New Delhi: India’s projected economic growth of 7.0% to 7.4% (at constant prices) for the 2026-27 fiscal year is exposed to potential downside risks, as highlighted in the Finance Ministry’s monthly report released on Saturday. The report points to rising energy prices and supply chain disruptions linked to the conflicts in West Asia as key factors that could weigh on the outlook.

Domestic demand has remained relatively stable so far, but risks to growth are rising, particularly in sectors reliant on imported inputs, says the report, which emphasised that India will need to provide immediate, targeted relief to the most affected and vulnerable businesses and households to cushion the potential impact.

“Clearly, there is considerable downside to this (growth) number. Data for March will not reveal much, since businesses are trying to meet full-year targets for FY26,” notes V Anantha Nageswaran, Chief Economic Advisor, Government of India, in the report, adding high-frequency data for April and possibly May “may give a better handle” on the likely growth rate for the new financial year.

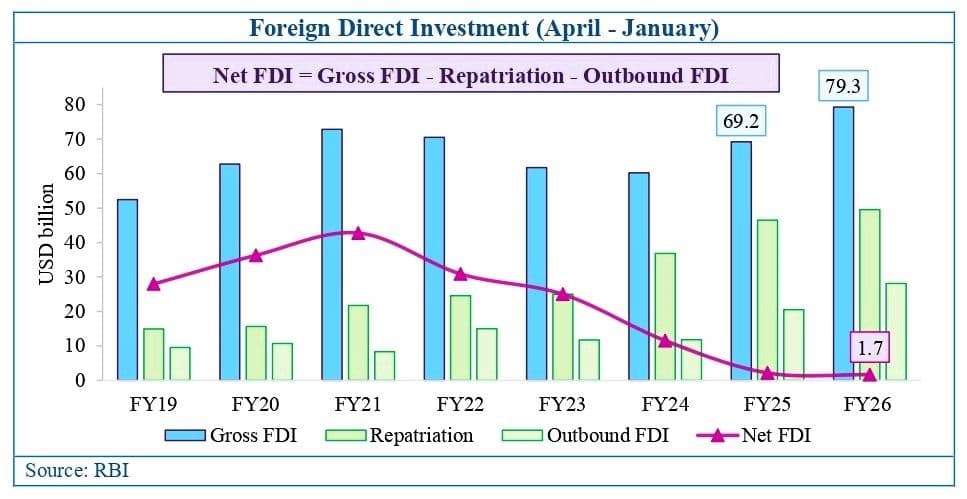

The report also flagged concerns over external balances, stating that the current account deficit is expected to widen significantly in FY27. While gross foreign direct investment (FDI) inflows have remained steady, net capital flows have declined sharply in recent years, reflecting heightened global uncertainty and weaker investor sentiment.

Policy Push

To sustain investment attractiveness, the report underscored the need for continued reforms aimed at lowering manufacturing costs. Suggested measures include reducing tariffs on industrial power, introducing flexibility in labour arrangements such as averaging working hours over longer periods, and cutting overtime costs. It also highlighted the importance of ensuring tax policy certainty, stability and continuity in the current environment.

“Given the considerable impact of the conflict on India’s economy, we should leverage the fallout to redouble our recent reform efforts to enhance India’s competitiveness and preparedness. The ‘entrepreneurial mindset’ in bureaucracy (not making the ‘best’ the enemy of the ‘good’), accompanied by enhanced speed of decision-making, is precisely what is called for if India is to emerge from this episode stronger, more resilient and more competitive,” said Nageswaran.

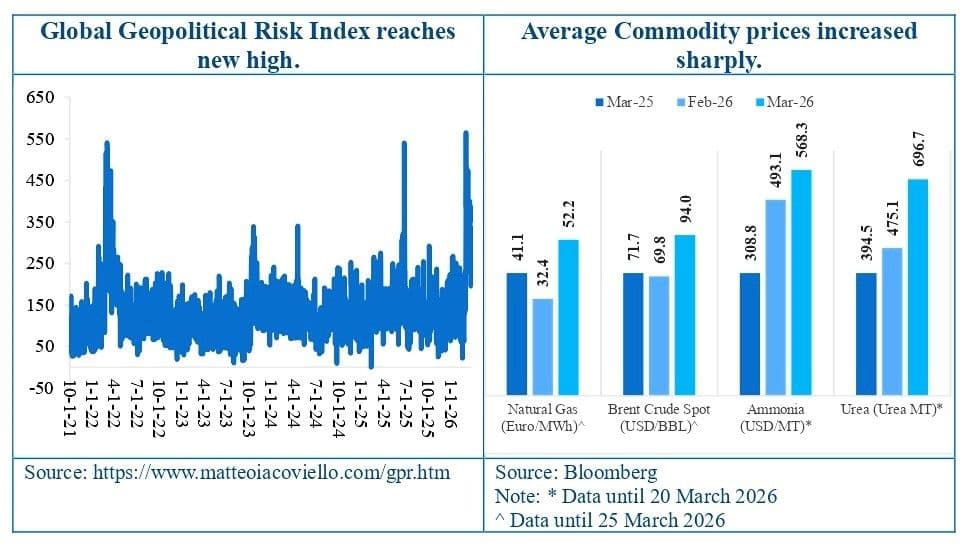

The economic outlook has grown increasingly uncertain amid escalating geopolitical tensions in West Asia, which have disrupted key energy and logistics channels and tightened global supply conditions. Although economic activity remained robust up to February, early signs suggest that recent shocks are being transmitted through higher input costs and supply constraints, with some moderation in activity emerging.

Growth Signals

Industrial performance in February reflected mixed trends. While hydrocarbon output contracted due to global energy uncertainties, domestic demand-driven sectors showed resilience. Growth in steel and cement production, along with steady expansion in coal and fertilisers, pointed to continued strength in infrastructure and construction, supported by public capital expenditure and supply-side initiatives such as the Bharat Audyogik Vikas Yojna (BHAVYA).

Inflationary pressures showed a mild uptick, with retail inflation rising to a 10-month high of 3.21% in February, driven largely by food prices. However, the data does not yet fully capture the potential impact of rising crude oil prices, which pose an upside risk in the coming months, says the report.

Financial conditions remained supportive, with bank credit growth accelerating to 14.5% (YoY) in February and overall financial resource flows to the commercial sector rising 33.2% (YoY).

On the external front, merchandise exports dipped marginally by 0.8% (YoY) in February, although non-petroleum, non-gems and jewellery exports recorded a healthy growth of 6.6% (YoY). Services exports continued to underpin trade performance, with the services trade surplus covering 85.4% of the merchandise trade deficit.

The current account deficit widened to 1.3% of GDP in Q3 FY26 from 1.1% a year earlier, largely due to a higher merchandise trade deficit. Despite an increase in gross FDI inflows during April-January of FY26, net FDI remained subdued and negative for five consecutive months, while portfolio flows turned negative in March amid declining global risk appetite.

Foreign exchange reserves remained comfortable, covering more than 11 months of goods imports. The labour market also showed resilience, with higher participation rates, declining unemployment, and steady hiring across sectors. The unincorporated sector recorded robust performance in 2025, supported by improved wages, productivity gains, and increased digital adoption.

“The Government has undertaken a range of measures to manage supply disruptions, ensure energy availability, support trade and logistics, and maintain overall economic stability. While these interventions, along with existing macroeconomic buffers, provide some support, the balance of risks remains tilted to the downside. In this context, continued vigilance and proactive policy measures will be important to mitigate the impact of evolving global uncertainties,” suggests the report.