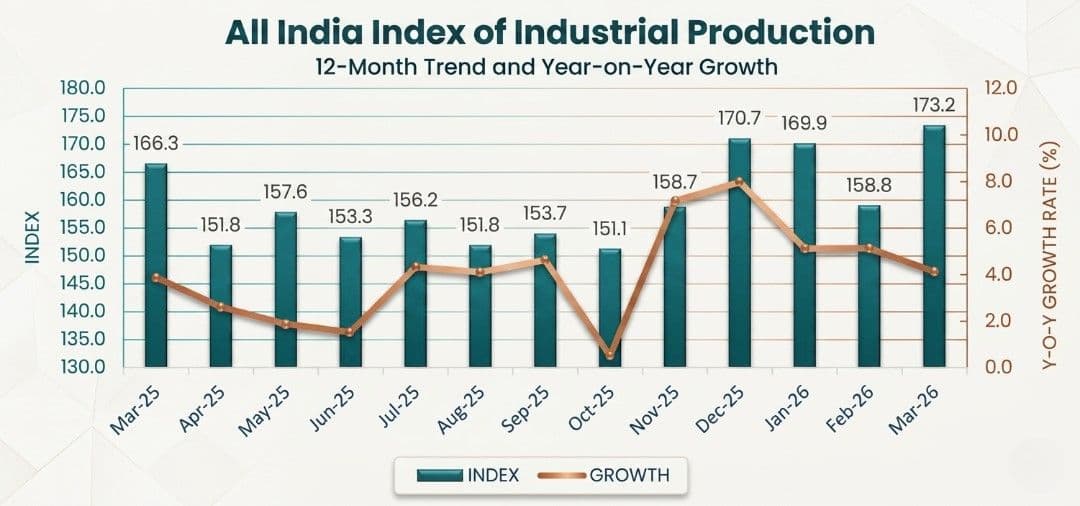

New Delhi: India’s industrial production growth slowed to a five-month low of 4.1% in March 2026, reflecting a combination of subdued manufacturing activity and near-stagnation in the power sector, even as mining output showed a marked improvement. The latest data, released by the National Statistics Office (NSO), underscores the uneven momentum within the economy amid external pressures, including disruptions linked to the West Asia crisis.

Factory output, measured by the Index of Industrial Production (IIP), expanded at a marginally higher pace than the 3.9% recorded in March 2025, but the deceleration from recent months highlights emerging stress points. The NSO also revised February 2026 growth slightly downward to 5.1% from the earlier estimate of 5.2%, reinforcing the narrative of softening industrial traction. The last time IIP growth had dipped lower was in October 2025, when expansion slowed sharply to just 0.5%.

Manufacturing, which carries the largest weight in the IIP, remained tepid, growing 4.3% in March 2026 compared with 4% in the corresponding month a year earlier. While the sector managed to sustain positive growth, the pace indicates limited demand-side strength and lingering cost pressures.

In contrast, mining emerged as a relative bright spot, with output expanding 5.5%, a sharp improvement over the modest 1.2% growth recorded in March 2025. This uptick provided some cushion to overall industrial performance.

The power sector, however, was a significant drag. Electricity generation grew by just 0.8% in March, a steep fall from the robust 7.5% expansion seen a year earlier. The near-flat growth in power output points to both demand moderation and possible supply-side constraints, exacerbated by global geopolitical uncertainties.

For the full fiscal year 2025-26, industrial production growth remained broadly unchanged at 4.1%, compared with 4% in the previous year, suggesting that headline stability masks underlying sectoral divergence.

A closer look at manufacturing reveals a mixed picture. Of the 23 industry groups within the sector, 14 recorded positive growth in March 2026 over the year-ago period. The strongest contributions came from the manufacture of basic metals, which grew 8.6%, followed by motor vehicles, trailers and semi-trailers at a robust 18.1%, and machinery and equipment at 11.2%. Within basic metals, key drivers included MS slabs, flat products of alloy steel, and hot-rolled coils and sheets of mild steel, indicating sustained activity in core industrial inputs.

Use-based classification data further illustrates the divergence in demand segments. Capital goods stood out with a sharp 14.6% growth, signalling continued investment activity. Infrastructure and construction goods also posted a healthy 6.7% increase, pointing to ongoing public and private sector project execution.

Consumer-facing segments, however, remained relatively subdued. Consumer durables grew 5.3%, while consumer non-durables expanded just 1.1%, indicating cautious household spending. Primary goods recorded a modest 2.2% growth, and intermediate goods rose 3.3%, reflecting moderate momentum in the supply chain.

In index terms, primary goods stood at 173.3, capital goods at 156.2, intermediate goods at 181.4, and infrastructure/construction goods at 229.0 in March 2026. Consumer durables and non-durables were pegged at 146.2 and 150.6, respectively.

The IIP data paints a picture of an industrial sector navigating cross-currents — resilient investment demand and mining output on one hand, and subdued consumption and energy sector weakness on the other. The trajectory in the coming months will hinge on how these competing forces evolve, particularly in the context of global uncertainties and domestic demand conditions.

(Cover photo by Zoshua Colah on Unsplash)