New Delhi: After a robust close to 2025, the momentum of deal-making in India’s banking sector lost pace significantly in the first quarter of 2026, as global headwinds including geopolitical tensions, tariff-related pressures and the ongoing conflict in West Asia weighed on investor sentiment and tempered capital deployment. The absence of large-ticket transactions further dragged overall activity, even as stable domestic fundamentals such as low inflation and steady growth offered some support to the sector.

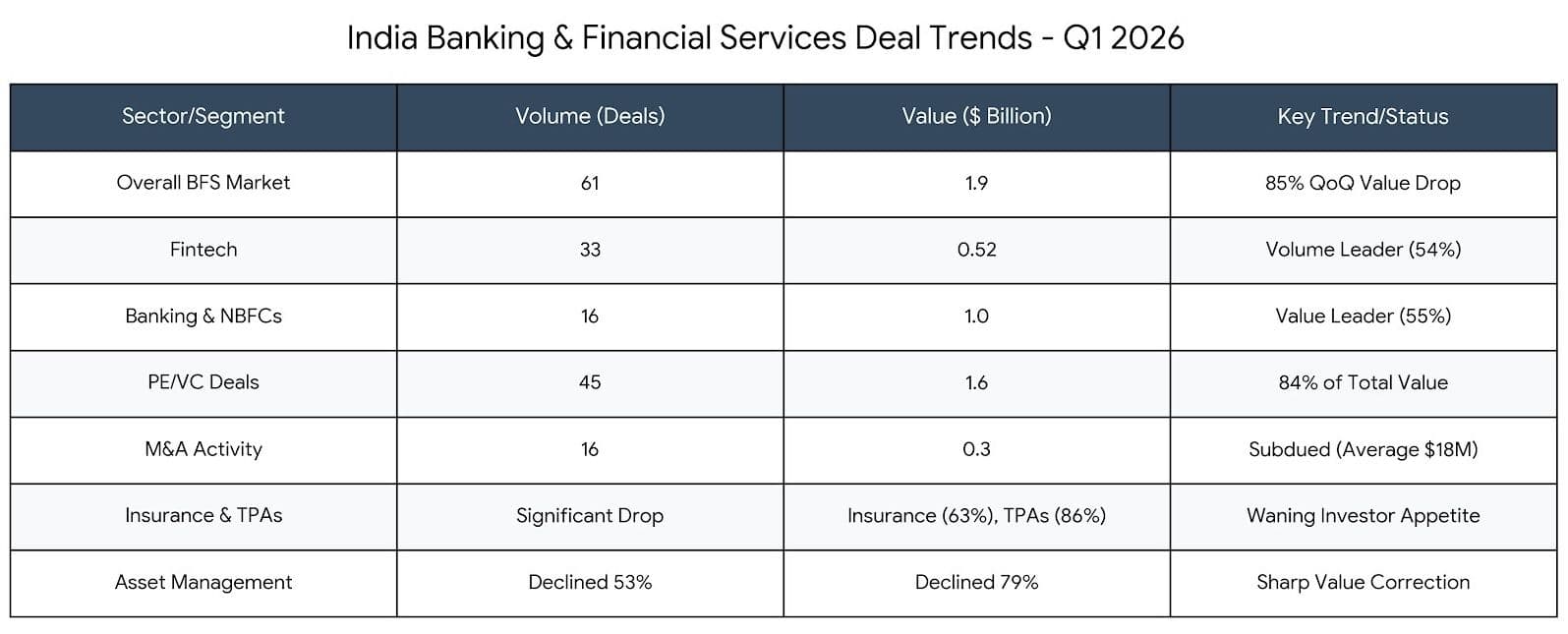

According to the Grant Thornton Bharat Banking Dealtracker, the sector recorded 61 deals worth $1.9 billion during the quarter, excluding IPO and QIP transactions. This marked a 6% year-on-year decline in volumes and a steep 62% drop in value. On a sequential basis, the slowdown was sharper, with deal volumes and values falling 25% and 85%, respectively, compared to Q4 2025.

