New Delhi: The prospect of oil surging to $150 a barrel is back on the table as geopolitical tensions involving Iran refuse to fade. For global markets, the bigger risk is not merely another Middle East conflict but the possibility of a prolonged disruption to energy flows through the Strait of Hormuz, the world’s most critical oil transit chokepoint.

The immediate market reaction to any escalation would almost certainly be a sharp spike in crude prices. Traders have repeatedly demonstrated that geopolitical premiums can overwhelm underlying supply-demand fundamentals, especially when nearly a fifth of global oil trade is potentially at risk.

The latest Oil Market Balances Report by Rystad Energy offers an intriguing counterpoint to the prevailing market anxiety. While the consultancy acknowledges the enormous risks surrounding the Middle East conflict, it argues that the global oil market is simultaneously heading towards a structural oversupply, creating a complex and often contradictory outlook for investors and policymakers.

“All eyes are on the Strait of Hormuz,” notes the report, highlighting how a single maritime corridor has become the focal point of global energy security. Yet the same study suggests that longer-term market dynamics could eventually cap sustained price rallies.

That contradiction lies at the heart of today’s oil story. A fresh military escalation involving Iran could easily push prices towards $150 in the short term, but whether such levels can be maintained is a far more complicated question.

Supply Meets Reality

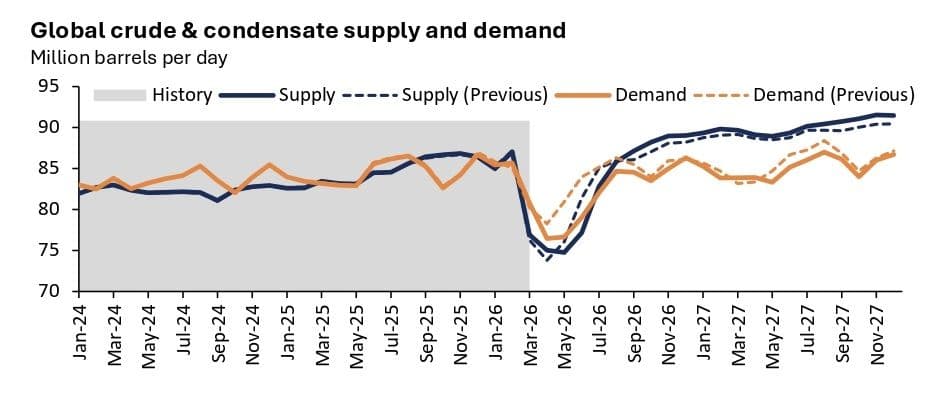

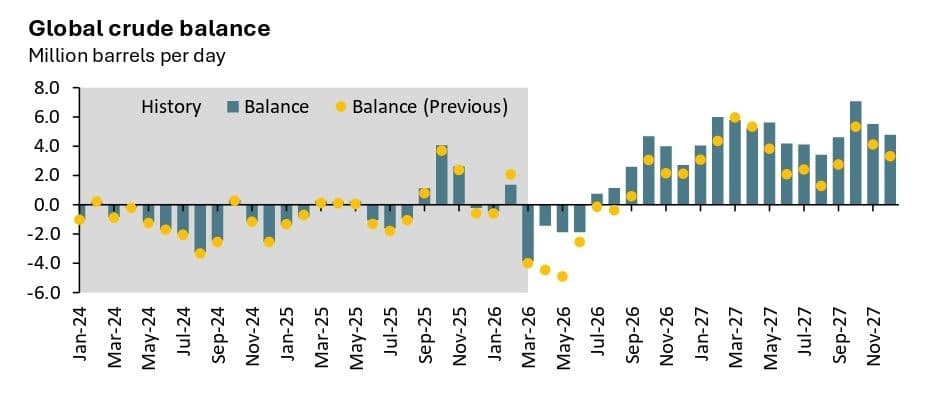

According to Rystad Energy, crude balance (or crude oil balance) refers to the fundamental equation measuring global crude oil supply versus crude oil demand. It is the difference between total crude and condensate production (supply) and the amount of crude consumed by refineries and direct crude burning (demand).

Its analysis suggests the oil market has become more balanced than previously feared, largely because demand expectations have weakened while supply adjustments have been relatively modest.

The consultancy now expects the global market to record an average oversupply of about 600,000 barrels a day in 2026, a dramatic reversal from its earlier expectations of a supply deficit. Elevated energy prices themselves are beginning to curb consumption, particularly across Asia, while logistical disruptions have altered refinery operations across several regions.

The report observes that “demand takes the front seat of the changes this month”, reflecting how higher prices and trade bottlenecks are reshaping consumption patterns. For energy economists, this is a reminder that expensive oil eventually destroys demand, even if geopolitical risks initially tighten supplies.

Iran remains central to the equation. US pressure on Iranian oil exports and regional military uncertainty have complicated production and shipping, while attacks on critical infrastructure have reinforced concerns about supply vulnerabilities. The report points out that “Iran’s attack on Saudi Arabia’s East-West pipeline offered a stark reminder of a vulnerable system.”

The conflict has also forced a remarkable reordering of global trade flows. Brazilian and Venezuelan crude is finding new buyers in Asia, while the US has increased exports to help offset Middle Eastern disruptions. Strategic petroleum reserve releases have softened some of the immediate pressure, but they are hardly a permanent solution.

There is another reason markets remain nervous. Even if the Strait of Hormuz were to reopen quickly after a ceasefire, restoring normal trade would not happen overnight. Production facilities require time to ramp up, shipping fleets need repositioning and commercial inventories must be rebuilt.

A sustained closure or renewed military confrontation could therefore create a temporary but severe supply squeeze. In such a scenario, analysts warn that prices could briefly overshoot fundamental valuations and move towards the psychologically significant $150 mark.

Price Versus Politics

Perhaps the most striking conclusion from the Rystad assessment is that today’s oil market is being driven as much by politics as by economics.

The consultancy has actually lowered its Brent price forecasts for the near term, partly because diplomatic efforts between Washington and Tehran could reduce tensions. However, those projections depend heavily on geopolitical assumptions that remain highly uncertain.

The report says, “prices remain elevated due to the extended timeline of disruption”, underlining that markets are pricing in prolonged uncertainty rather than a quick resolution.

There is also a broader structural story unfolding. High fuel prices and concerns over supply security are accelerating the energy transition. Electric vehicle sales have strengthened in several markets, particularly in Europe, while governments are reassessing long-term dependence on imported fossil fuels.

Ironically, another oil shock could strengthen the very forces that eventually weaken crude demand. Consumers faced with expensive petrol and diesel are more likely to switch technologies, while policymakers could accelerate investments in energy diversification.

That does not mean the immediate economic pain would be any less severe. A move towards $150 oil would intensify inflationary pressures, increase transport and manufacturing costs, complicate central bank policy and widen trade deficits for major importing economies, including India.

For India, the stakes are particularly high. The government has diversified its crude sourcing over recent years, but it remains heavily dependent on imported energy. Any sustained disruption in Middle Eastern supplies would increase procurement costs and place additional pressure on government finances and household budgets.

The larger lesson is that oil markets remain vulnerable to geopolitical shocks despite years of investment in energy security. The world may eventually face an oversupplied market, as Rystad Energy expects, but wars rarely wait for economic logic.

A fresh confrontation with Iran could push crude towards $150 a barrel, at least temporarily. Whether those prices endure will depend less on the size of global oil reserves than on the willingness of political leaders to prevent another Middle East crisis from becoming a full-blown energy emergency.