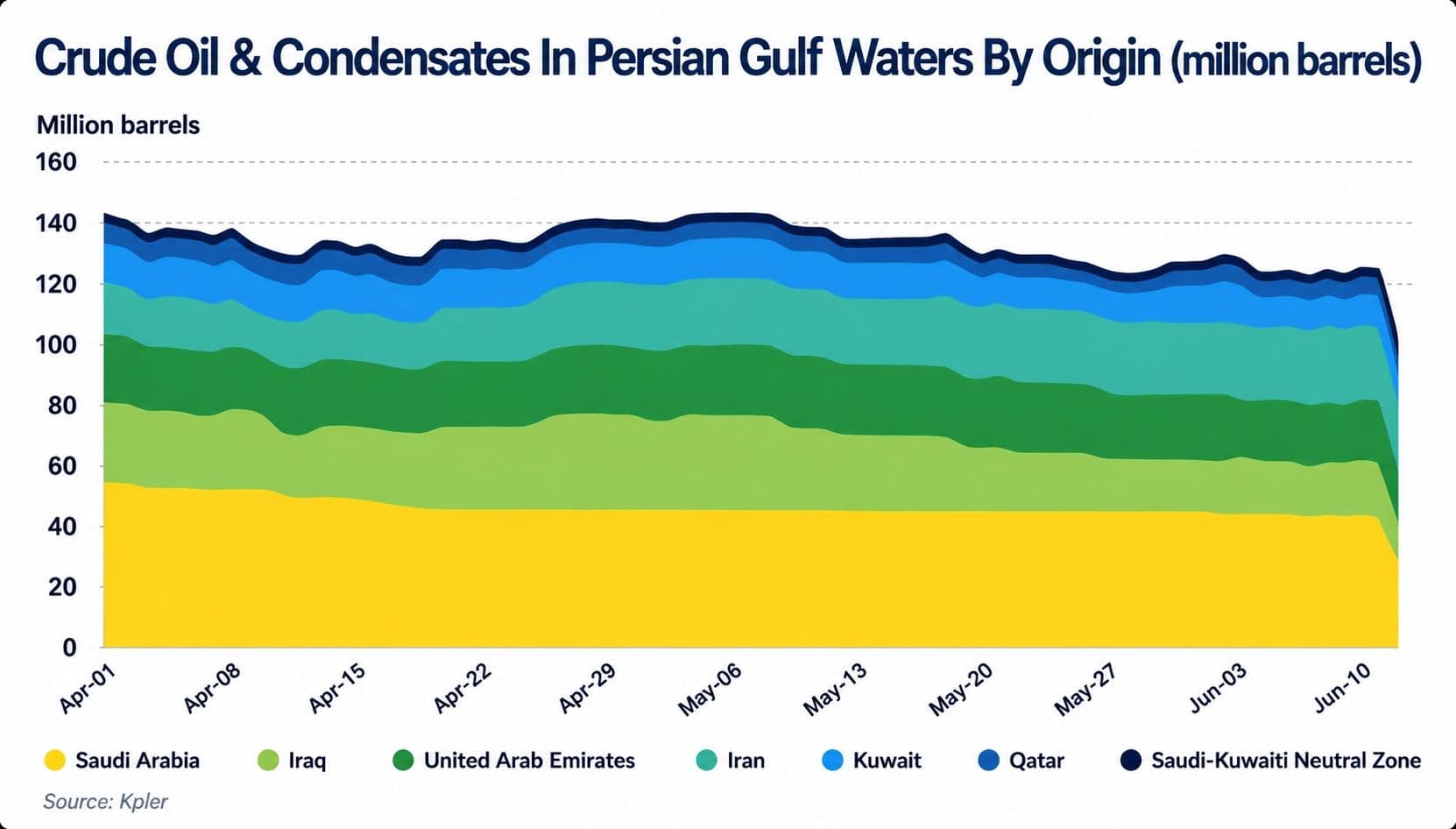

New Delhi: The global oil market is rapidly shifting from fears of disruption to concerns over oversupply as the reopening of the Strait of Hormuz threatens to unleash a wave of crude cargoes that have been stranded for weeks across the Persian Gulf.

According to maritime analytics firm Kpler, the return of shipping traffic through one of the world’s most important energy chokepoints could release approximately 93 million barrels of non-Iranian crude that remain trapped inside the Gulf. At the same time, a potential easing of restrictions on Iranian exports could bring an additional 72 million barrels into international markets, creating a powerful “supply shock” just as demand growth shows signs of slowing.

