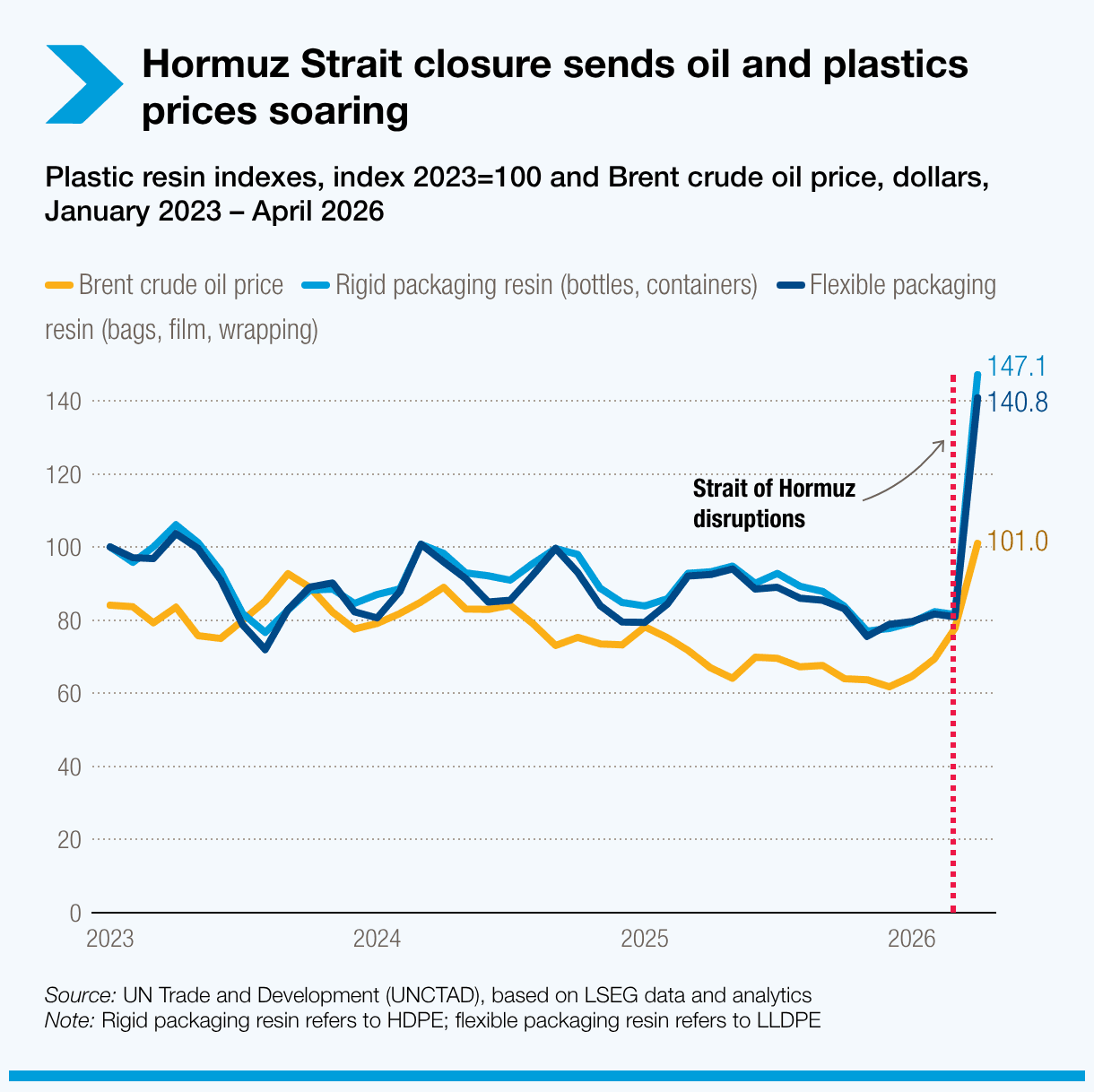

New Delhi: The latest escalation of conflict in West Asia has not only pushed up crude prices but also sent shockwaves through global commodity markets. One of the worst-hit sectors is the plastics industry, where higher oil prices are driving up production costs to unsustainable levels.

According to a news report published online by United Nations Conference on Trade and Development (UNCTAD), the crude price surge following the military escalation has already translated into rising costs for fertilizers and fuel. Less immediately visible, but equally significant, is the knock-on effect on plastics, which are deeply embedded in modern global supply chains.

