New Delhi: India’s economic resilience is being stress-tested by a volatile global environment.

The Finance Ministry’s Monthly Economic Review for April comes with a warning that external shocks are intensifying, even as domestic fundamentals remain robust. The report’s central takeaway: India is relatively insulated, but not immune. And the durability of that insulation will depend on how policy responds to simultaneous pressures from energy markets, geopolitics and climate risks.

The report underscores that while domestic demand, public investment, and a stable financial system provide a cushion, the persistence of supply disruptions, particularly in energy and fertilisers, could tilt the macroeconomic balance unfavourably. Inflation risks are rising, growth risks are increasing, and fiscal pressures are building.

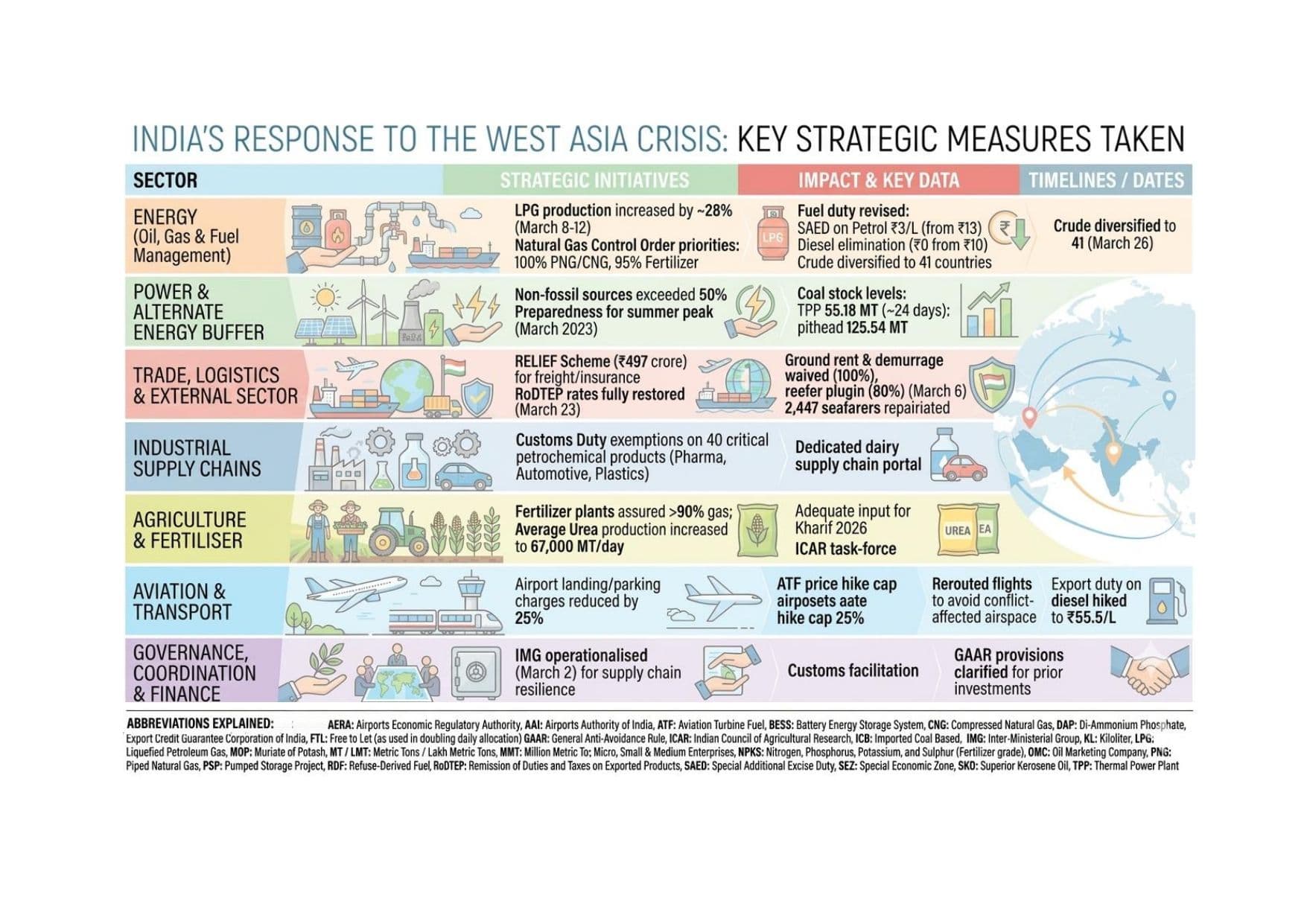

The global backdrop has turned decisively adverse. What began as a year of stabilising inflation and improving growth prospects has been disrupted by the West Asia conflict, which has triggered supply shocks, elevated commodity prices, and revived uncertainty in global trade and financial flows. India, like other energy-importing economies, is exposed to these shifts, though it remains better positioned than most emerging markets.

On the uncertainty ahead, the report says: “It has been 60 days since the conflict in West Asia began on February 28. We do not appear to be closer to a resolution. The positions of the warring parties remain wide apart, as the negotiations are marked or marred by a lack of trust regarding the underlying motive for ceasing hostilities.”

This prolonged uncertainty is already feeding into higher costs, tighter supply chains, and cautious business sentiment. Yet, the report insists that India’s policy framework and structural strengths offer a platform to navigate these challenges, provided reforms are accelerated rather than deferred.

Supply Shocks, Inflation Risks

At the heart of the economic challenge lies the surge in global energy prices and its cascading impact across sectors. India’s crude basket hovering above $110 per barrel has intensified concerns over inflation, trade deficits and fiscal stability.

“Some countries have begun to allow prices to be passed on to end-users – households and businesses. Some are yet to do so. But it is inevitable. During a period of supply disruption, demand has to moderate; failing that, countries will have to pay a much higher price for energy supplies,” says the report on the inevitability of price transmission.