The report attributed this decline primarily to the absence of billion-dollar transactions. Only four deals exceeded $100 million in Q1, contributing around $0.8 billion, a stark contrast to $11.7 billion generated by 19 such deals in the preceding quarter. Including public market activity, total deal volumes stood at 63 transactions worth $2 billion, representing a 30% decline in volumes and a 90% drop in values quarter-on-quarter, making it one of the weakest quarters since Q3 2023.

Vishal Agarwal, Partner and Private Equity Group & Deals Structuring Leader, Grant Thornton Bharat, said, “Q1 reflects a continuation of cautious sentiment shaped by global headwinds, including geopolitical tensions, tariff-related pressures and the ongoing conflict in West Asia. While India’s macro fundamentals remain stable with low inflation and steady growth, capital markets have remained measured, influencing the pace of transactions.”

“The Union Budget 2026 has taken steps in the right direction through proposed reforms such as easing foreign investment norms and deepening the bond market, which could support deal activity over time. However, in the near term, private capital deployment is expected to remain selective until there is greater clarity on global conditions, particularly around energy prices and geopolitical stability,” he added.

Sectoral Divergence

The sectoral composition of deal activity reveals a clear divergence between volume-led and value-led segments. Fintech emerged as the most active segment by deal count, accounting for 33 transactions or 54% of total volumes, though aggregate value stood at a relatively modest $518 million. The trend underscores a shift towards smaller, early- to mid-stage investments, even as sequential momentum moderated.

In contrast, banking and NBFCs dominated in value terms, contributing $1 billion, or 55% of total deal value, across 16 transactions. This reflects continued investor confidence in credit-driven platforms and the resilience of traditional financial institutions, despite the broader slowdown.

Other segments witnessed sharper corrections. Insurance and TPAs saw deal volumes and values decline significantly by 63% and 86%, respectively, indicating waning investor appetite in the absence of compelling large-scale opportunities. Similarly, financial services and asset management segments experienced declines of 53% in volumes and 79% in value, highlighting the impact of fewer marquee transactions during the quarter.

M&A Weakness & PE Resilience

The GTB report points to a particularly subdued quarter for mergers and acquisitions. M&A activity fell to 16 deals worth $0.3 billion, marking the lowest quarterly value since Q1 2025. The absence of large transactions led to a sharp compression in average deal size, which dropped from $333 million in Q4 2025 to just $18 million in Q1 2026. Domestic deals dominated, accounting for 81% of volumes, while inbound transactions, though limited in number, contributed a disproportionately higher share of value.

Notably, there were no M&A deals exceeding $100 million. The largest transaction during the quarter was DWS Group GmbH & Co. KGaA’s acquisition of a 40% stake in Nippon Life India AIF Management Ltd at approximately $81 million, followed by BillDesk’s acquisition of Worldline’s India operations for $71 million. The lack of disclosed deal values for nearly half of all transactions further suppressed overall value metrics.

Private equity and venture capital activity, while also moderating, remained the primary driver of deal-making. The quarter saw 45 PE/VC deals worth $1.6 billion, accounting for 74% of volumes and 84% of total deal value. Despite the sequential decline, the segment performed better on a year-on-year basis compared to Q1 2025, indicating sustained long-term investor interest. Investment patterns were skewed towards smaller deals below $50 million, reflecting a more cautious and selective deployment strategy.

The largest PE deal of the quarter was Indriya Ltd’s acquisition of a 14% stake in Aditya Birla Housing Finance Ltd, signalling continued traction in the banking and NBFC space.

While India’s financial services sector continues to attract capital, the near-term outlook remains tempered by global uncertainties and a cautious investment approach, says the GTB report. Sectoral trends indicate resilience in core lending businesses and fintech innovation, but the absence of large deals continues to weigh heavily on aggregate deal values, it adds.

(Cover photo by Amina Atar on Unsplash)