New Delhi: The Federation of Indian Chambers of Commerce and Industry (Ficci) has issued a set of “imperatives” for both the industry and the government as the ongoing West Asia conflict threatens to destabilise the country’s economic trajectory. With the Strait of Hormuz — through which nearly 20% of global seaborne oil flows — severely disrupted, the ripple effects are being felt across energy markets, supply chains, and financial systems. For an import-dependent economy like India, the stakes are unusually high.

The scale of disruption is unprecedented in recent years. Shipping traffic through the Strait of Hormuz has reportedly dropped by nearly 95% from pre-conflict levels, while war-risk insurance premiums have surged to 5-10% of vessel value, compared to a peacetime norm of around 0.25%. Damage to critical industrial hubs such as Ras Laffan and Ras Tanura has already curtailed supply, with LNG export capacity at Ras Laffan alone reduced by 17%, and recovery timelines stretching up to five years.

These developments have translated swiftly into severe economic stress for India. Brent crude prices have spiked sharply from $71 per barrel on February 27 to $118 by the end of March. The Indian rupee has weakened to approximately ₹93.5 per dollar, while foreign exchange reserves have declined from $728.5 billion to $698.3 billion within weeks. Growth projections are already under pressure, with estimates revised downward from 7.3% to 7.1%, and warnings of further downside risks.

Inflationary pressures are also building. Even a 10% increase in crude oil prices could add around 20 basis points to headline inflation. Financial markets have reacted nervously, with equity indices falling by about 7.1% in March and volatility doubling. What began as a geopolitical conflict is rapidly morphing into a macroeconomic challenge with implications for fiscal stability, external balances, and industrial output.

The Ficci report makes it clear that this is not a transient shock. Instead, it outlines three potential scenarios — ranging from a short-lived disruption to a prolonged crisis involving closure of the Strait of Hormuz. In the worst-case scenario, global trade routes could be fundamentally altered, forcing rerouting through alternative ports and significantly increasing logistics costs. If this happens, the implications for India’s trade competitiveness and industrial resilience would be profound.

“Given the current crisis may last longer than envisaged, and may flare up again in the future, the Indian industry and government need to work with a bifocal approach of mitigating the current crisis and preparing for a potentially similar event in the future. With targeted fiscal and policy interventions, the impact can be contained and help accelerate beneficial, long-term structural shifts,” the Ficci report said.

Ficci has emphasised the need to diversify sourcing geographically, strengthen domestic supplier ecosystems, and pursue backward integration where feasible.

Managing Costs, Supply Shocks & Structural Vulnerabilities

The impact of the crisis is being felt most acutely across India’s manufacturing and process industries, which are heavily dependent on imports from the Gulf. Imported LNG accounts for 53% of India’s marketed gas, with key sectors such as fertilisers, city gas distribution, power, and refining deeply exposed. LNG prices in Asia have already surged by nearly 80% since the onset of the conflict.

Fertiliser supply chains are particularly vulnerable. Around 15% of global ammonia trade and 21% of urea trade pass through Hormuz, while India imports nearly 75% of its ammonia from the Middle East. Fertiliser prices could rise by 15-20%, potentially increasing India’s subsidy burden by ₹20,000-25,000 crore. Even niche but critical inputs like helium have been affected, with one-third of global supply disrupted due to halted production in Qatar.

The cascading effects are visible across industrial value chains, highlights Ficci. Petrochemical feedstocks such as LPG, naphtha and propylene are in short supply, pushing up input costs for sectors ranging from plastics and textiles to pharmaceuticals and automotive components. Packaging companies have reported price increases exceeding 50% for key materials like HDPE, PP, and PET. Shortages of derivatives such as butadiene, styrene and caprolactam are disrupting tyre production, consumer electronics, and nylon-based industries.