This observation captures a fundamental policy dilemma. Shielding consumers from price shocks may contain inflation in the short term, but it risks widening fiscal deficits and distorting market signals. Conversely, passing on costs could dampen demand and slow growth.

Compounding the energy shock is the likelihood of a weaker monsoon due to the El Niño Southern Oscillation (ENSO). The report highlights the dual risk of supply-side inflation and reduced agricultural output, warning that macroeconomic risks are becoming increasingly asymmetric. “On top of this, the El Niño Southern Oscillation (ENSO) is expected to keep India’s Southwest monsoon below normal. Most rainfall districts are expected to receive below-normal rainfall this season. Therefore, risks are tilted to the upside for inflation, fiscal and external deficits and to the downside for economic growth.”

The inflation outlook, therefore, is no longer benign. While consumer inflation remains moderate for now, wholesale price pressures are rising sharply, indicating that cost increases could soon pass through to consumers. This creates a complex policy trade-off between supporting growth and maintaining macroeconomic stability.

The report also questions global assumptions about oil prices, noting that many forecasts may be overly optimistic. “In the second week of April, the IMF released its World Economic Outlook. With an assumption of $82 per barrel for the year, the IMF’s overall macroeconomic forecasts appear more sanguine than they would otherwise be. In other words, the risks to the IMF’s growth forecasts are heavily tilted to the downside, while inflation risks are tilted to the upside.”

This divergence between assumed and actual price trajectories suggests that global growth projections could be revised downward if the conflict persists and energy markets remain tight.

India’s crude basket averaged about $113 per barrel in March and nearly $115 per barrel in April (till April 24), underscoring the intensity of imported cost pressures. At the same time, wholesale price inflation jumped sharply from 2.13% in February to 3.88% in March, signalling rapid transmission of input costs. Consumer inflation, however, remained relatively moderate at 3.4% in March, reflecting temporary policy shielding of households.