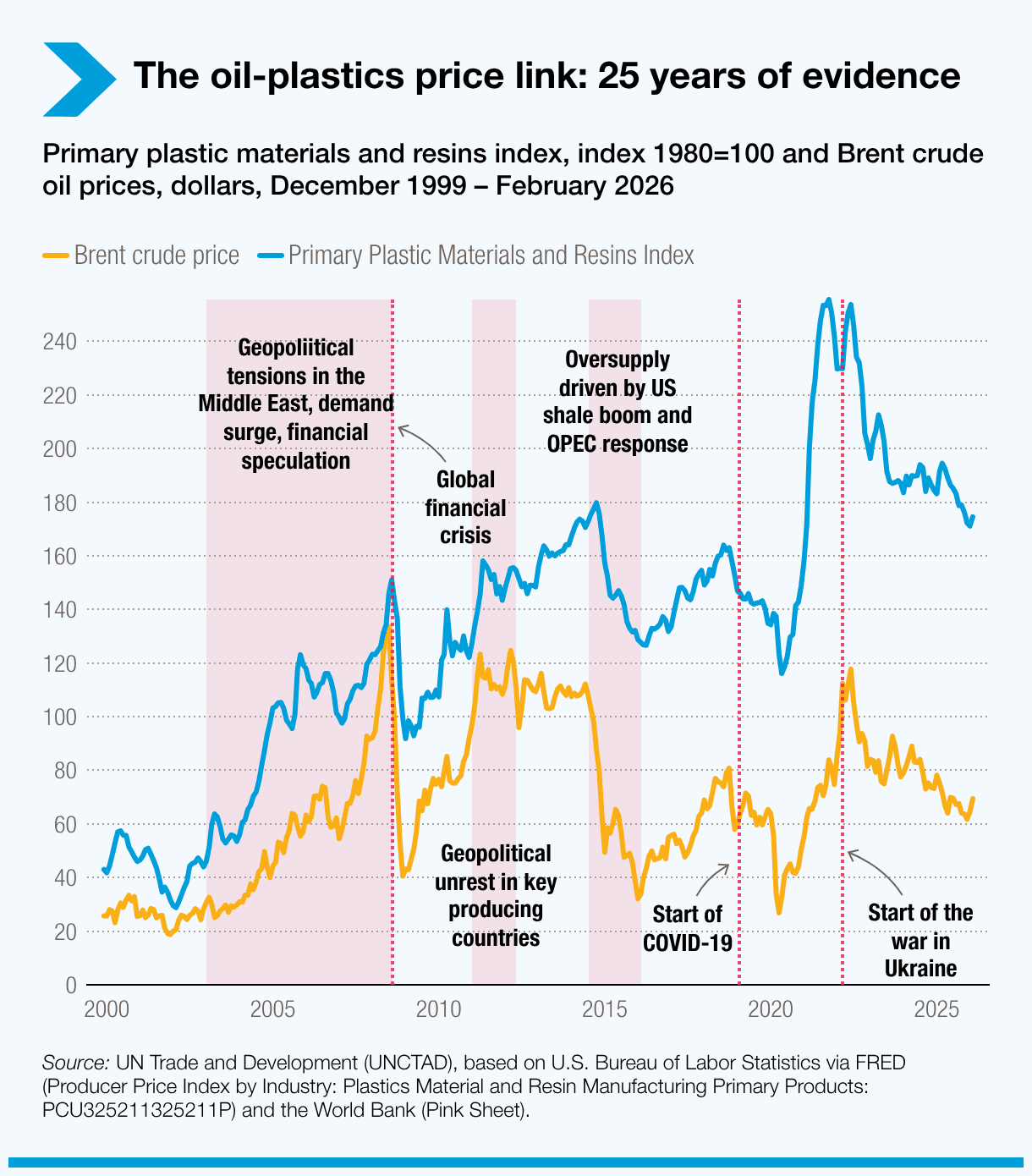

Plastics, derived largely from fossil fuels, sit at the heart of global trade, used extensively in packaging, manufacturing, and logistics. As oil prices rise, so too do the costs of producing these materials, feeding into inflationary pressures across sectors from food distribution to consumer goods. Yet, even as the economic case for alternatives strengthens, structural barriers in global trade continue to favour fossil-fuel-based plastics over greener substitutes.

This imbalance is not merely a market anomaly; it reflects long-standing policy distortions. Tariffs on plastics have steadily declined over the years, averaging 7.2%, while natural substitutes face significantly higher tariffs of 14.4%. The disparity effectively penalises environment-friendly materials such as seaweed-based packaging, pineapple fibre composites, and banana fibre textiles — many of which are produced in developing economies.

The implications are profound. Countries that are best positioned to supply sustainable alternatives are often those most constrained by trade barriers. This disconnect not only limits their ability to scale production but also raises the global cost of transitioning to greener materials. In effect, the system incentivises continued reliance on fossil-fuel-derived plastics, even as their economic and environmental costs escalate.

The UNCTAD report quotes Balasaheb Gavane, CEO of a Tanzanian company working with the UK-UNCTAD SMEP Programme, saying, “Plastic packaging costs have spiked… Alternatives exist, but without reliable supply, clear standards and competitive pricing, switching at scale remains difficult.” His remarks capture a central tension in the current moment: the world is increasingly aware of the need to shift away from plastics, yet the infrastructure and policy frameworks required to enable that shift remain underdeveloped.

