New Delhi: A dual shock from the escalating Iran-Israel war and looming refinery closures/rationalization is reshaping global energy markets, with conflict-triggered high crude prices colliding against forecasts that 21% of global refining capacity could be at risk of shutting down by 2035, predicts Wood Mackenzie, which specializes in research and analytics across the energy and natural resources landscape.

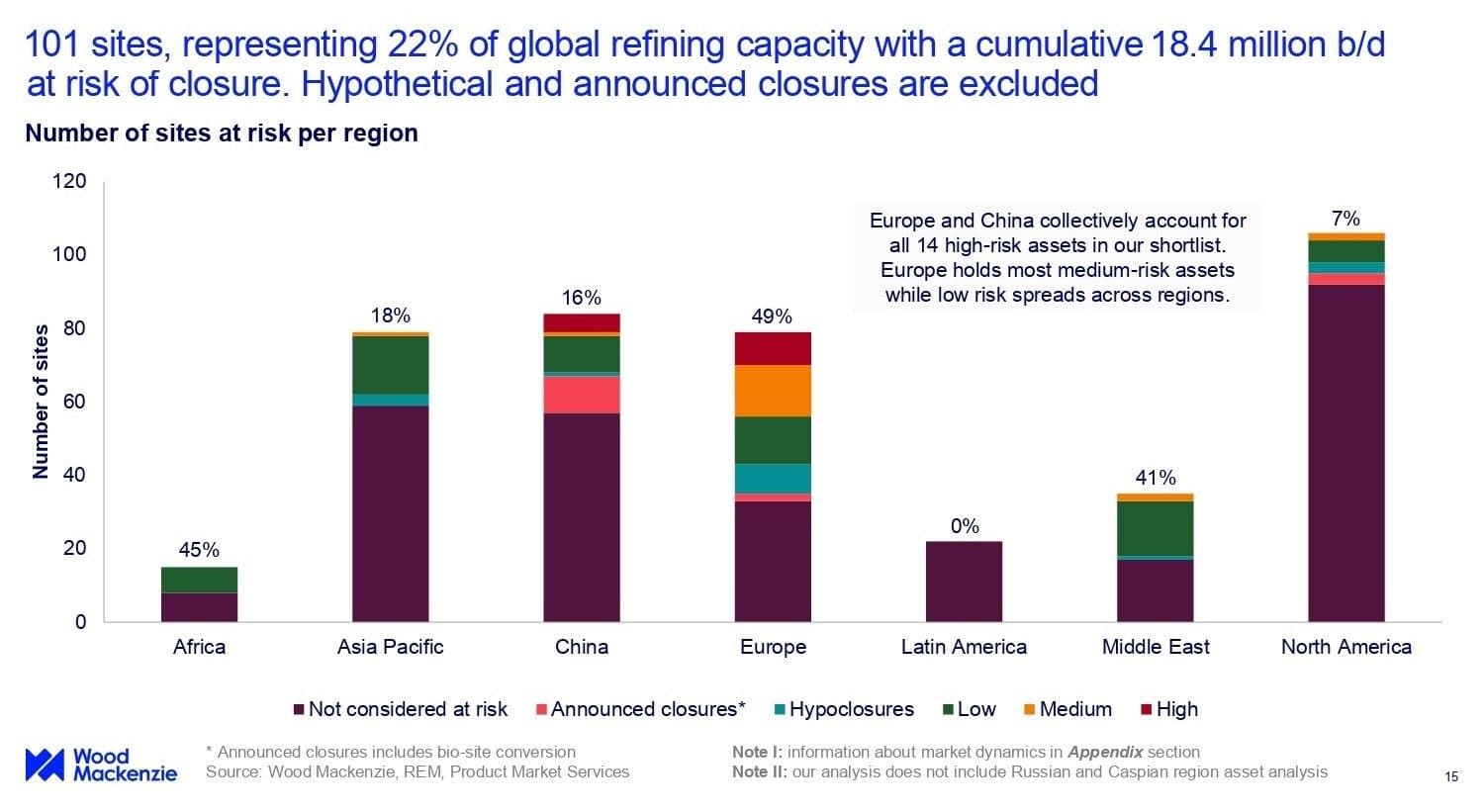

A new analysis, conducted by WoodMac, highlights how structural pressures within the refining sector are intensifying just as geopolitical instability drives oil price volatility. Based on the 2035 integrated net cash margin forecasts, 101 out of 420 screened refining sites have been identified as “at risk of closure”, representing 18.4 million b/d of capacity, equivalent to 21% of global refining capacity in 2023.

The geographic concentration of this risk is striking, with Europe and China alone accounting for all high-risk sites and Europe holding 62% of the threatened capacity, even as 70% of the shortlisted assets remain categorised as low-risk.

Operational complexity and decarbonisation exposure are emerging as defining factors. Complex and deep-conversion refineries, particularly those operating in regions with carbon pricing regimes, are disproportionately vulnerable. By 2035, carbon emission costs without free allowances are expected to significantly erode margins, especially in the EU, UK and Canada where carbon prices are forecast to be roughly three times higher than in other regions. Survival will depend heavily on investment in decarbonisation projects, which may be difficult to justify for weaker assets already facing margin compression.