Domestic Strengths

Despite these external shocks, the report maintains that India’s domestic economy retains significant resilience. High-frequency indicators show that while supply-side pressures are emerging, demand remains relatively stable. Consumption, infrastructure activity and credit growth continue to support economic momentum.

The resilience is rooted in deliberate policy choices made over recent years, particularly in strengthening financial stability, maintaining fiscal discipline and sustaining public investment. The banking system remains well-capitalised, liquidity conditions are adequate, and credit growth is broad-based.

According to the MER: bank credit grew by 17.1% year-on-year as of March 31, 2026, while total exports (goods and services) rose 4.2% to a record $860.1 billion in FY26, with services exports alone crossing $418.3 billion for the first time.

However, the report cautions against complacency. The current environment exposes structural vulnerabilities, particularly India’s dependence on imported energy and critical inputs. Supply chain disruptions in fertilisers, chemicals and industrial inputs are already affecting production and sentiment.

It also highlights a broader lesson for policymakers. “One enduring message for policymakers from the conflict is the need to build buffers of key commodities. That goes beyond energy. That has moved up the ladder of policy priorities and will remain there for the next decade or two as geopolitical conflicts intensify,” it says.

This emphasis on resilience marks a shift in economic thinking — from efficiency-driven globalisation to security-oriented policy frameworks. Strategic reserves, diversified supply chains and domestic manufacturing capacity are no longer optional; they are essential.

At the same time, the report warns against excessive focus on short-term growth at the expense of macroeconomic stability. “In this context, it will be a reasonable temptation for many countries to shore up near-term growth and preserve employment. However, macroeconomic stability is equally important, as anxious attempts to restore near-term growth may cause significant harm to medium to long-term growth prospects by destabilising external balances, the inflation outlook and the currency,” the MER says.

This balancing act — between growth and stability — will define India’s policy response in the months ahead.

Further, high-frequency indicators reflect mixed signals: e-way bill generation touched a record 140.6 million in March, while PMI manufacturing moderated to 53.9 and services to 57.5, indicating continued expansion but easing momentum. Fertiliser production contracted sharply by 24.6% in March due to input shortages, highlighting sector-specific stress.

Crisis as Catalyst

Perhaps the most striking aspect of the report is its call to treat this ongoing crisis as an opportunity for structural reform. It outlines a five-point agenda that includes energy security, deregulation, agricultural reform, workforce skilling and tax policy certainty. “It is axiomatic in policy circles that crises should not be allowed to go to waste. This crisis is no exception,” notes the report.

Energy security emerges as the top priority. The report stresses that India must reduce vulnerability to external shocks without replacing one dependency with another. Investments in public transport, renewable energy and strategic reserves are seen as critical to achieving this goal.

Equally important is the push for regulatory simplification and trade facilitation. Lowering the cost of imports and exports, improving logistics and removing policy distortions in agriculture could enhance productivity and competitiveness.

The report also underscores the importance of preparing the workforce for structural changes, particularly the impact of artificial intelligence. Promoting “AI-insulated” skills could boost both domestic employment and export potential.

Tax policy stability is another key pillar. In a world where supply chains and investment flows are increasingly influenced by geopolitics, predictable and transparent tax regimes are essential to attract capital and sustain growth.

The external sector data adds urgency to these reforms. India’s merchandise trade deficit widened to $333.2 billion in FY26 from $283.5 billion in FY25, while the overall trade deficit rose to $119.3 billion. Global growth is projected to slow to 3.1% in 2026, with adverse scenarios suggesting a slowdown to 2.0-2.5% and inflation rising up to 6%, highlighting the challenging global backdrop.

The report stresses that if the recommended policy actions are implemented, India could emerge stronger from the current crisis, with a more resilient and diversified economic base. However, resilience alone is not enough. The coming months will test not just the strength of India’s economy, but the agility and foresight of its policy response.