New Delhi: Global trade growth moderated in mid-2025 but remained positive, with services outpacing goods on the back of firmer prices and stronger activity in developing regions such as East Asia and Africa, according to the latest update from United Nations Conference on Trade and Development (UNCTAD). Against this backdrop, India’s trade performance in the first half of FY26 has held firm, led by exports and underpinned by a structural shift towards electronics, according to NITI Aayog’s Trade Watch Quarterly for Q2, FY 2025-26, released on Friday.

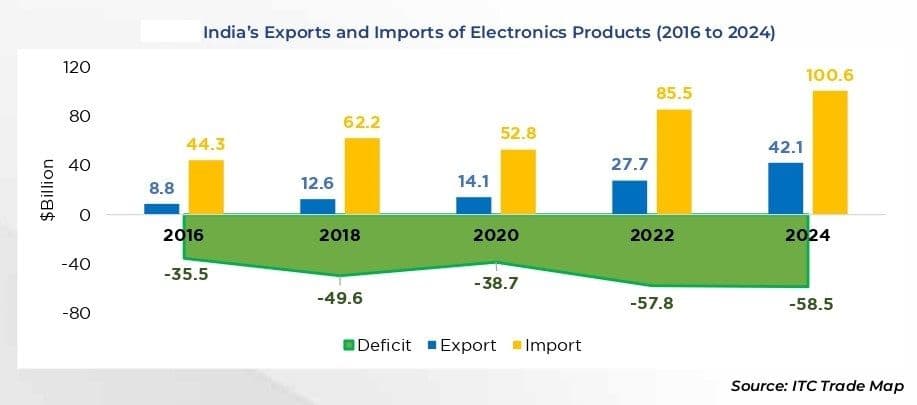

As per the report, India’s total merchandise and services trade rose 5.1% year-on-year during April-September 2025 to $895.1 billion. In the July-September quarter (Q2 FY26), exports emerged as the principal driver, with both merchandise and services exports expanding by about 8.5% year-on-year, outpacing import growth.

The report notes that merchandise exports were buoyed by a sharp 33.4% surge in electrical machinery in Q2, alongside continued strength in mineral fuels, cereals, automobiles and precious stones. Smartphones, non-basmati rice and passenger vehicles were among the key growth drivers. On the import side, mineral fuels, electronics, precious stones and fertilisers dominated the basket. Fertiliser imports registered a striking 239% year-on-year jump in Q2, aided by favourable monsoon conditions that lifted agricultural demand.

India’s trade destinations remained broadly stable, the report says. Exports to top markets grew strongly, led by Hong Kong, China and the United States, while imports from the UAE surged 48% year-on-year. ASEAN markets, however, showed some moderation in export growth.

The report places India’s performance within a broader structural rebalancing of global trade. South-South trade has outpaced South-North trade over the past two decades, with exports among developing economies rising from about $1.8 trillion in 2005 to $7.3 trillion in 2024, exceeding their exports to developed economies. India’s evolving trade profile, the Quarterly notes, aligns with this Global South rebalancing, supported by rising intra-Asia trade, regional value chains and new trade corridors.

E-commerce is identified in the report as a critical enabler of future export growth. India is now among the world’s top six e-commerce markets, with electronics-led online trade gaining momentum. While cross-border e-commerce exports remain modest, they are projected to scale rapidly and could contribute up to a quarter of India’s merchandise exports by 2030, provided regulatory, logistics and MSME-related constraints are addressed.

Focus on Electronics

In the electronics segment, that represented a $4.6 trillion global market in 2024, India’s share in stands at around 1%. Electronics has become India’s second-largest export sector, driven overwhelmingly by mobile phones, which account for 52.5% of the electronics export basket.

Power equipment and wires contribute smaller shares. Export growth between 2015 and 2024 has been concentrated in telecom and mobile phones, while segments such as chips and semiconductors have seen minimal gains.

On the import side, integrated circuits account for 23.7% of India’s electronics imports, followed by mobile phones at 17.5% and data-processing machines at 10.6%. The Quarterly underscores that while India has developed a strong comparative advantage in mobile phone assembly, it remains heavily import-dependent for semiconductors, integrated circuits, batteries and displays that anchor global electronics demand.

Global electronics trade remains highly concentrated in East Asia, with China, Taiwan, South Korea and Vietnam deeply embedded in component-intensive production networks. In contrast, India is positioned primarily as a final-market supplier, exporting finished electronics largely to consumption markets such as the United States, the UAE and the Netherlands, rather than participating in dense intra-Asian processing trade. As a result, the report cautions, India lacks the scale, value addition, technological learning and spillovers associated with deeper integration.

Domestic electronics manufacturing has expanded rapidly but remains concentrated in mobile phones, with gradual diversification into industrial electronics, automotive electronics, components and consumer devices. India’s tariff structure, which is more protective than peers such as China and Vietnam, has supported domestic assembly but raised costs for component-intensive production and weakened integration into global supply chains, the Quarterly observes.

Addressing delegates at the launch of the report, Niti Aayog Vice-Chairman Suman Bery said, “Electronics, as the organising core of modern manufacturing value chains, with semiconductors and components, plays a key role in determining trade balances and technological sovereignty. While India has achieved scale in final assembly, sustained competitiveness will depend on correcting structural cost disabilities, deepening domestic component ecosystems, and leveraging anchor investments in components to embed Indian firms more firmly within global production networks”.

Recent policy initiatives — including the Electronics Component Manufacturing Scheme, the semiconductor mission, customs duty rationalisation and support for e-commerce exports — signal a strategic push to move up the electronics value chain. NITI Aayog’s Trade Watch Quarterly argues that India’s electronics strategy must transition from assembly-led gains to component-led manufacturing, with incentives aligned towards domestic value addition, sustained R&D and ecosystem deepening through anchor investments.

To sustain export momentum and meet the $500 billion manufacturing ambition by FY2030, the report calls for coordinated fiscal, trade and logistics reforms to close structural cost gaps, expanded targeted export financing, predictable domestic procurement and regulatory simplification. While recent free trade agreements have improved external market access, deeper integration into global value chains will be critical.