New Delhi: The collapse of recent high-stakes diplomatic negotiations in Islamabad has effectively extinguished the hope of a “de-escalation” baseline of the Iran-Israel war. What was once a localized regional conflict has now breached the gates of world trade, forcing a definitive shift in the global economic trajectory.

For India, the transition from a stable growth path (‘base case’ scenario) to a high-risk ‘alternative case’ scenario is no longer a matter of if, but when. This pivot is necessitated by a conflict that has moved from the periphery to the core of global energy infrastructure. The Crisil’s Economic impact of West Asia Shock report outlines a stark blueprint for this new reality. As supply lines tighten and the cost of basic commodities surges, the transition to an alternative economic framework has become an urgent, unavoidable necessity for policymakers and industry alike.

Breakdown of the ‘Baseline’

The original projections for the current fiscal year have been rendered obsolete by the sheer scale of the disruption in West Asia. The report confirms that the situation has deteriorated significantly beyond early expectations. “The West Asia conflict is expanding in scale, casting a growing shadow over shipping, energy supply, trade and economically critical infrastructure. This multidimensional crisis is taking its biggest toll on energy prices and supply. To be sure, this is the largest energy shock on record,” it says.

This escalation has crippled the primary arteries of global commerce. Specifically, “only selective passage is allowed through the Strait of Hormuz, which transports 20% of global oil”, and critically, “the world’s largest LNG facility in Qatar has been partially destroyed and shut”.

Under this ‘alternative case’ scenario, the global and domestic energy landscape is unrecognizable compared to the start of the year. The Crisil report notes that “S&P Global views this as the largest energy shock on record, beginning to constrain supplies”. For a nation that imports the vast majority of its energy, the destruction of infrastructure in West Asia is a direct hit to the domestic treasury. The report highlights that Brent crude oil is expected to average $82-87 per barrel in fiscal 2026 in the alternative case, marking a 23% on-year rise. This price hike is compounded by logistical nightmares, as rerouting ships around the Cape of Good Hope adds 19 to 33 days to the journey time, leading to a situation where tanker shortages are acute.

Growth Under Pressure

The transition to the alternative case carries a heavy price tag for India’s GDP and fiscal health. The optimism of a 7.1% growth rate has been tempered by reality. According to the report: “In the alternative case, India’s real GDP growth is expected to slow to 6.8% from 7.1% in the base case.” This deceleration is largely due to the negative impact of high crude oil and gas prices on manufacturing, construction, and services sectors such as travel and transport. Furthermore, the report warns that export growth will be 2% in the alternative case, lower than 3% in the base case, as global demand weakens and trade disruptions persist.

The fiscal deficit and the value of the rupee are also in the line of fire. The current account deficit (CAD) is expected to widen to 2.0% of GDP in the alternative case, up from 1.2% in the base case, primarily due to a higher petroleum import bill, says the report.

This pressure is also reflected in the currency markets, where the rupee is expected to remain under significant strain. The report projects that the rupee is expected to remain under pressure and average 92.5 per US dollar in March 2027, adding that exchange rate volatility could remain high in the alternative case. This necessitates a vigilant stance from the Reserve Bank of India, as the central bank is expected to use its foreign exchange reserves “to manage” the volatility.

