New Delhi: India’s manufacturing sector is showing signs of strain beneath a headline expansion, as slowing demand momentum tempers optimism around output and new orders. The latest data indicates that while activity remains in growth territory, the pace of expansion is losing steam amid persistent global and domestic headwinds, raising concerns about the durability of the recovery going into the new fiscal year.

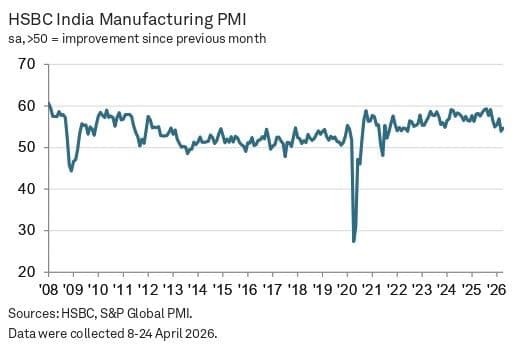

The HSBC India Manufacturing Purchasing Managers’ Index report released today (May 4, 2026) highlights this divergence, with the headline PMI rising to 54.7 in April from 53.9 in March. The report notes that this still marks one of the weakest improvements in operating conditions in nearly four years, underscoring the fragile nature of the recovery and suggesting that the sector is expanding more out of resilience than strong demand traction.

According to the report, gains in new orders and output remain subdued despite sequential improvement. Competitive pressures, cautious client behaviour, and geopolitical uncertainties are weighing on demand, limiting the strength of the rebound. Advertising and marketing efforts have supported sales to an extent, but have not been sufficient to offset broader demand-side hesitations.

“April data showed mild recoveries in growth of new business intakes and production among Indian manufacturers, but rates of increase were still the second-weakest since 2022. Exports was a bright area, with firms welcoming the fastest upturn since last September,” notes the report.

Export demand has emerged as a rare bright spot, supported by stronger orders from key international markets. However, domestic demand continues to show signs of fatigue, with firms reporting hesitation among clients to approve pending contracts, reflecting a cautious investment climate and tighter budget cycles across industries.

Even as companies increased hiring at the fastest pace in 10 months, the mismatch between employment growth and output momentum points to an uneven and uncertain recovery trajectory. The expansion in workforce appears to be driven more by long-term capacity planning and optimism rather than immediate demand pressures. At the same time, growth in purchasing activity has slowed to one of its weakest levels in over two years, signalling caution in inventory accumulation and production planning.

Inflation Pressures, Policy Concerns

The report flags a sharper and more immediate risk in the form of surging inflationary pressures, largely driven by geopolitical disruptions in the Middle East. Input costs have risen steeply, forcing manufacturers to pass on higher prices to customers and potentially fuelling broader inflation, complicating the macroeconomic outlook.

According to the report, “Companies continued to indicate that the war in the Middle East exerted upward pressure on inflation. Input costs and output charges rose at the quickest rates in 44 and six months respectively.”

The increase in cost burdens spans multiple categories, signalling systemic inflation rather than isolated price shocks. Manufacturers are facing higher prices for metals, chemicals, fuel and other key inputs, which are feeding into output charges at an accelerating pace. This cost escalation is particularly significant as it comes at a time when demand remains uneven, squeezing margins and forcing difficult pricing decisions.

“Panellists often attributed hikes to the Middle East war. The overall rate of inflation climbed to its highest since August 2022. Subsequently, goods producers lifted their fees to the greatest extent in six months,” the report highlights.

Inventory strategies reflect this uncertain environment. Firms are maintaining lean stock levels amid subdued sales, while only marginal accumulation of finished goods indicates limited confidence in near-term demand. Input inventories are rising at their slowest pace in nearly five years, reinforcing the cautious stance adopted by manufacturers in response to demand volatility.

Improvements in supplier delivery times, however, offer a partial counterbalance. The report suggests that better coordination with suppliers has led to a historically strong reduction in lead times, easing some operational bottlenecks that had previously constrained production schedules.

Although overall business sentiment remains relatively strong, it has softened from recent highs. According to the report, confidence is anchored in expectations of improved marketing outcomes and approvals of pending projects rather than a decisive demand revival. The moderation in sentiment suggests that firms are increasingly aware of the risks posed by inflation and geopolitical instability.

The interplay between cost pressures and cautious demand could shape policy responses in the months ahead, particularly as authorities weigh inflation control against the need to sustain industrial growth.

(Cover photo by Fastenex P on Unsplash)