New Delhi: India’s fertiliser sector is heading into FY27 under mounting pressure as the West Asia conflict disrupts global supply chains, inflates raw material costs and threatens to stretch the Centre’s subsidy budget well beyond projections. The CareEdge Ratings’ latest report, Fertiliser Sector: Impact of West Asia Crisis on Availability & Subsidy Budget, warns that the country’s growing dependence on imported fertilisers and feedstock has sharply increased vulnerability to geopolitical disruptions around the Strait of Hormuz.

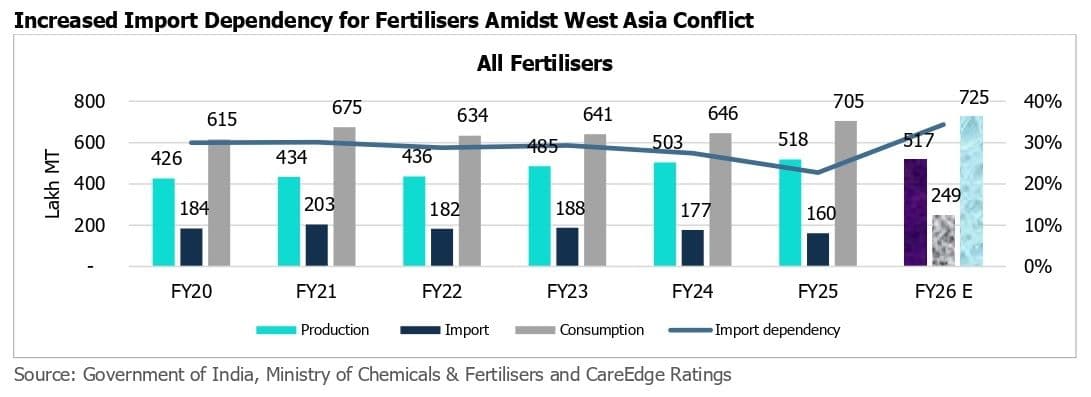

According to the report, India’s fertiliser import dependency rose materially to nearly 34% in FY26 from 23% in FY25 as domestic production weakened and consumption continued to rise. The shift comes at a sensitive juncture for the agriculture economy, with the upcoming Kharif season expected to witness healthy sowing demand despite forecasts of a below-normal monsoon at 92% of the long period average.

The report says ammonia prices have surged nearly 60% since March 2026, while sulphur prices climbed around 50%, sharply escalating production costs for fertiliser manufacturers. India imports more than 80% of its ammonia and sulphur requirements from Gulf nations, making the sector highly exposed to shipping disruptions and freight volatility arising from the West Asia conflict.

“After a steady performance for three years ending FY26, the fertiliser sector is entering FY27 amid a challenging operating environment. The ongoing West Asia geopolitical crisis led to a sharp rise in the prices of natural gas and other key inputs for urea and complex fertilisers. The Strait of Hormuz remains a critical chokepoint, with approximately one-third of the global seaborne fertiliser trade and around one-fifth of oil & LNG volumes passing through it,” said Rabin Bihani, Associate Director, CareEdge Ratings, in the report.

Imports Expose Structural Weakness

The sharpest stress is visible in urea and Di-Ammonium Phosphate (DAP), two of India’s most critical crop nutrients. The report says urea import dependency has climbed back to nearly 29-30% in FY26 after easing in recent years due to domestic capacity additions. Imports are estimated to have jumped to around 115 lakh metric tonnes during FY26 to build strategic buffers ahead of the Kharif season.

West Asia remains central to this supply chain. In FY25, nearly 73% of India’s urea imports originated from Oman, Qatar, Saudi Arabia and the UAE. Although Chinese exports resumed partially during FY26, dependence on Gulf suppliers remains elevated.

DAP presents an even bigger challenge. According to the report, India’s DAP import dependency is estimated to rise to 68% in FY26, the highest level in recent years. Saudi Arabia alone accounted for 40% of total DAP imports during the first 10 months of FY26.

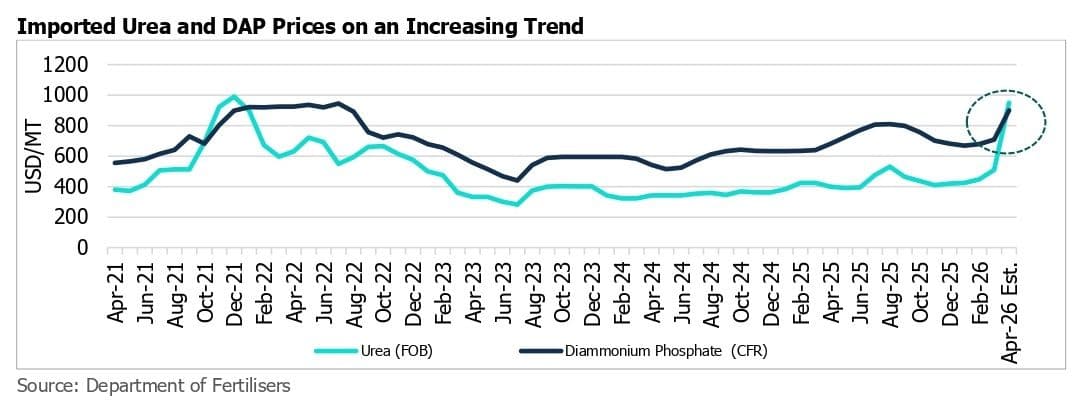

The economics of DAP imports have deteriorated sharply. International DAP prices have climbed to nearly $900 per metric tonne, almost double pre-conflict levels. Yet the maximum retail price remains capped at Rs 27,000 per metric tonne, leaving importers with significant under-recoveries even after government support.