Sectoral Vulnerability

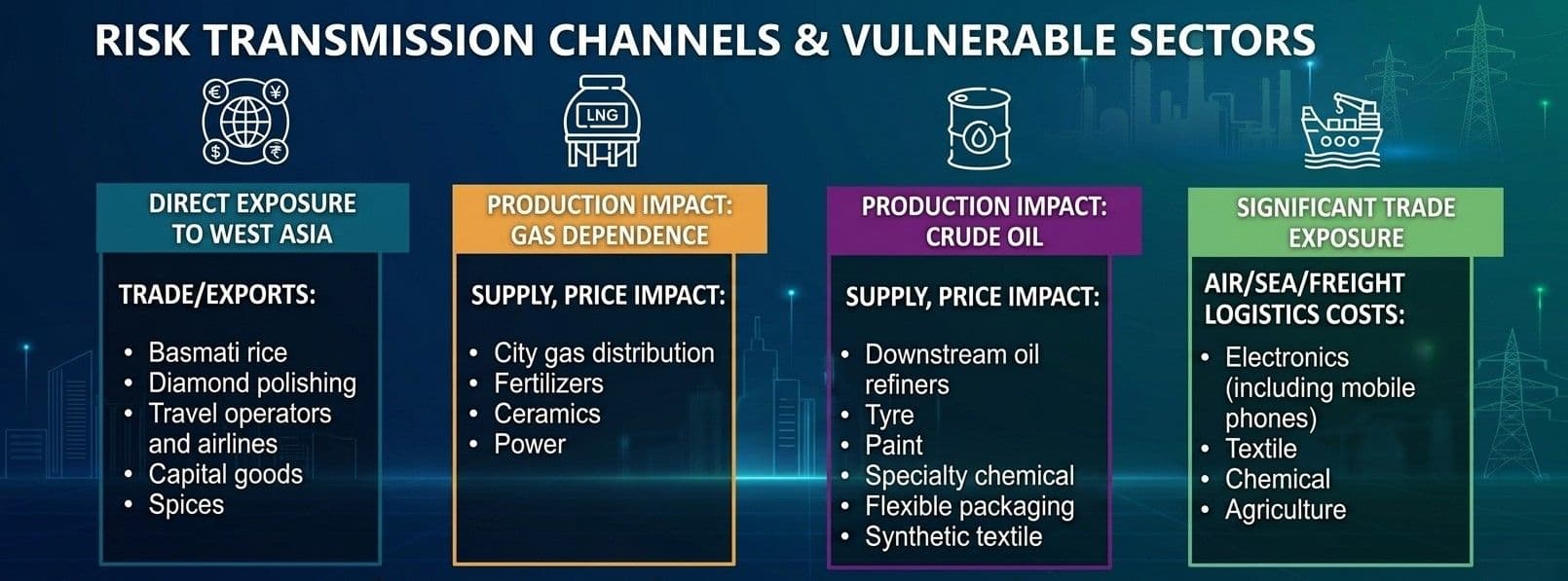

Perhaps the most visceral impact of the alternative scenario is found in the supply chains of essential commodities. India’s reliance on the Strait of Hormuz for its gas requirements is a critical vulnerability. India is highly dependent on the Strait of Hormuz for its gas requirements, as 85-95% of LNG imports pass through it. “India does not have a national buffer for LPG and LNG,” the report says.

While the government has sought to shield the common man, the industrial sector is paying the price. “The government is prioritizing LPG and LNG supply for households and the transport sector, keeping retail prices unchanged. This means industrial and commercial users are facing the brunt of shortages and price hikes,” says the report.

The agricultural sector, the backbone of the Indian economy, is equally exposed. West Asia accounted for more than 40% of India’s fertilizer imports in the last few years. Within this, West Asia accounted for approximately 65% of urea shipments to India in fiscal 2025. The report warns of impending shortages, saying: “While the current stock of fertilizers is sufficient for the next 2.5 months, a prolonged conflict will impact the procurement of fertilizers for the Rabi crop.”

This creates a domino effect where energy shortages lead to fertilizer shortages, which eventually culminate in reduced food security and inflationary pressure on the common citizen.

Building a Strategic Fortress

As India moves deeper into this alternative scenario, the focus must shift from crisis management to long-term structural fortification. The report suggests that the only way to mitigate these shocks is through aggressive diversification and the building of strategic reserves.

