New Delhi: The Iran conflict has done what years of tariff wars, inflation shocks and monetary tightening could not — it has forced the World Bank to slash its global growth outlook and warn that the world economy is facing another defining crisis. Yet, amid the gloom, India has emerged as a rare outlier, with growth projected at 6.6%, reinforcing its position as the fastest-growing major economy despite an increasingly hostile global environment.

The World Bank’s Global Economic Prospects, June 2026 paints a sobering picture of an economy once expected to stabilise after the pandemic but instead being dragged into another geopolitical shock. Global growth is now projected at just 2.5% in 2026, down from 2.9% last year, as the Iran-linked conflict in West Asia disrupts energy supplies, drives up commodity prices and revives inflationary pressures.

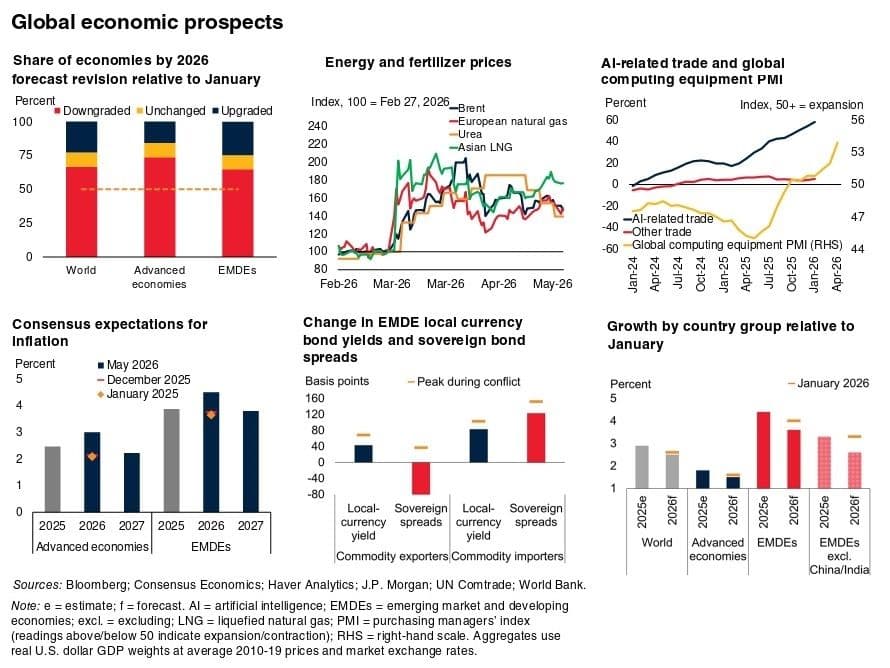

“The global economy is facing another major shock,” says the report. According to the report, the conflict has triggered sharp increases in energy prices, renewed inflationary pressures and expectations of tighter monetary policy, significantly weakening growth prospects for energy-importing economies.

The numbers underline the scale of the disruption. The World Bank expects overall commodity prices to jump by 22% this year, a dramatic reversal from the decline projected just months ago. Brent crude oil is forecast to average $94 a barrel, up 36% from 2025 levels and more than 50% above the Bank’s January estimate. European natural gas prices are expected to climb about 30%, while fertiliser prices have also surged because of supply disruptions in the Gulf region.

For India, which imports nearly 90% of its crude requirements, the oil shock could prove to be the single biggest external risk to growth. Higher energy prices threaten to feed inflation, widen the trade deficit and complicate the Reserve Bank of India’s monetary policy calculations. Even so, the report projects India’s economy to expand by 6.6% in FY2026-27 before recovering to 7.2% the following year.

India Stands Apart

India’s resilience is even more striking when viewed against the global backdrop. Emerging market and developing economies are expected to slow to 3.6%, while growth in advanced economies is forecast at just 1.5%. The Middle East, North Africa, Afghanistan and Pakistan region is expected to witness one of the sharpest slowdowns, with growth collapsing to 1.6% from 4% last year.

South Asia is projected to grow by 6.3%, largely because of India’s economic strength. The country’s domestic demand, infrastructure spending and investment momentum continue to provide buffers against external shocks.

But the World Bank makes it clear that India is not insulated from global turbulence. According to the report, slower global growth translates into reduced investment, constrained hiring and tighter fiscal space, making job creation a bigger challenge across developing economies.

One of the more striking findings is that nearly two-thirds of economies across the world have seen their growth forecasts downgraded since the Bank’s January assessment. The deterioration has been so broad-based that the report warns of nearly a decade of lost income convergence for emerging economies excluding China and India.

The report also highlights an overlooked consequence of the conflict — the disruption of fertiliser trade. With the Gulf accounting for a significant share of global fertiliser exports and natural gas prices surging, agricultural costs could rise worldwide, adding another layer to food inflation risks.

Another worrying trend is the rapid rise in government debt. According to the report, elevated debt levels are increasing borrowing costs and eroding fiscal space, leaving governments with fewer resources for infrastructure, public services and investment needed to create jobs and sustain long-term growth.

A Lost Decade?

Perhaps the most arresting message in the report comes not from the economic forecasts but from its broader assessment of the decade.

“Barring a miracle, the 2020s will prove to be... a lost decade,” writes Indermit Gill, Senior Vice President and Chief Economist of the World Bank Group. He argues that repeated global shocks have prevented many developing economies from narrowing the income gap with richer nations.

The report notes that by the end of 2026, one-fourth of developing economies, one-third of low-income countries and half of fragile and conflict-affected economies will still be poorer than they were before the pandemic.

According to the report, private investment growth in developing economies during the 2020s has more than halved compared with the previous decade, while government debt has climbed to record highs.

The World Bank also sketches out a darker scenario. If energy supply disruptions become more severe and financial markets come under significant stress, global growth could plunge to just 1.3% this year. Inflation would rise further, commodity prices could spike again and financial conditions could tighten sharply.

Yet the report is not entirely pessimistic. It identifies three major opportunities capable of reshaping the global economy — AI, the clean energy transition and expanding regional trade.

“AI would, in short, usher in the world’s most prosperous decade since the 1970s,” Gill says, provided governments build the digital infrastructure and skills needed to harness the technology.

The report notes that clean energy now accounts for two-thirds of global investment in energy and reached a record $2.2 trillion in 2025. Regional trade agreements have also expanded rapidly and now account for about 60% of global trade, providing an alternative source of economic stability amid geopolitical fragmentation.

For India, these trends present both opportunities and challenges. The country stands to benefit from the global realignment of supply chains, digital investments and clean energy expansion. But it must also contend with higher oil prices, volatile commodity markets and slowing external demand.

The World Bank’s latest assessment ultimately offers a mixed verdict. India’s economy remains among the strongest in the world and continues to outperform most major peers. But in an increasingly fractured global economy shaped by conflict, commodity shocks and geopolitical uncertainty, sustaining that advantage will require careful macroeconomic management and accelerated structural reforms. The message from Washington is clear: India may be a bright spot, but it cannot afford to ignore the gathering global storm.