New Delhi: India’s private sector is signalling a cautious turn in its investment outlook, with fresh data pointing to a notable pullback in capital expenditure (capex) plans for the 2026-27 financial year. The latest survey by the Ministry of Statistics & Programme Implementation suggests that corporate India may be preparing to tighten its purse strings after a period of steady investment alignment.

According to the survey, private sector capital expenditure on the acquisition of new assets is projected to decline by 16.5% to ₹9.55 lakh crore in FY27. This marks a significant drop from the provisional estimate of ₹11.43 lakh crore for FY26, indicating a more conservative stance among enterprises as they look ahead.

Despite this anticipated slowdown, past investment behaviour reflects a high degree of accuracy in corporate planning. The actual capex incurred during FY25 stood at ₹173.5 crore per enterprise, closely tracking the intended ₹180.2 crore reported in the earlier CAPEX-2024 survey. This resulted in a realization ratio of 96.3%, underscoring that companies largely executed their investment plans as envisaged.

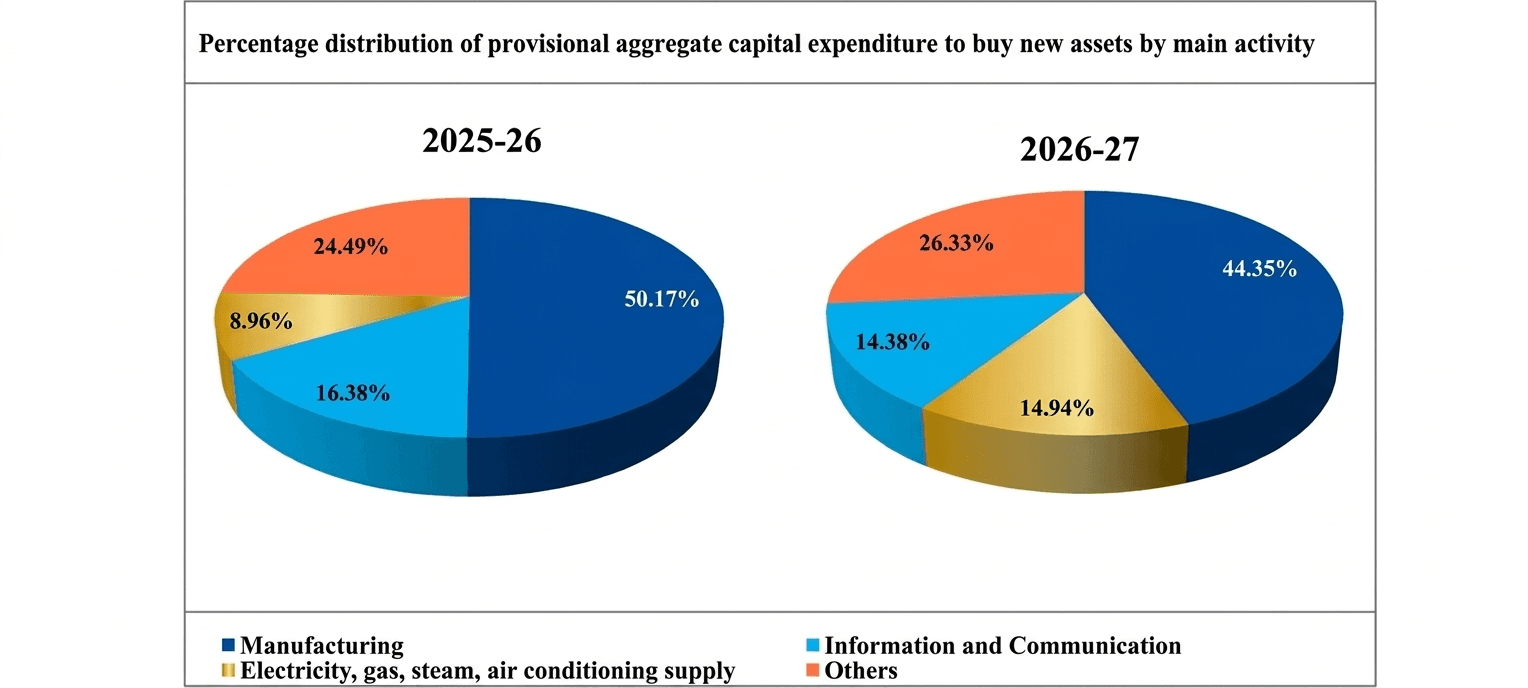

The survey reveals that investment strategies in FY26 were predominantly centred around strengthening core operations. About 48.63% of enterprises focused on core assets, while 38.36% channelled funds into value addition of existing assets. A smaller segment, 14.54%, pursued opportunistic investments, while less than 4% adopted debt-related strategies and around 1.0% targeted distressed assets or non-performing loans. Notably, 20.15% of enterprises did not specify any particular investment strategy.

