New Delhi: Women now account for over a quarter of India’s total credit market, and their borrowing is expanding at a pace that is beginning to reshape the country’s financial architecture.

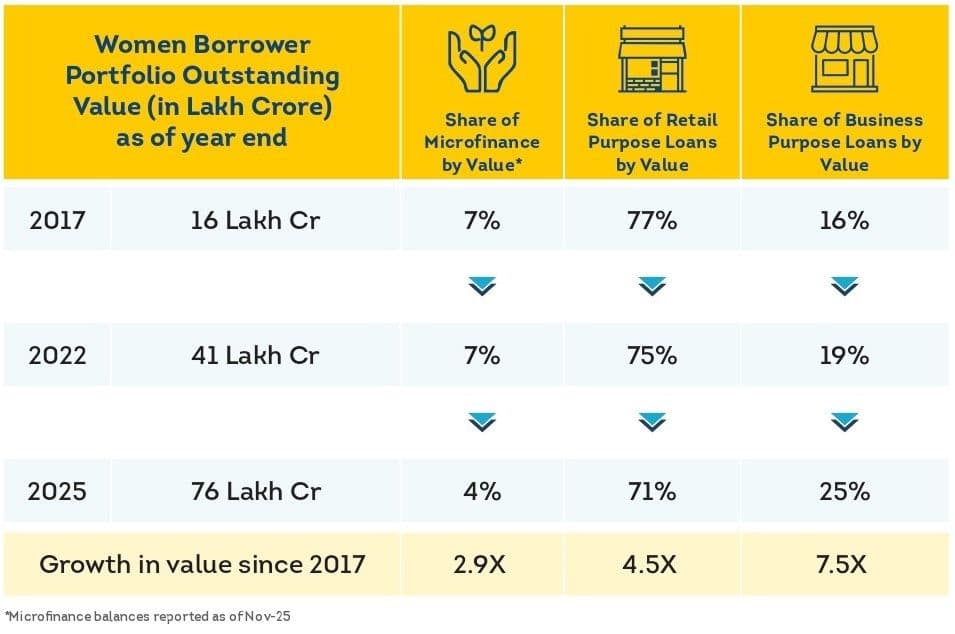

The latest Niti Aayog report, From Borrowers to Builders: Women and India’s Evolving Credit Market, shows that as of 2025 women hold 26% of total system credit, with outstanding loans reaching ₹76 lakh crore, marking a 4.8x increase since 2017. This growth has significantly outpaced the broader credit system, which expanded 2.9x over the same period.

The number of women borrowers has risen steadily at a CAGR of 9%, reaching 16 crore, while credit penetration has nearly doubled from 19% to 36%. These trends point to a structural shift rather than a cyclical expansion, indicating that women are not just participating in India’s credit growth but actively driving it.

The report situates this transformation within a broader transition in India’s financial system, from expanding access to deepening participation. Women are at the centre of this shift, moving beyond basic inclusion into more substantive engagement with formal finance. What emerges is not a story of incremental progress but one of accelerated integration, supported by digitisation, policy alignment, and changing financial behaviour.

“Strengthening women’s economic participation requires attention not only to credit supply, but to the conditions that enable consistent and independent digital engagement. When digital systems are responsive to lived realities, they can accelerate graduation across credit segments and support enterprise resilience,” says Anna Roy, Programme Director, Niti Aayog, and Mission Director, Women Entrepreneurship Platform.

At a macro level, the scale of expansion is striking. Women’s credit portfolios have grown rapidly across segments, with broad-based participation spanning microfinance, retail credit, and business lending. Importantly, this growth is not static. Women are moving along the credit lifecycle, transitioning from entry-level borrowing to more complex and higher-value financial products. This progression reflects both rising financial capability and deeper economic integration.

Microfinance continues to serve as the primary entry point, particularly for low-income borrowers. However, the segment is undergoing recalibration. The number of credit-active microfinance borrowers declined slightly from 7.4 crore in 2022 to 7.3 crore in 2025, reflecting tighter lending conditions amid concerns about overleveraging. At the same time, the share of new-to-credit women in microfinance originations has fallen from 28% to 24%, as lenders prioritise portfolio stability over rapid expansion. This suggests a temporary pause rather than a reversal in financial inclusion, with new-to-credit onboarding emerging as the next critical frontier.

More significant is what follows microfinance. The report identifies a clear graduation pathway, with 19% of microfinance borrowers moving into retail or commercial loans by 2025. This transition is central to the evolving credit ecosystem, indicating that women are not remaining confined to subsistence borrowing but are advancing toward asset creation and enterprise financing.