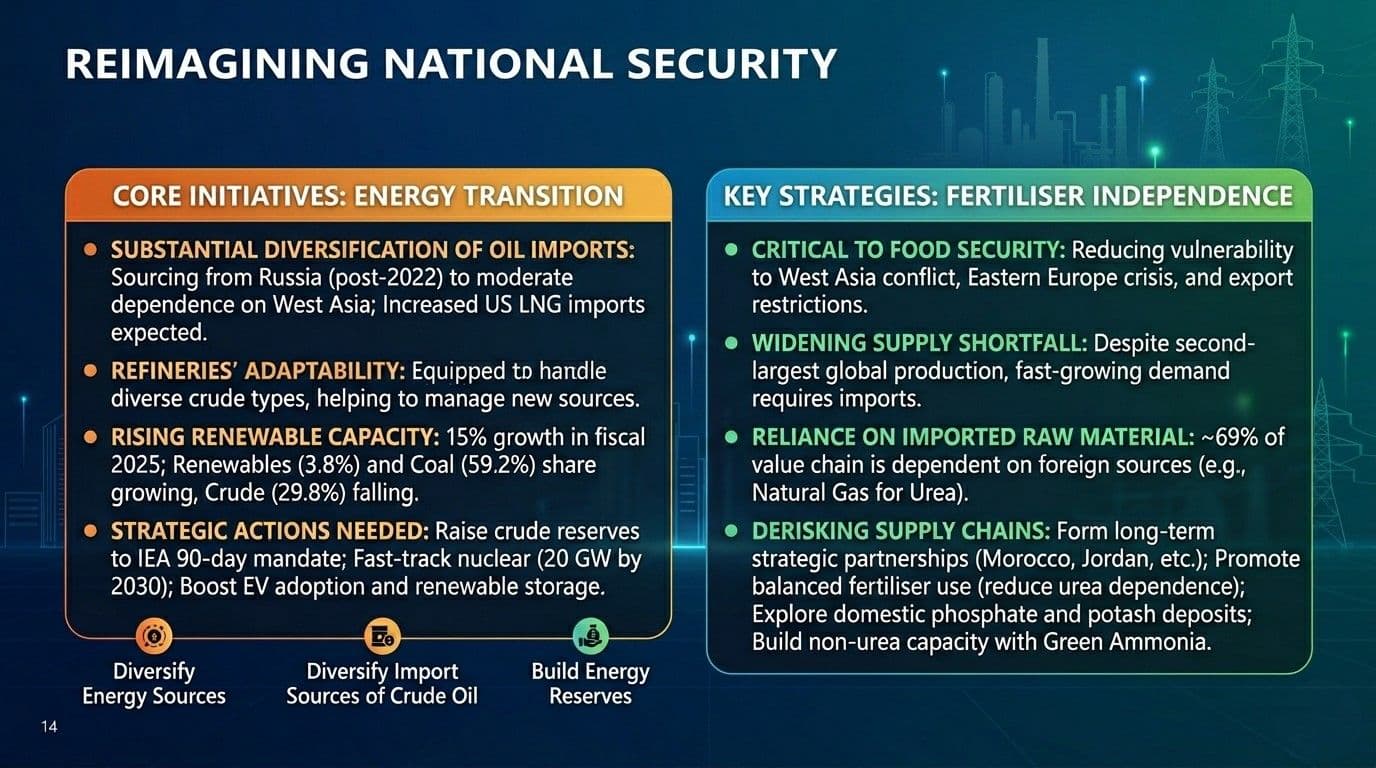

According to the Crisil report, India has already increased its oil imports from Russia, which accounted for approximately 40% of India’s oil imports in fiscal 2025. This has reduced India’s dependence on West Asia. However, the report is clear that more must be done. “To enhance energy security, India needs to increase its strategic petroleum reserves to 90 days of net imports as recommended by the IEA,” it says.

The transition also highlights the critical need for a faster shift toward green energy. “India’s renewable energy capacity grew 15% in fiscal 2025. Accelerating the transition to renewable energy and green hydrogen will reduce India’s dependence on fossil fuel imports in the long run,” the report says.

In the fertilizer sector, the report advocates for securing long-term supply contracts with countries outside West Asia and promoting the use of nano-fertilizers and green ammonia.

To sustain its growth story, India must treat this transition not as a temporary hurdle, but as a fundamental shift in the global order that requires a reimagining of national economic security. “Efficiency and resilience will be the key to navigating this period of high volatility and ensuring that the Indian economy remains on a stable growth path despite the global headwinds”, says the report.

(Cover photo by Ian Simmonds on Unsplash)