In terms of intent, capex spending was largely driven by the need to generate income, with 60.13% of enterprises citing this as their primary objective during FY26. Upgradation of existing capacity was another major driver, reported by 42.12% of firms. Meanwhile, 7.2% of enterprises invested with diversification goals, and 17.64% cited other reasons not explicitly captured in the survey.

Financing patterns further highlight the cautious approach of the private sector. Internal accruals remained the dominant source of funding, accounting for 65.35% of total capex in FY26. Domestic debt emerged as the second-largest contributor at 23.25%, followed by equity raised within the country at 3.78%. External financing played a limited role, with 1.04% of capex funded through the FDI route and 2.38% through foreign debt.

The survey, conducted by the National Statistics Office, covered a broad sample of enterprises to gauge investment trends. Out of 7,486 enterprises approached, 5,366 were operational and responded, and 4,203 (about 78.3%) provided their capex plans for FY27. The sample included 5,795 enterprises from the census sector and 1,691 from the sample sector.

This exercise builds on the first such survey carried out between November 2024 and January 2025, with the latest round conducted from October to December 2025. The government noted that enterprises typically adopt a conservative approach when reporting future investment estimates, suggesting that actual capex outcomes for FY27 could differ from current projections.

The data offers a clear signal: while corporate India has maintained discipline in executing investment plans, uncertainty and evolving economic conditions may be prompting a more measured approach to future capital spending.

Corporate India’s overall capex during FY27-FY31 is projected at ₹145-155 lakh crore, nearly 1.5 times the investment seen in previous five years, says a Crisil report. Of this, ₹55-60 lakh crore is expected to be funded through long-term debt, with the remainder coming from budgetary support and internal accrual. (Photo by Troy Mortier on Unsplash)

Crisil Projections

A report released on March 11 by Crisil Ratings indicates that corporate India will require substantial funding to support medium-term growth. It estimates that companies will need ₹130-140 lakh crore in debt between FY27 and FY31 to finance large-scale capital expenditure in infrastructure and industrial sectors, meet working capital requirements, and sustain rising retail credit demand.

Overall capital expenditure during FY27-FY31 is projected at ₹145-155 lakh crore, nearly 1.5 times the investment seen in the previous five years. Of this, ₹55-60 lakh crore is expected to be funded through long-term debt, with the remainder coming from budgetary support and internal accruals.

The report highlights that stronger corporate balance sheets and improved risk profiles, especially in infrastructure, position companies better to undertake debt-funded investments. Median gearing among rated entities has declined to 0.4-0.5 times as of March 31, 2026, from 1.05 times in 2015, alongside steady improvements in revenue and profitability.

Median gearing describes a company’s capital structure where debt and equity are balanced, generally falling within a gearing ratio range of 0.4-0.5. It indicates that the company uses a moderate amount of debt to finance its operations and growth, but is not overly reliant on borrowing.

Infrastructure financing has also evolved, aided by better risk-sharing frameworks, increased participation from central government counterparties and the growing role of infrastructure investment trusts (InvITs). This has improved the median rating of infrastructure assets in Crisil’s portfolio from BBB+ in March 2018 to AA− by December 2025.

Beyond capex, corporates are expected to need ₹30-35 lakh crore in debt for working capital, assuming revenue growth of about 11% over five years. Non-banking financial companies are projected to raise ₹40-45 lakh crore to support around 15% growth in retail lending.

While the countries financing ecosystem, including banks, debt capital markets and external commercial borrowings, is expected to grow at 10-11% annually through FY31, Crisil estimates a potential funding gap of ₹10-20 lakh crore. The banking system remains well-capitalized, though a credit-to-deposit ratio of about 82% as of January 2026 could constrain lending expansion relative to deposit growth.

The report also points to a larger role for debt capital markets, with outstanding issuances expected to rise from ₹70 lakh crore in FY26 to ₹115-120 lakh crore by FY31. Regulatory support from the Reserve Bank of India is likely to aid external borrowings, although costs will remain sensitive to global conditions and currency volatility.

Taken together, the MoSPI survey and Crisil’s projections suggest a nuanced picture: while near-term capex intentions appear cautious, the medium-term investment cycle remains structurally strong, underpinned by healthier balance sheets and expanding financing avenues.

(Cover photo by Tye Doring on Unsplash)