New Delhi: India’s media and entertainment (M&E) industry entered 2025 at a defining inflection point, marked not just by scale, but by a structural shift in how content is created, distributed, and consumed. Technology, storytelling, and evolving audience behaviour are converging to reshape a more integrated ecosystem.

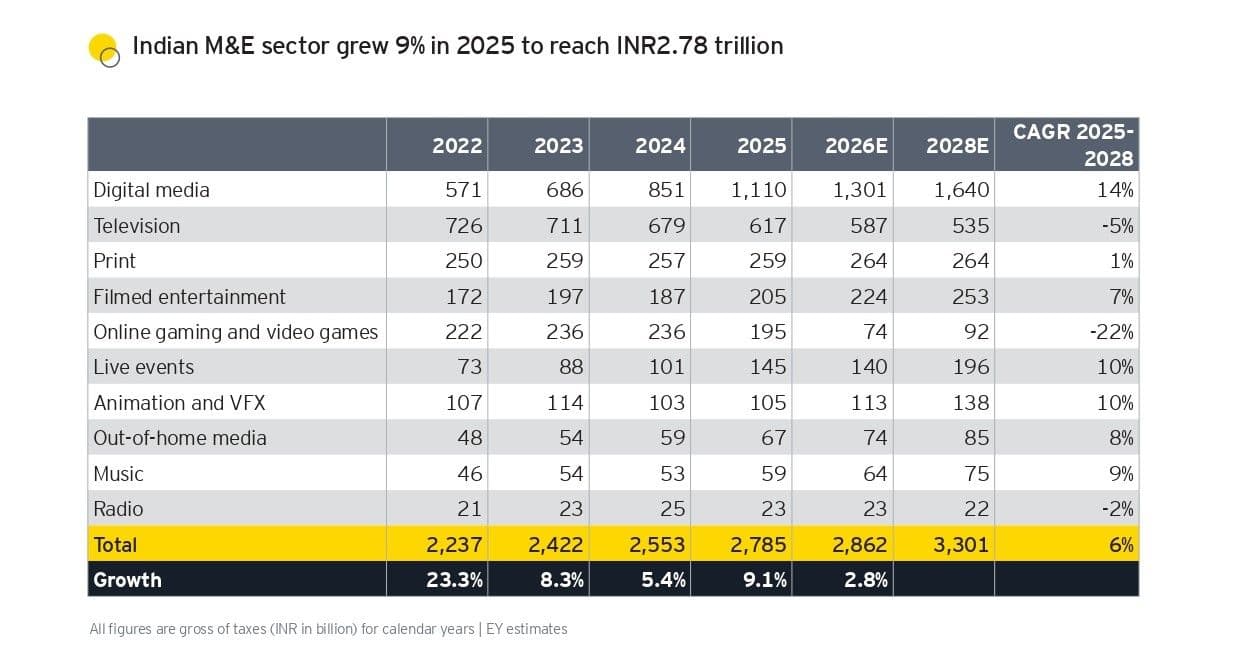

The sector grew 9.1% in 2025 to reach ₹2.78 lakh crore, outpacing India’s nominal GDP per capita growth of 7.7%. Excluding regulatory disruptions in online gaming, growth stood stronger at 11.8%, underscoring the industry’s underlying resilience. M&E now contributes roughly 0.8% to GDP, supporting 27.5 lakh direct jobs and over one crore indirect jobs, making it both an economic and cultural force.

Advertising emerged as a key growth engine, expanding 13.5% and outpacing the broader industry. This was driven by the rise of e-commerce, growth in point-of-sale advertising, and improved credit access for MSMEs, whose share in industrial credit reached 33% by December 2025. Despite this momentum, India’s ad-to-GDP ratio remains just 0.41%, leaving significant room for expansion.

Digital advertising continues to dominate, accounting for 63% of total ad revenues and growing 26% to ₹94,700 crore. Within this, e-commerce and point-of-sale advertising surged 50% to ₹22,000 crore, as brands increasingly favoured performance-driven, measurable platforms. Over 10 lakh long-tail advertisers contributed ₹36,300 crore, highlighting how digital has democratized marketing. Connected TV advertising also grew strongly, rising from ₹6,900 crore to ₹9,900 crore, supported by a 35% increase in subscriptions and access to affluent audiences.