Retail credit illustrates this evolution clearly. Women’s share of retail loan originations has increased to 27% in 2025, up from 24% in 2022. Consumption-led products remain the primary entry point, with women’s share in consumption loans rising from 16% to 19%, while their participation in gold loans has edged up from 36% to 37%. These products, characterised by lower barriers to entry, act as gateways into formal credit.

However, the deeper shift is visible in asset-backed lending. Women now account for 69% of housing loan originations, up from 63% in 2022. This reflects not only increased access to credit but also growing agency in household financial decisions and asset ownership. Women borrowers also demonstrate stronger credit discipline, with delinquency rates at 0.7x that of the overall borrower base, reinforcing lender confidence and supporting further expansion.

The role of new-to-credit borrowers is particularly important in this segment. Women’s share of new-to-credit retail originations has risen from 28% to 38% between 2022 and 2025. Their entry is largely concentrated in consumption and gold loans, suggesting that immediate household needs continue to anchor early borrowing behaviour, even as longer-term financial trajectories evolve.

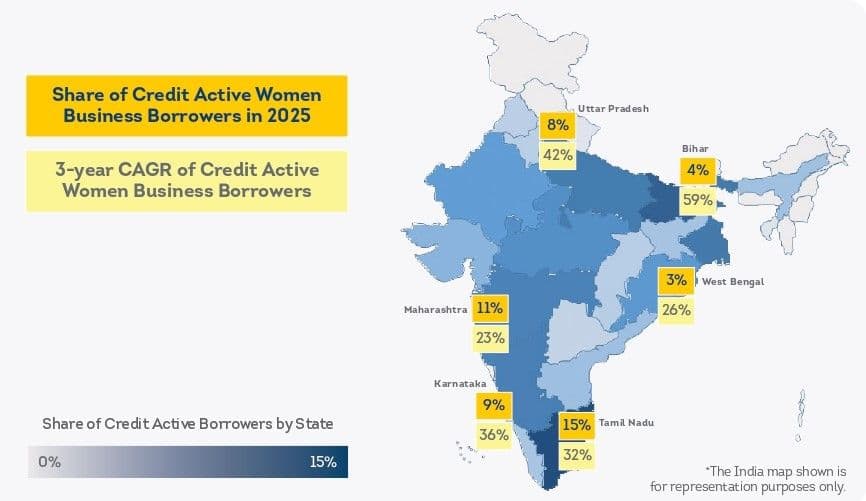

If retail credit reflects stabilisation, business lending represents acceleration. Women entrepreneurs have emerged as the fastest-growing segment within the credit ecosystem. Outstanding balances in business loans have increased 7.5x since 2017, and the number of women with active business loans has grown at a CAGR of 31% over the past three years, compared to 17% for overall commercial credit. By 2025, 1.6 crore women entrepreneurs hold active business loans, up from 1 crore in 2023.

This growth is geographically uneven but increasingly dispersed. While southern and western states continue to dominate in absolute terms, northern states such as Bihar and Uttar Pradesh are witnessing the fastest growth, with CAGRs of 59% and 42% respectively. This divergence suggests that traditional credit markets are maturing, while new regions are entering a phase of rapid expansion.

Despite this progress, the report highlights a gap between access and depth. Only 27% of women entrepreneurs access credit through formal business entities, and just 4.3% use advanced financial products such as cash credit or overdraft facilities, compared to around 40% overall. This indicates that while entry barriers are declining, progression into more sophisticated financial instruments remains limited.

Digitisation emerges as the central enabling force behind these trends. India’s digital public infrastructure, particularly Aadhaar-based KYC and UPI, has transformed credit access by reducing onboarding friction and creating verifiable financial trails. The rapid expansion of digital payments has provided lenders with the data needed for modern credit underwriting, reducing information asymmetry and enabling faster decision-making.

The impact is evident in loan processing times. Same-day approvals for consumption loans have increased from 34% in 2022 to 45% in 2025, while same-week approvals in commercial lending have risen from 24% to 30%. Speed, in this context, is not just an operational improvement but a structural enabler, particularly for first-time borrowers navigating formal financial systems.

However, digital adoption remains uneven. Among rural women nano-entrepreneurs, while 60% to 70% accept digital payments, engagement is often limited to basic transactions. Factors such as time constraints, trust networks, and limited decision-making autonomy influence how women interact with digital tools. This underscores a key insight: access to digital infrastructure does not automatically translate into meaningful financial participation.

India is entering a new phase of financial inclusion, defined not by how many women enter the system but by how far they progress within it, says the report. With an estimated 45 crore credit-eligible women, the opportunity remains vast. The “The next phase of inclusion will be defined not by how many women enter the system, but by how

steadily they progress within it. Enabling that progression will be central to deepening India’s entrepreneurial base and sustaining long-term economic growth,” says Roy.

(Cover photo by Dileesh Kumar on Unsplash)