New Delhi: India’s money story is no longer about cash versus digital. It is about both rising together — but for different reasons.

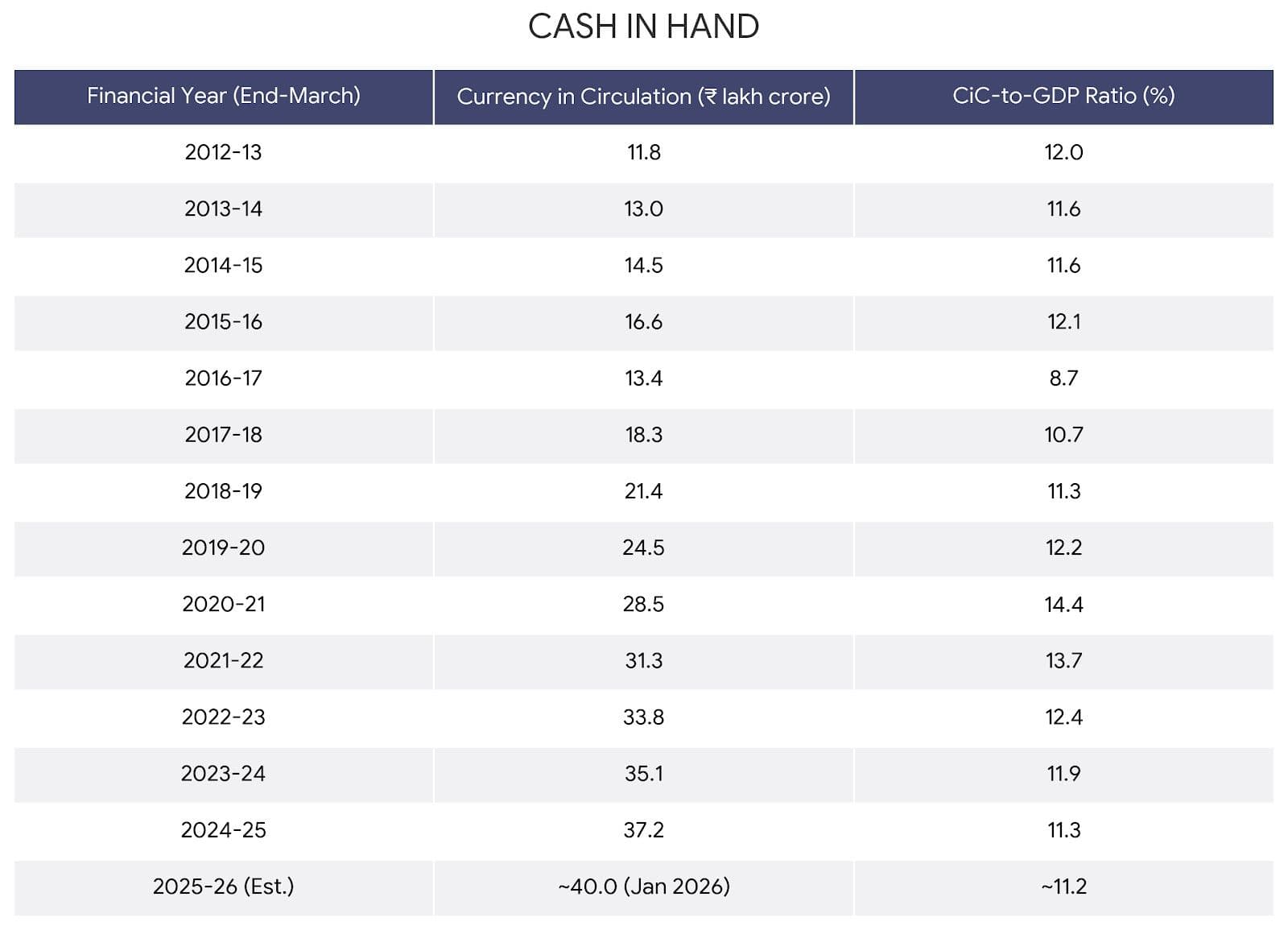

According to the latest Ecowrap report by the State Bank of India (SBI) Research, currency in circulation (CiC) touched nearly Rs 40 lakh crore by January 31, 2026, growing 11.1% year-on-year. This is much faster than the 5.3% growth seen a year earlier. In simple terms, more cash is physically present in the system than ever before.

At the same time, digital payments — especially through the National Payments Corporation of India’s Unified Payments Interface (UPI) — are breaking records. Monthly UPI transactions have reached about Rs 28 lakh crore in value. That means digital payments every month are equivalent to roughly 70% of the total cash available in the economy.

So why is cash still growing if digital payments are booming?

Cash is rising, but its importance is shrinking

While the total amount of cash has increased, its importance relative to the economy has actually fallen. The cash-to-GDP ratio has dropped from 14.4% in FY21 to around 11% in FY26. This tells us that although more currency notes are now in circulation, India’s economy is growing even faster — and digital payments are expanding faster than cash.

ATM withdrawals have remained steady at around Rs 2.5 lakh crore per month on average. This suggests that cash usage has not collapsed; instead, it has stabilized even as digital modes expand rapidly.

The real shift is happening in small-value transactions. Data show that 86% of person-to-merchant UPI transactions are below Rs 500. This indicates that people are increasingly using UPI for everyday purchases — groceries, tea, auto fares — where small notes were once dominant.

Interestingly, the Rs 500 note has become even more dominant in the cash system after the withdrawal of the Rs 2,000 note in 2023. High-value notes now account for a larger share of total currency value. This suggests that while digital is replacing smaller notes, larger notes continue to circulate for savings, precautionary needs, or bigger cash transactions.

Cash behaviour is not uniform across India. Some states such as Karnataka, West Bengal and Tamil Nadu have seen stronger ATM withdrawal trends compared with previous years. In Karnataka, researchers found that districts with high ATM usage before July 2025 saw further increases in withdrawals after GST scrutiny notices were issued to certain traders with high digital turnover.

This suggests an important behavioural insight: when small businesses fear closer tax scrutiny linked to digital trails, some may temporarily shift back to cash. However, this pattern was not uniform across all states, indicating that such responses are localized rather than nationwide reversals.

SBI Research finds that lower interest rates tend to increase demand for cash. When returns on savings are lower, people may prefer holding more liquid money. Deposit growth has been moderate at about 10.6%, which may also be nudging households — especially in rural areas — to keep more cash on hand for consumption and precautionary purposes.

Gold imports and liquidity recycling

India’s gold imports remain elevated, but the report suggests a different dynamic from earlier years. Instead of people shifting away from financial assets, households may be liquidating gold holdings amid high prices and converting them into cash for spending. This reflects asset recycling rather than a retreat from formal finance.

The coexistence of high cash levels and record digital payments is not a contradiction — it reflects a transition phase in a growing economy.

Digital payments are clearly deepening ‘financialization’ and improving transparency. Small-ticket payments are increasingly cashless. But cash still plays an important role in liquidity management, rural consumption, savings habits and behavioural responses to policy signals.

The SBI Research report notes that policy actions should avoid unintentionally discouraging digital payments. Even in a maturing digital ecosystem, abrupt enforcement or compliance shocks can push some users temporarily back toward cash.

India’s financial system, therefore, is not choosing between cash and digital. It is evolving into a hybrid model — where digital dominates transactions, but cash remains a trusted store of liquidity.