensions remain unresolved, fiscal deficits across major economies are elevated, and the traditional negative correlation between stocks and bonds has weakened. Together, these factors reinforce gold’s appeal as a hedge and a store of value.

What has changed is the tone of the rally. The earlier phase was driven largely by strong price momentum and investor flows. Now, the market appears to be entering a more measured phase, where prices are reacting more closely to policy signals — particularly interest rates, inflation trends and central bank actions — rather than surging purely on sentiment.

For Indian investors tracking daily rates in Mumbai or Delhi, the message is nuanced. Gold may not replicate the breakneck pace of 2025 immediately, but neither has its strategic relevance faded. In an environment where global growth, geopolitics and monetary policy are all in flux, gold’s role as a portfolio stabilizer remains intact. The rally may have paused, but the forces underpinning demand have not disappeared.

(Cover photo by NEXARO STUDIO on Unsplash)