New Delhi: India’s hotel industry is poised to extend its multi-year growth cycle into FY27, with strong leisure travel, weddings and social events expected to offset emerging risks from geopolitical tensions and softer corporate demand. India Ratings and Research (Ind-Ra) expects revenue per available room (RevPAR) to remain resilient across its rated portfolio, even as the pace of growth moderates after a sustained recovery.

The agency expects occupancy for its peer set of 13 listed hotel companies to remain close to FY26 levels of nearly 74%, supported by a structural shift in consumer spending towards experiences rather than goods. Demand and supply are both projected to expand by 10%-15% year-on-year, helping maintain healthy operating cash flows despite signs that room pricing is approaching a cyclical peak.

“Our baseline estimates on the hotel sector demand and supply growth range from 10%-15% y-o-y in FY27, leading to sustained robust operating cash flows even as RevPAR growth normalises. Key industry players have focused on brownfield investments and leasing models to swiftly add capacity and capitalise on strong spending trends,” says Mahaveer Shankarlal, Director (Corporates), Ind-Ra.

Corporate Travel Faces Pressure

While leisure demand remains robust, the Ind-Ra report highlights growing uncertainties for the business travel segment. Rising oil prices linked to geopolitical tensions in the Middle East could increase operating costs for companies and curb corporate travel budgets, creating a divergence between leisure and business demand.

The moderation in demand growth is also expected to coincide with a stabilisation in room tariffs. Average room rate (ARR) growth, which rose 5%-8% in FY26 and between 2% and 13% across the broader peer set, is expected to approach its cyclical high. As a result, RevPAR growth is likely to normalise in FY27, although absolute levels are expected to remain healthy by historical standards.

“We further expect major hotel operators to continue outperforming the industry in FY27, on back of continued industry consolidation. Within segments, leisure and luxury are likely to remain more resilient than the premium and business. Despite strong supply additions, the balance sheet leverage is likely to remain low, with the capacity to absorb the risk of a near-term oil shock,” Shankarlal adds.

Consolidation Gathers Pace

India’s leading hotel operators are accelerating capacity additions to capture strong travel demand, with expansion strategies increasingly centred on brownfield projects, asset upgrades and leasing models that require relatively lower capital commitments. International growth in key gateway cities is also emerging as an important avenue for larger players.

At the same time, rising merger and acquisition activity and greater institutional participation are reshaping the competitive landscape. The report expects larger hotel chains to outperform the broader industry as consolidation strengthens market positioning and operational efficiencies.

According to the report, “The ongoing upcycle has accelerated capacity additions across rated entities through brownfield expansions, asset upgrades, leasing models, and international expansion in gateway cities. Additionally, rising M&A activity and increasing institutional ownership are driving industry consolidation, with larger players likely to outperform the broader market.”

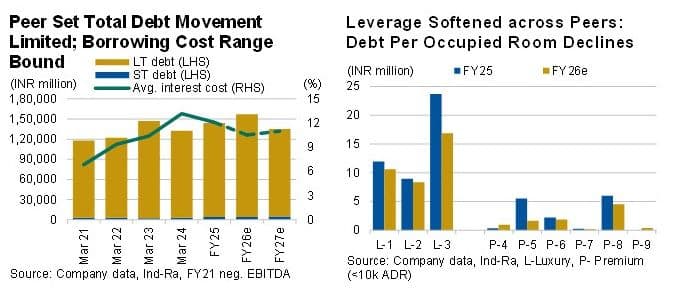

Strong Balance Sheets

Despite aggressive expansion plans, Ind-Ra expects the financial profile of major hotel operators to remain robust. EBITDA margins across the rated portfolio are projected to remain stable to marginally lower at 39%-40% in FY27, supported by a favourable mix of revenues from banquets, food and beverage operations, and management contracts.

The report expects only a marginal increase in leverage as companies fund expansion and acquisitions, while maintaining adequate financial flexibility to withstand external shocks. Healthy cash flows and disciplined capital allocation are expected to provide a buffer against near-term macroeconomic uncertainties, including oil price volatility and geopolitical disruptions.

For India’s hotel industry, the structural drivers that emerged after the pandemic remain intact. A sustained appetite for leisure travel, rising spending on experiences and ongoing consolidation among organised players are expected to keep the sector on a firm growth trajectory, even as pricing power moderates and global economic risks become more pronounced.