The development marks a dramatic reversal from the wartime supply concerns that dominated energy markets earlier this month. The report notes that crude benchmarks linked to Middle Eastern exports have already started reflecting the changing fundamentals, with Dubai spreads and regional crude premiums collapsing as traders prepare for a flood of barrels.

Kpler said the reopening of the waterway could trigger a rapid clearing of the export backlog. “The reopening of the Hormuz Strait could unleash some 93 mb of stranded non-Iranian barrels from the Persian Gulf, while producers are expected to continue supplying cargoes through less visible channels. On top of this, the lifting of the US blockade on Iranian crude could release a further 72 mb of Iranian cargoes currently held west of Chabahar.”

The report highlights how quickly market sentiment has turned from scarcity to abundance, particularly as major Gulf producers continue finding alternative routes to move oil.

Producers Push Volumes

Middle Eastern exporters have not waited for a full restoration of normal shipping conditions.

Kpler data shows crude loaded through ship-to-ship transfer operations in the Gulf of Oman surged to around 2 million barrels per day in June, up sharply from 772,000 barrels per day in May and just 303,000 barrels per day in April. Much of the increase is believed to have originated from the UAE, with additional volumes from Kuwait and Iraq.

The most visible sign of producer confidence has come from Abu Dhabi. ADNOC has already launched its third crude sales tender this month, offering Upper Zakum, Das and Umm Lulu grades under multiple delivery arrangements, including direct loading, storage-based lifting and ship-to-ship transfers, says the report.

The state producer is estimated to have already sold at least 40 million barrels of June-to-August loading crude through earlier tenders. Buyers from China, India, Japan and South Korea have reportedly accounted for most of the purchases.

Kpler estimates that once navigation conditions stabilise, laden vessels already waiting inside the Gulf could depart first, enabling a relatively swift reduction in congestion. “Provided there are no restrictions from the Iranian side, the backlog could be cleared within roughly 10-15 days. Of these cargoes, 42.5 mb are Saudi, 18.4 mb are UAE-origin, and 15 mb are Iraqi.”

Assuming ADNOC awards another 20 million barrels through its latest sales programme, Kpler estimates that at least 153 million barrels of non-Iranian Persian Gulf crude could enter the market between June and August alone.

The return of these volumes comes at a time when producers are increasingly expected to insist that long-term customers lift their contracted supplies. Such requirements could reduce refiners’ appetite for discretionary spot purchases and place additional downward pressure on prompt crude prices.

The market has already begun responding. The Dubai M1-M3 spread narrowed sharply to about $1.6 per barrel from roughly $6 per barrel a week earlier. Premiums for flagship Middle Eastern grades such as Murban and Upper Zakum have also fallen to multi-year lows, signalling weaker competition among buyers.

Demand Lags Supply

The biggest uncertainty now lies on the demand side.

While refinery activity across Asia has recovered substantially since the conflict period, Kpler believes the rebound may not be strong enough to absorb the incoming supply wave. Refinery utilisation in Asia excluding China has already recovered to around 90% of pre-war levels and is projected to rise only modestly over the coming months.

Although refiners continue to benefit from healthy product margins during the summer driving season, analysts see limited room for further processing increases. Inventory rebuilding is also expected to be gradual despite significant stock draws earlier this year.

Kpler estimates that Asia-Pacific inventories outside China declined by 78 million barrels between March and May. However, historical replenishment patterns suggest replacement buying could emerge slowly, providing little immediate relief to oversupplied crude markets.

China remains the decisive variable. The country continues to process significantly less crude than before the conflict and retains sizeable onshore inventories. Without stronger policy support, analysts see little reason for Chinese refiners to aggressively increase purchases. “Unless Beijing relaxes restrictions on product exports and/or proceeds with another round of SPR refilling, which some market participants said had been planned prior to the war, Chinese refiners are unlikely to have strong incentives to buy crude in large volumes,” according to the Kpler report.

The absence of a major Chinese buying programme could leave global oil markets vulnerable to a short-term imbalance. Additional pressure may emerge if the United States proceeds with planned Strategic Petroleum Reserve releases, potentially adding more Atlantic Basin crude to a market already preparing for the return of Persian Gulf supplies.

For traders, the immediate challenge, according to the Kpler report, is no longer whether enough oil will reach the market, but whether demand can absorb it quickly enough. With more than 150 million barrels expected to re-enter global trade flows over the next two months, the risk of a temporary supply glut is becoming the dominant theme in oil markets, increasing the likelihood of further weakness in Dubai-linked crude benchmarks and raising the prospect of a brief return to contango.