New Delhi: The global economic landscape, which had begun to show signs of a steady post-pandemic reflation, has been abruptly jolted by the escalating conflict in West Asia.

The war between Iran and Israel-US combine has moved beyond a localized skirmish, threatening the stability of the world’s most critical energy arteries. For India, a nation that imports nearly 90% of its crude oil requirements, the stakes could not be higher. The crisis is not merely a geopolitical event but a systemic macro-economic shock that is already rippling through the country’s twin deficits, currency markets, and corporate profit margins.

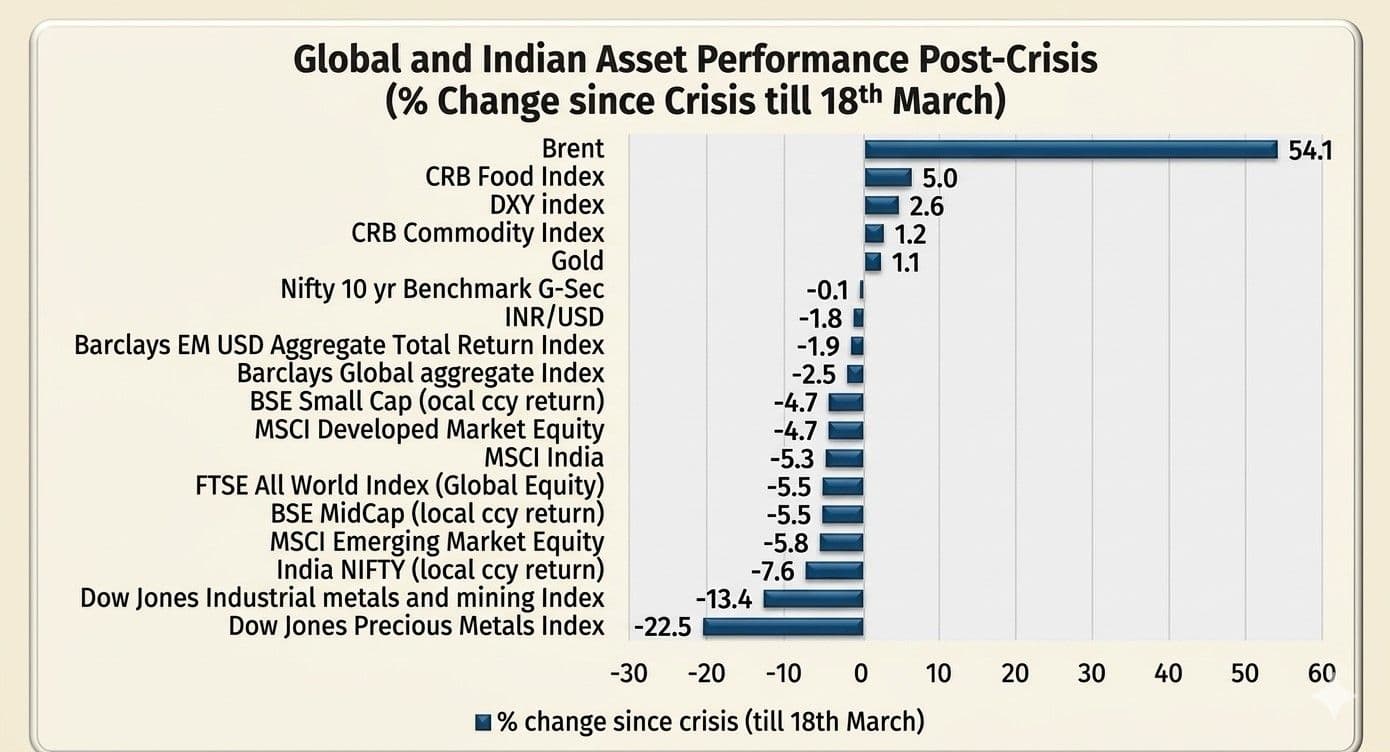

The era of the “peace dividend” has officially been incinerated. According to the SBI Funds Management report, 2026 Middle East Conflict and Its Implications, geopolitical risk has mutated from a peripheral concern into a primary, material threat to India’s financial stability. With the Strait of Hormuz — the world’s most vital energy artery — facing a practical shutdown, the strategic calm that anchored the last decade of growth has evaporated, leaving the Indian economy exposed to a volatile new reality.