“Given the current situation, international DAP prices have risen to around $900/MT, or about Rs 83,500/MT at current exchange rates, which is nearly double the levels seen before the West Asia conflict. However, with MRP fixed at Rs 27,000/MT and subsidy at Rs 30,000/MT, imports remain economically unviable,” says the report.

The report further notes that the Centre’s additional DAP support package of Rs 3,500 per metric tonne still leaves companies facing under-recoveries of nearly Rs 23,000 per metric tonne, intensifying pressure on both profitability and availability.

Subsidy Arithmetic Heads For Blowout

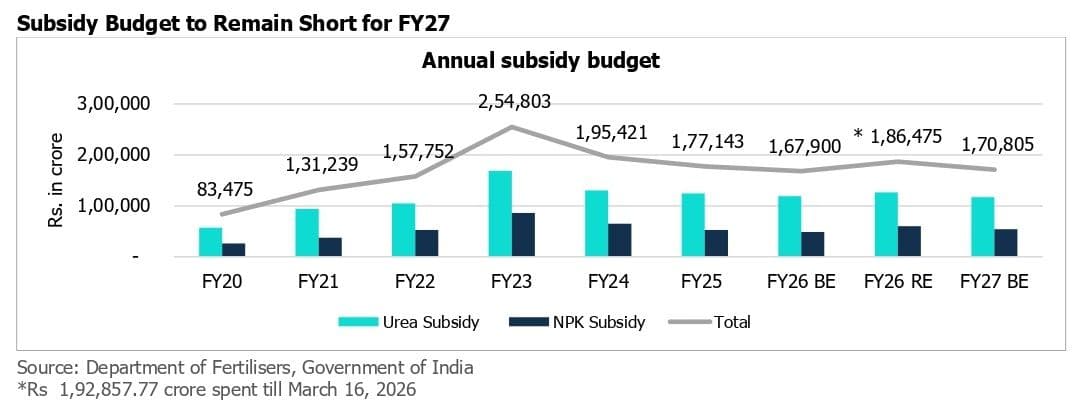

The fiscal implications are now emerging as a major concern for the Union government. After touching a record Rs 2.55 lakh crore in FY23, fertiliser subsidies had moderated over the past two years as commodity prices cooled. However, the latest geopolitical flare-up has reversed that trajectory.

The CareEdge report says FY26 subsidy outgo is already likely to exceed the revised estimate of Rs 1.86 lakh crore by more than 10%. For FY27, the Centre has budgeted Rs 1.71 lakh crore towards fertiliser subsidies, including Rs 1.17 lakh crore for urea and Rs 54,000 crore under the nutrient-based subsidy regime.

That allocation now appears increasingly inadequate amid soaring import costs for natural gas, ammonia and finished fertilisers. Spot imported natural gas prices reportedly surged from around $10 per mmbtu to above $15 per mmbtu in April 2026, sharply increasing production costs for domestic urea manufacturers.

“Timely subsidy releases in recent years have reduced receivable build-up and supported working capital management of fertiliser companies. Hence, the sector is better placed to absorb volatility in input prices. Relatively comfortable reservoir levels and a better inventory position offer a near-term cushion for the Kharif sowing season,” said Hardik Shah, Director, CareEdge Ratings.

The report, however, cautions that elevated prices and any delay in subsidy disbursals could increase sector borrowings significantly and put pressure on working capital cycles across fertiliser companies.

Stocks Offer Relief, But Risks Remain

Despite the mounting cost pressures, the immediate supply outlook for the Kharif season appears relatively stable. According to the report, fertiliser inventories as of April 2026 stood at nearly 49% of estimated Kharif requirements, significantly above the normal level of 33%. That inventory cushion could help prevent a near-term supply squeeze even if shipping disruptions continue.

Still, the report underlines that shipment timing, logistics bottlenecks and product-specific shortages remain critical variables. Any prolonged escalation in the West Asia conflict could sharply impact availability, particularly because the fertiliser sector remains heavily dependent on imported gas and raw materials routed through the Gulf region.

The report says the sector is entering this volatile phase from a relatively stronger financial position due to improved subsidy release mechanisms over recent years. Yet rising import dependence, volatile commodity prices and weather uncertainties linked to the monsoon could together keep the fertiliser industry under sustained pressure through FY27.

With fertiliser demand expected to remain firm and retail prices politically difficult to raise, the government may once again be forced to absorb the bulk of the cost escalation — setting the stage for another year of supplementary subsidy allocations and heightened fiscal strain.

(Cover photo by Gowtham AGM on Unsplash)