The lack of petrochemical integration further compounds the risk profile. Around 60% of the shortlisted sites are standalone refineries, limiting their ability to capture additional value streams. Only 29 of the 101 at-risk sites have petrochemical integration with olefins production, and even among these, 13 face additional margin pressure due to vulnerabilities in steam cracker economics. While petrochemical margins are expected to recover toward the end of the decade, the benefits will be unevenly distributed.

Ownership structures also play a critical role in determining resilience. National oil company refiners are viewed as less exposed to closure risk due to likely government support, even in scenarios of negative net cash margins. In contrast, international oil companies continue to optimise portfolios by divesting weaker assets, often transferring them to independents or joint ventures that may prioritise short-term profitability with minimal capital investment before eventual shutdown decisions.

War-triggered Volatility

These structural industry challenges are unfolding against the backdrop of a volatile oil market shaped by the Iran-Israel war. A temporary easing of tensions in week four, marked by reports of US-Iran talks, pushed Brent prices below $100/barrel, but uncertainty remains over whether this signals a turning point or merely a pause before further disruption to Gulf exports.

The stakes are high. “The importance of oil and the sensitivity of the global economy to price can’t be overstated. Wood Mackenzie analysis suggests that a scenario of Brent averaging $125/bbl through 2026 will lead to a global recession, a view broadly echoed this week by Blackrock CEO Larry Fink. No economy is immune to the fallout of sustained, high crude prices, but some are impacted more than others. The major oil-importing countries of Asia are among those feeling the pain most acutely,” says Simon Flowers, Chairman & Chief Analyst, WoodMac.

Asia sits at the epicentre of the economic fallout due to its deep reliance on West Asia crude. Prior to the conflict, about 80% of oil moving through the Strait of Hormuz was destined for Asian refineries. Countries such as Japan and South Korea depended on the Gulf for more than 90% and 70% of their imports respectively, while China and India, despite diversification efforts toward Russia and the US, still source roughly half of their crude from the region. This structural dependence leaves both advanced and developing Asian economies acutely exposed to supply disruptions and price spikes.

The economic vulnerability is particularly severe for emerging markets across South and Southeast Asia, where growth models rely heavily on manufacturing and exports and where foreign currency reserves are often limited. In 2026, the so-called “war premium” on oil is translating into tangible pressure on national balance sheets, amplifying fiscal and external imbalances.

Traffic in Bangkok. Thailand and Vietnam are drawing from dedicated funds to offset losses suffered by refiners and fuel suppliers, although these reserves are already under strain. (Photo by Photo by Robert Eklund on Unsplash)

Asia’s Policy Responses

Governments across the region have responded with aggressive intervention to shield consumers and industries from rising fuel costs. Measures include price caps, subsidies and compensation schemes for refiners and fuel suppliers. Indonesia plans to reimburse losses incurred by its national oil company, while Japan and Malaysia are deploying similar mechanisms. Thailand and Vietnam are drawing from dedicated funds to offset losses, although these reserves are already under strain.

China has implemented a $130/bbl cap on refined product prices and has introduced additional subsidies despite prices remaining below that threshold. India has frozen retail prices, with state-owned oil marketing companies initially absorbing losses until the government steps in through tax cuts, effectively trading fiscal revenue for price stability.

However, the sustainability of these interventions is increasingly in question. If oil remains at $100/bbl for four months, total fuel subsidies across Asia are projected to exceed $80 billion. In a prolonged high-price scenario, the fiscal burden intensifies, affecting deficits, balance of payments and potentially sovereign credit ratings. Thailand’s subsidy fund is already in deficit, while Vietnam’s is expected to be fully depleted by early April under current conditions.

Among major economies, India faces the most significant fiscal strain, with subsidy costs estimated at 0.7% of GDP and 7.2% of government revenue for fiscal year 2025-26 under a $100/bbl scenario. Indonesia risks breaching its legal fiscal deficit ceiling of 3% if elevated subsidy spending persists. Even countries with stronger fiscal positions are likely to face prolonged budgetary pressures, exacerbated by currency depreciation that increases the cost of dollar-denominated oil imports.

The trajectory of oil prices remains the critical variable. A sustained escalation of the conflict could push Brent toward $125/bbl, triggering global recessionary conditions and compounding the structural challenges already facing the refining sector. Conversely, a durable ceasefire and the normalisation of tanker flows through the Strait of Hormuz would ease pressure on both markets and governments.

Thus, the trajectory of oil prices remains the critical variable, even as structural risks within the refining sector continue to mount. A sustained escalation of the conflict could push Brent toward $125/bbl, triggering global recessionary conditions while amplifying margin pressures on already vulnerable refineries, accelerating potential shutdowns. Conversely, a durable ceasefire and the normalisation of tanker flows through the Strait of Hormuz would ease price volatility but do little to offset the longer-term rationalisation pressures facing the industry.

In this environment, the convergence of geopolitical instability, war-driven price shocks and structural capacity closures underscores a period of worrisome uncertainty for global energy markets, with both short-term volatility and long-term transformation reinforcing each other in shaping the industry’s future.

(Cover photo by mos design on Unsplash)