Energy Shocks and the Twin Deficit Strain

The primary transmission channel for this crisis is the energy tax levied by surging crude prices. Brent crude, which hovered around $70 per barrel in late February, surged past the $110 mark in March, with some scenarios projecting a climb toward $137 if hostilities persist. This surge exerts immediate pressure on India’s current account deficit (CAD).

“Geopolitical factors have re-emerged as a material risk factor for financial markets with the recent war in the Middle east. A prolonged conflict will put pressure on India’s twin deficits and drive rupee weaker. Impact on WPI inflation and hence corporate profit margin will be sharper than the retail inflation which could have an initial layer of shock absorber from the OMCs and then possibly via fuel tax cut,” the report says.

Statistically, the impact is mathematical and unforgiving. Research estimates suggest that for every $10 per barrel increase in crude oil prices, India’s CAD widens by approximately 36 basis points. In a high-price scenario where oil sustains near $100-$110, the annual deficit could widen by as much as $70 billion. This external strain is compounded by a weakening fiscal balance.

While the 2026 Union Budget focused on quality expenditure and a 7.7% growth in total spending, the rising cost of energy and gas has sent the fertilizer subsidy bill skyrocketing. Urea prices have jumped nearly 50% since December 2025, potentially forcing a ₹300 billion upward revision in government subsidies.

“A prolonged disruption of Persian Gulf oil and gas exports could mean return to 2022-style energy prices which would have clear macro and market implications. In this scenario, inflation rises worldwide, more so in Europe and Asia. The deterioration in terms of trade for India becomes quite stark with rising crude oil prices,” says the report.

Currency Volatility and Shift in Monetary Policy

The Indian Rupee, a traditional barometer of external health, has found itself in the eye of the storm. Currently trading at ₹93 per US dollar, the currency is facing dual pressure from a rising Dollar Index — fuelled by safe-haven demand — and sharp capital flight. In March alone, foreign institutional investors (FIIs) pulled out nearly $11.8 billion, marking one of the largest monthly exits in recent history.

Analysts have revised their depreciation expectations for the rupee to 4-5% for the year, up from an earlier estimate of 2-3%. If the conflict sustains, the currency could test the ₹96 mark over the next two quarters. This creates a vicious cycle of imported inflation, where the cost of everything from electronics to industrial raw materials rises simply because the currency buys less.

According to the report, “Monetary policy easing in the current cycle has possibly reached its end, with focus now likely to be on rates transmission. The recent geopolitical developments add an additional layer of risk on the overall macro environment with possible upside inflation pressures if crude prices were to stay elevated. This would also impact RBI's reaction function in various market segments.”

The Reserve Bank of India (RBI) has been forced into a defensive crouch. While the central bank has intervened aggressively, selling billions in forex reserves to anchor yields, the higher for longer interest rate regime now seems inevitable. The market’s hope for a rate cut cycle in early 2026 has been replaced by the realization that the RBI must prioritize currency stability and inflation management over growth-oriented easing.

Remittance Cushion and Resilience Strategy

Despite the gathering clouds, India possesses structural buffers that prevent a 1991-style crisis. A significant silver lining remains the country’s robust inward remittances. India is expected to receive between $140 billion and $145 billion in FY26, a 15% increase over previous years. However, even this buffer is being watched closely, as 38% of these inflows originate from the Gulf Cooperation Council (GCC) countries.

“Remittance inflows are also likely to be affected, as about 38% of total inward remittances originate from the Middle East, half of which come from the UAE alone. Despite a structural improvement in India’s current-account dynamics and a CAD that has remained below 2% of GDP since FY15 (except FY19 at 2.1%), India's balance-of-payments position has weakened materially due to near-zero net FDI inflows,” notes the report.

To navigate this new normal, the Indian economy must rely on its diversified energy sourcing, the report suggests. Since 2022, India has strategically shifted its import basket to include over 40 countries, significantly increasing its intake from Russia. This diversification acts as a vital shock absorber, preventing a total supply-side collapse. Furthermore, the 2026 Union Budget’s emphasis on infrastructure expansion, with a 17% growth in broad infra spending, provides a long-term growth floor that may help the country weather the immediate storm.

The West Asia conflict has ended the era of easy macro for India. The path forward requires a nimble policy response: a combination of fiscal discipline to manage the subsidy burden and a vigilant monetary policy to protect the Rupee. While India remains relatively insulated compared to its peer emerging markets, the “Orcus of inflation”, as described by market veterans, is once again at the door, demanding a disciplined and strategic response from policymakers and investors alike.