New Delhi: Jolted by the ongoing geopolitical upheaval in West Asia and global capital volatility, India’s financial system has slipped into its most stressed phase since the Covid pandemic, says Crisil’s Macroeconomics First Cut report.

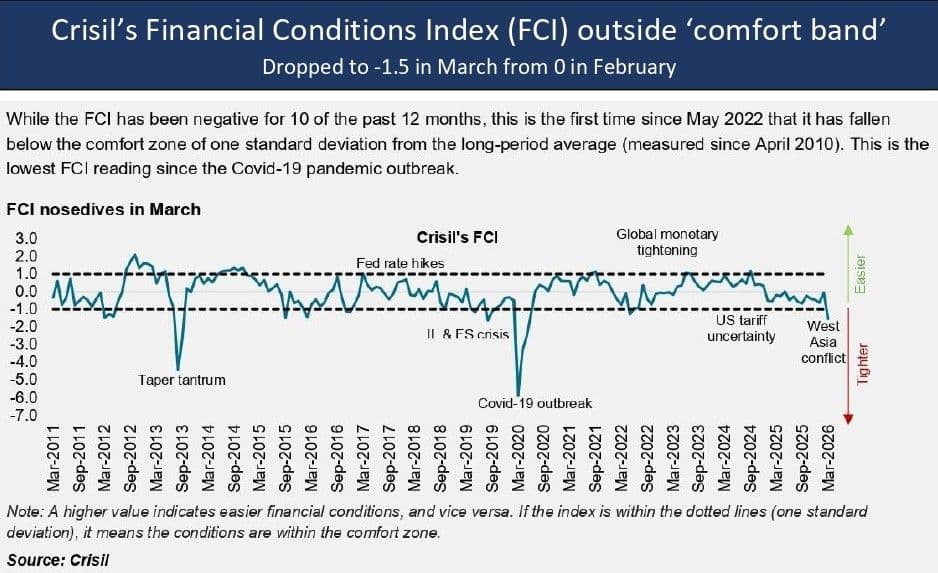

In March, Crisil’s Financial Conditions Index (FCI) plunged to -1.5 from 0 in February, breaching its comfort band for the first time since May 2022 and marking its lowest reading since the Covid outbreak. The deterioration is not episodic; it reflects sustained stress, with the index remaining negative for 10 of the past 12 months.

At the heart of this tightening lies the West Asia war, which triggered a chain reaction across markets. A surge in crude oil prices, heightened global risk aversion, and a flight of foreign capital combined to tighten liquidity, weaken the rupee and push bond yields higher. Financial markets reacted sharply, even as real sector indicators have yet to fully reflect the stress, underscoring how external shocks are rapidly transmitting into India’s financial system.

Notably, the stress has been broad-based, with multiple segments of the financial system simultaneously shifting into adverse territory, indicating a more systemic tightening rather than a sector-specific disruption.

Capital Flight, Currency Stress & Market Turbulence

The Crisil report highlights an aggressive pullback by foreign investors as the most immediate transmission channel. Foreign portfolio investors (FPIs) recorded net outflows of $13.6 billion in March, the largest monthly exodus since the pandemic. This reversed a $4.2 billion inflow in February and took total FPI flows in fiscal 2026 to a net outflow of $16.6 billion, compared with an inflow of $2.7 billion the previous year. Importantly, the bulk of these outflows came from equities, which saw record selling, signalling heightened risk aversion among global investors toward growth-linked assets.

Equity markets bore the brunt. The Sensex fell 8.4% in March — the steepest monthly decline since COVID — while volatility spiked, with the NSE VIX jumping to 22.1 from 13.0, its highest since May 2022.

Currency pressures intensified in tandem. The rupee depreciated 2.2% on average in March — the sharpest monthly fall since October 2022 — sliding to an average of 92.8 per dollar and touching 94.7 by month-end. A broad-based strengthening of the dollar, driven by safe-haven demand, compounded the pressure, although subsequent regulatory measures by the Reserve Bank of India helped limit further depreciation into April.

Debt markets were no less affected, says the report. The 10-year government security yield rose above 7% for the first time since July 2024, ending March at 7.02%, up 36 basis points. Fiscal concerns, stemming from fuel tax cuts and higher fertiliser subsidies amid rising crude, added to the upward pressure.

The trigger for much of this turbulence was oil. Brent crude surged from $71.1 per barrel in February to $103.7 in March, even touching $121 at month-end, amplifying macroeconomic vulnerabilities for an import-dependent economy.

Liquidity Tightens Despite Policy Cushion

Even as systemic liquidity remained in surplus, the cushion narrowed, notes the Crisil report. The Reserve Bank of India (RBI) absorbed liquidity equivalent to 0.6% of net demand and time liabilities in March, compared with 0.9% in February, reflecting both global outflows and domestic tax-related drains. At the same time, the central bank conducted open market operations worth Rs 1.8 lakh crore, preventing a sharper tightening in financial conditions.

Money market conditions tightened accordingly. The weighted average call money rate rose to 5.2%, and briefly exceeded the repo rate in late March. Short-term borrowing costs climbed, with six-month commercial paper rates rising to 7.68% and certificates of deposit to 7.27%.

Yet, the tightening was not uniform across the system. Credit growth remained relatively resilient at 13.8% year-on-year as of mid-March, supported by strong demand in services (16.3%) and personal loans (15.2%). Lending rates also stayed benign, with housing loans at 8.35% and auto loans at 8.95%, both below pre-pandemic levels.

This divergence — tight financial conditions alongside steady credit growth — suggests that while markets are under stress, domestic demand drivers have not yet fully weakened, highlights Crisil in the report.

Economists Flag Fragility, Policy Agility

The Crisil report strikes a cautious tone on the outlook. Economists see a clear downside risk to growth and upside risk to inflation, driven by elevated oil prices, global uncertainty and potential weather-related shocks such as a weak monsoon. The synchronised tightening across financial segments also signals that the current episode may be more persistent than earlier bouts of volatility, keeping financial conditions under pressure for longer.

The policy response, therefore, must remain agile. The RBI has already held rates steady while signalling a proactive approach to liquidity management. Its commitment to ensuring adequate liquidity and using multiple instruments, from open market operations to forex regulations, has helped stabilise markets in the short term. Measures such as curbs on speculative forex positions have also played a role in tempering currency volatility.

However, risks remain elevated, according to the Crisil report. Persistently high oil prices could widen the current account deficit, strain fiscal balances and fuel inflation. Global monetary divergence, with expected rate hikes by the European Central Bank and Bank of England and a potential rate cut by the US Federal Reserve, could further destabilise capital flows and the rupee. There are also emerging concerns around remittances, which could be disrupted by geopolitical tensions, adding pressure to external balances.

Though India’s macroeconomic fundamentals provide resilience, but they are not immune to prolonged external shocks, the report says. Financial conditions may remain under pressure, and market volatility could persist until geopolitical tensions ease. In that sense, the current episode is less a transient shock and more a stress test; one that will demand policy prudence, fiscal discipline and continued central bank agility to navigate the uncertain months ahead.