Content production remains the backbone of the industry. “India’s storytelling ecosystem continues to thrive, producing nearly 200,000 hours of content in 2025, with 96% created for television (excluding news bulletins). OTT platforms, films, and short-form formats also complement this scale, creating a rich multi-platform ecosystem where audiences consume stories on their terms,” notes Kevin Vaz, Chairman, Ficci M&E Committee.

The film industry had a record year with over 1,900 releases and 37 films crossing ₹100 crore, reaffirming the enduring appeal of theatrical entertainment even in a digital-first era.

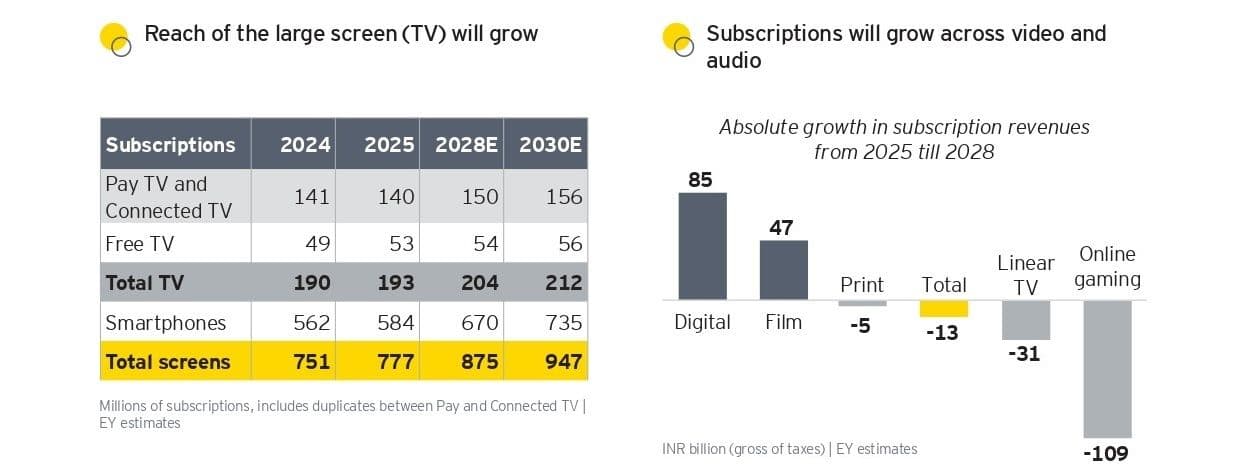

Digital media has been the most transformative force, overtaking television as the largest segment. The OTT market alone crossed ₹27,200 crore. Paid video subscriptions reached 21.6 crore across 14.3 crore households, while digital subscription revenues rose 60% to ₹16,300 crore. Music streaming subscriptions grew 37% to 1.44 crore users, driven by tighter limits on free consumption. However, digital news subscriptions remain low at around 40 lakh, reflecting persistent monetization challenges.

Regional content has become a major growth driver. It now accounts for 56% of OTT consumption, up from 27% in 2020, while contributing over 65% of film production. This reflects both cultural diversity and strategic expansion, enabling platforms to deepen engagement across India’s vast audience base.

Traditional media continues to adapt. Television still reaches about 74.5 crore viewers weekly, but linear TV advertising declined 10.3% and subscription revenues fell 8%, following the loss of 1.1 crore pay-TV households. At the same time, Free TV and Connected TV are expanding, signalling a hybrid future where linear and digital coexist. Print remained stable, with advertising growing 2%, particularly in premium segments, even as younger audiences move away from physical circulation.

Out-of-home (OOH) media grew 13%, driven by premium inventory and digital formats, which now contribute 18% of segment revenues. Live events were among the fastest-growing segments, with the organized sector expanding 44%. Growth was fuelled by concerts, weddings, government events, and large religious gatherings such as the Maha Kumbh Mela, reflecting rising demand for shared, immersive experiences.

Technology is now central to industry evolution. AI is enabling personalization, localization, and efficiency at scale — from content recommendations to advanced production and immersive sports broadcasts. These innovations are deepening engagement and unlocking new revenue streams.

India’s music industry reflects this diversification. While digital licensing growth has slowed due to declining platform returns, revenues from OTT, social media, and live events have increased. Labels are expanding into talent management, branded content, and live experiences, with non-traditional revenues rising 26%.

Not all segments grew. Radio declined 7%, affected by falling ad rates and structural shifts such as the removal of FM receivers from newer devices. Online gaming contracted 17% due to regulatory disruptions, although in-app purchases rose 15%, signalling a shift in monetization models.