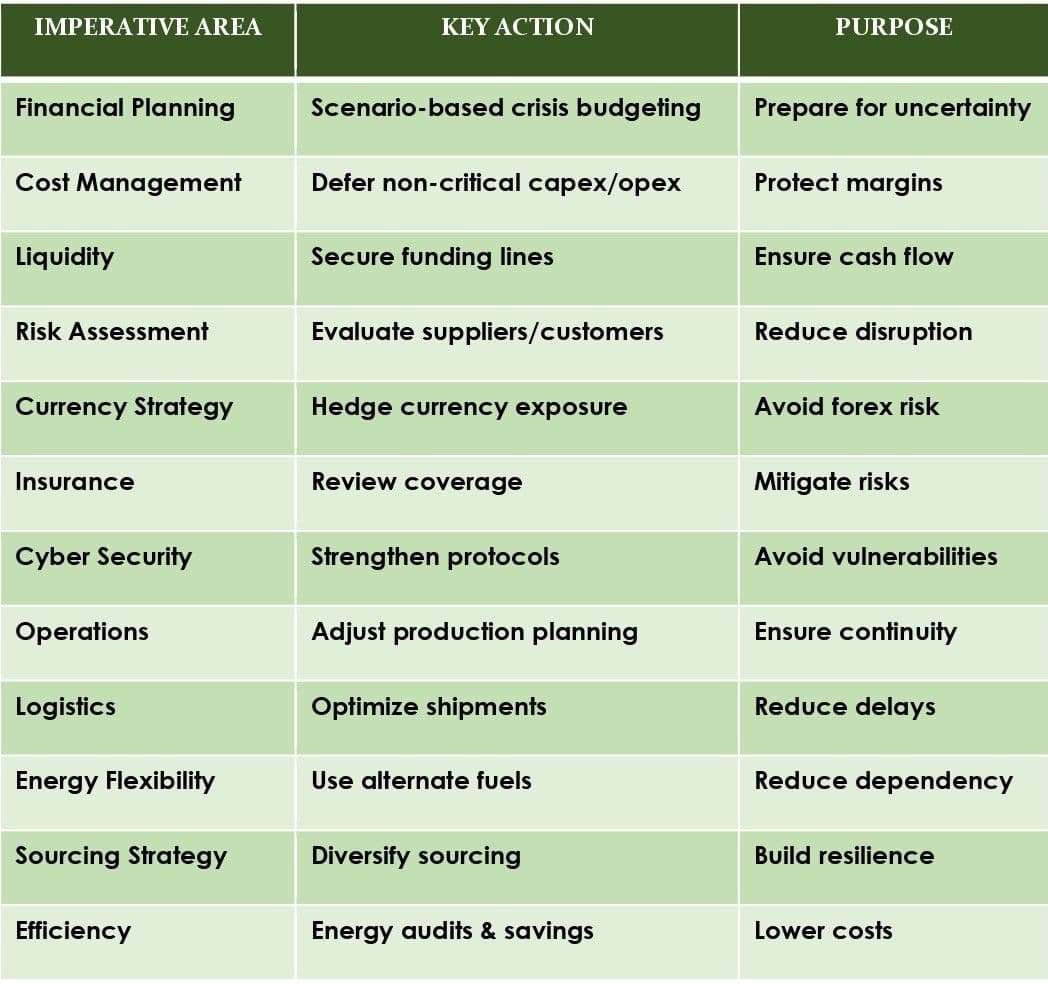

In response, Ficci has outlined a comprehensive set of imperatives for industry, centred on financial resilience and supply chain adaptation. It has urged companies to adopt scenario-based planning, effectively creating a ‘Middle East crisis’ version of their budgets. This includes deferring non-essential capital expenditure, optimising operational costs, and building inventory buffers to mitigate supply disruptions.

Liquidity management is another priority. Ficci advises firms to secure additional funding lines, hedge currency risks, and reassess insurance coverage. Strengthening cybersecurity protocols is also highlighted by the industry body, reflecting the heightened risk environment during periods of geopolitical instability.

Operationally, the focus is on flexibility and efficiency, the report says. Ficci urges companies to recalibrate production schedules based on constrained raw material availability, optimise logistics through shipment consolidation, and collaborate with shipping lines to ensure route stability. The establishment of cross-functional “war rooms” to manage daily disruptions echoes strategies adopted during the Covid-19 pandemic.

Energy diversification is emerging as a critical theme. Firms are exploring multi-fuel capabilities, retrofitting systems to accommodate biofuels or electrification, and increasing reliance on renewable energy sources. Short-term measures such as energy audits and consumption optimisation are being complemented by long-term investments in green hydrogen, biofuels, and advanced energy technologies.

Supply chain resilience is also being reimagined. Ficci has emphasised the need to diversify sourcing geographically, strengthen domestic supplier ecosystems, and pursue backward integration where feasible. Aggregated procurement strategies and partnerships with local vendors are being promoted to reduce dependence on volatile international markets.

Govt’s Role in Stabilisation

While industry action is crucial, Ficci underscores that the scale and complexity of the crisis necessitate strong and coordinated government intervention. The report acknowledges several proactive measures already undertaken, including the formation of sector-specific empowered groups, reductions in fuel excise duties, and the introduction of the ₹497 crore RELIEF (Resilience & Logistics Intervention for Export Facilitation) scheme to support MSME exporters. The restoration of export incentives and enforcement of the Essential Commodities Act have also helped contain immediate pressures.

However, the report argues that more targeted and sustained policy support is required. Ensuring energy security is identified as the top priority. This includes strengthening diplomatic engagement with producer nations, establishing state-level energy security cells, and considering tax reductions on alternative fuels such as LDO and fuel oil to enhance their viability for industrial use.

Logistics facilitation is another critical area. Reducing chartering license fees and fast-tracking port clearances for critical imports could help offset rising freight costs and minimise delays. Financial support mechanisms, particularly for MSMEs, need to be expanded to address working capital constraints. Regulatory flexibility, including guidance on force majeure conditions in public procurement, could provide relief to firms facing unavoidable disruptions.

Looking beyond the immediate crisis, Ficci outlines a strategic roadmap for building long-term resilience. Diversifying energy imports through long-term agreements with countries such as the US, Australia and African nations is essential, it suggests. Expanding the gas grid and accelerating the development of strategic petroleum reserves would further strengthen energy security, it says.

The transition to renewable and clean energy is positioned, by Ficci, as both a necessity and an opportunity. Scaling up green hydrogen, battery storage systems, and biogas production could reduce dependence on fossil fuels while supporting India’s climate goals, the report says. Policy frameworks that replicate the success of solar energy initiatives could accelerate this transition, it adds.

Infrastructure development is another pillar of resilience. Projects such as the India-Middle East-Europe Economic Corridor and the International North-South Transport Corridor could provide alternative trade routes, reducing reliance on vulnerable maritime chokepoints. Strengthening multi-modal logistics and enhancing MSME capabilities through initiatives like PM-MITRA parks would further bolster industrial competitiveness.

The report also highlights the importance of agricultural resilience, particularly in managing fertiliser availability. Promoting bio-fertilisers, improving efficiency through precision agriculture, and addressing farmer concerns about alternatives to chemical fertilisers are critical steps in ensuring food security amid global supply disruptions, the Ficci report says.

The imperatives suggested by Ficci present a sobering yet constructive roadmap for navigating one of the most complex geopolitical-economic crises faced by India in recent times. While the West Asia conflict poses immediate risks to India’s growth and stability, it also offers an opportunity to accelerate structural reforms, enhance resilience, and redefine the country’s economic architecture, the report says.