Inconsistent Standards For Alternatives

The problem is compounded by fragmented regulatory systems. Inconsistent standards across countries create compliance challenges that disproportionately affect smaller producers in developing markets. International frameworks, including those under systems such as ‘Codex Alimentarius’, have yet to fully adapt to the growing role of bio-based materials. As a result, exporters of natural substitutes often face complex certification requirements, unclear quality benchmarks, and unpredictable market access conditions.

Seaweed offers a telling example. Abundant in many coastal developing countries, it has emerged as a promising raw material for biodegradable packaging and other applications. However, its potential remains largely untapped due to regulatory gaps and limited integration into global trade systems. Without harmonised standards and clearer classification within trade frameworks, scaling seaweed-based products remains a challenge.

The textiles industry reflects a similar dynamic. Around 60% of global textile production is based on synthetic fibres such as polyester, which are derived from fossil fuels. These materials are not only energy-intensive to produce but also contribute significantly to environmental degradation, including an estimated 9% of ocean micro-plastic pollution. Despite growing consumer awareness and demand for sustainable fashion, natural fibres continue to struggle against cost and accessibility barriers.

“Demand is growing, but supply chains are not yet structured to move these materials efficiently,” Muzzamal Hussain of Pakistan’s National Textile University told UNCTAD. His observation points to a broader structural issue: the global trade system has been optimised over decades for fossil-based materials, leaving newer, sustainable alternatives at a systemic disadvantage.

Oil price volatility is now bringing these structural imbalances into sharper focus. As the cost of plastics rises in tandem with crude oil, the economic argument for switching to natural substitutes becomes more compelling. However, without corresponding reforms in trade policy and supply chain infrastructure, that shift remains constrained.

Cost, Scale & Policy

At the heart of the issue is the interplay between cost, scale and policy. Fossil-fuel-based plastics benefit from established supply chains, economies of scale, and relatively low trade barriers. Natural alternatives, by contrast, often face higher upfront costs, fragmented production networks, and limited access to global markets. This creates a paradox where environmentally sustainable options are economically disadvantaged, even as their long-term benefits become increasingly evident.

The news report highlights the need for a coordinated global response to address these challenges. Aligning tariffs between plastics and their natural substitutes would be a critical first step, helping to level the playing field and encourage investment in sustainable materials. Equally important is the development of clear and consistent standards that can facilitate trade and reduce compliance costs.

Strengthening supply chains is another key priority. This involves not only improving logistics and infrastructure but also fostering partnerships between producers, manufacturers, and retailers. By building more integrated and efficient networks, it becomes possible to scale up production of natural materials and bring down costs over time.

Efforts are already under way in this direction. The UN trade body is actively engaged in discussions at the World Trade Organization and in negotiations towards a global plastics treaty. These initiatives aim to address the environmental impact of plastics while also creating opportunities for sustainable alternatives to gain traction in global markets.

However, progress remains uneven, and the urgency of the situation is growing. The current oil price shock serves as a stark reminder of the interconnectedness of global trade and the vulnerabilities inherent in a system heavily reliant on fossil fuels. It also highlights the missed opportunity to accelerate the transition to greener materials at a time when economic conditions might otherwise support such a shift.

For developing countries, the stakes are particularly high. Many of these nations possess the natural resources and labour capacity needed to produce sustainable alternatives at scale. Yet without supportive trade policies and investment in infrastructure, they risk being sidelined in the global transition to a greener economy.

Economic Impacts

The broader economic implications are equally significant. As businesses grapple with rising input costs, the ability to access affordable and sustainable materials becomes a critical factor in maintaining competitiveness. Companies that can successfully integrate natural substitutes into their supply chains may gain an advantage, both in terms of cost resilience and alignment with evolving consumer preferences.

At the same time, consumers are becoming more attuned to the environmental impact of the products they use. This shift in demand is creating new market opportunities for sustainable materials, but also increasing pressure on companies to adapt. The challenge lies in bridging the gap between demand and supply — a gap that is currently widened by trade barriers and regulatory inconsistencies.

The issue is not just about plastics or oil prices; it’s about the structure of global trade itself. The current system, shaped by decades of industrial development and policy decisions, continues to favour established, fossil-based industries. Rebalancing that system to support sustainable alternatives will require a concerted effort from governments, international organisations, and the private sector.

The path forward is clear, if not easy. Reducing tariffs on natural substitutes, harmonising standards, and investing in supply chains are all achievable goals. What is needed is the political will to implement these changes and the recognition that the cost of inaction is likely to be far greater.

As oil markets remain volatile and environmental concerns continue to mount, the pressure to reform the global plastics economy will only intensify. The question is whether the world can seize this moment to create a more balanced and sustainable trade system, or whether it will allow existing barriers to persist, holding back the very solutions that are needed most.