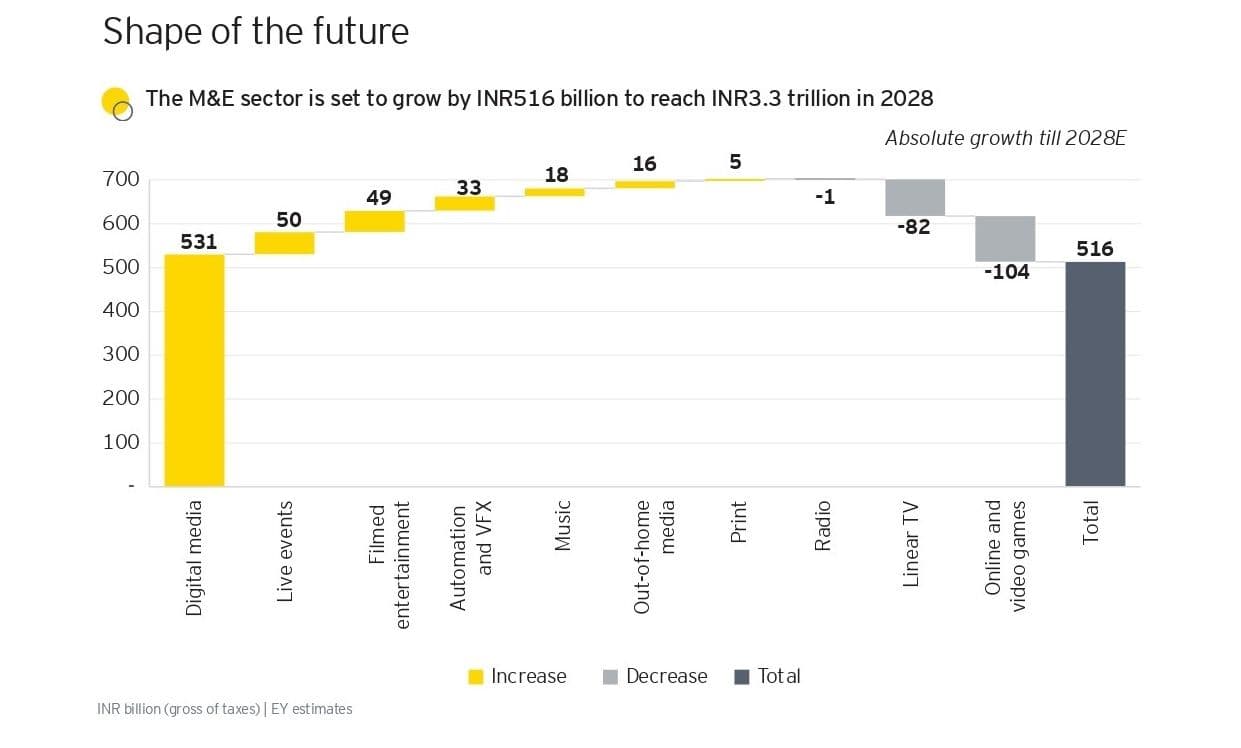

Looking ahead, the industry is expected to grow 2.8% in 2026 to ₹2.86 lakh crore, with underlying growth closer to 8% excluding gaming disruptions. Over the medium term, it is projected to grow at a CAGR of over 7%, reaching ₹3.30 lakh crore by 2028. Paid subscriptions alone are expected to rise nearly 30% over the next two years, reinforcing the shift toward consumer-funded models.

Ultimately, India’s M&E story is one of convergence — between traditional and digital platforms, mass and premium audiences, and local and global content. The industry is no longer defined by individual segments, but by an interconnected ecosystem where content flows seamlessly across formats and geographies.

“As the boundaries between consumer and creator continue to blur, understanding not only what people watch but why they do so, becomes central to unlocking the next phase of growth,” feels Ashish Pherwani, M&E Sector Leader, EY India.

With a young, digitally connected population, strong storytelling capabilities, and rapid technological advancement, India is well positioned to become a global content powerhouse. The next phase will depend on building strong intellectual property, improving monetization frameworks, and fostering deeper collaboration between industry and policymakers.

In 2025, India’s M&E industry did more than grow. It evolved into a more dynamic, diversified, and future-ready ecosystem.