New Delhi: India’s economic growth trajectory, which has demonstrated significant resilience throughout the current fiscal year, is bracing for a period of cooling, thanks largely to the escalating war in West Asia.

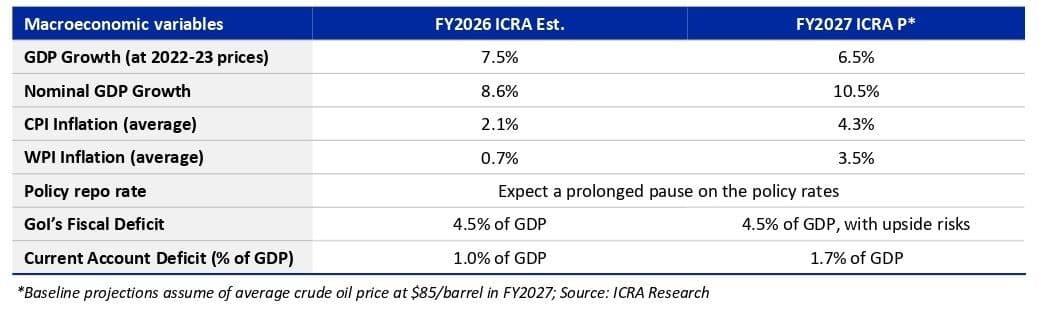

According to the latest macroeconomic update from rating agency ICRA, India’s GDP growth is projected to moderate to 6.5% in FY2027, a sharp deceleration from the 7.5% estimated for FY2026. This downward revision from an earlier forecast of 7.1% is primarily attributed to the escalating West Asia conflict, which has introduced volatility into energy markets and threatened domestic macroeconomic stability.

The primary catalyst for this cautious outlook is the heightened uncertainty in West Asia, a region critical to India's energy security and trade. West Asia currently accounts for approximately 14% of India’s exports and 20% of its imports. ICRA’s baseline projections for FY2027 assume an average crude oil price of $85 per barrel. However, the rating agency warns that if the conflict pushes prices toward the $105 per barrel mark for an extended period, the current account deficit (CAD) could widen to 2.4% of GDP, significantly higher than the 1.7% base case.

The impact of elevated energy costs is expected to be multi-dimensional. Beyond the direct hit to corporate profitability due to rising input costs, the spike in crude and natural gas prices will weigh on the fiscal deficit. Every 10% increase in crude oil prices is estimated to push the Wholesale Price Index (WPI) inflation up by 80-100 basis points and Consumer Price Index (CPI) inflation by 40-60 basis points, the ICRA report cautions.

Prior to the onset of the West Asia tensions, India’s domestic indicators showed strength. In January-February 2026, 12 of 18 key non-agricultural high-frequency indicators saw year-on-year (YoY) improvement compared to the third quarter of FY2026. Notably, two-wheeler production and vehicle registrations maintained double-digit growth, buoyed by GST rate cuts and healthy rural demand.

Despite these pockets of strength, urban sentiment remains in the “pessimistic zone”. The Reserve Bank of India’s Current Situation Index (CSI) eased to 98.1 in January 2026, down from 98.4 in November 2025. While the retail sale of passenger vehicles rose by 13% during the first 11 months of FY2026, ICRA notes that recent credit card spending has shifted toward lower-value transactions, suggesting a cooling of discretionary big-ticket spending.

On the investment front, the government’s continued capital expenditure drive remains a critical pillar. The FY2027 Union Budget has pencilled in a 12% growth in on-budget capex, representing 3.1% of GDP. This public spending is vital as private sector sentiment may turn cautious; ICRA suggests that the West Asia crisis could delay private capex decisions until regional stability returns.

Sector-specific trends provide a mixed but generally resilient outlook:

- Steel and Cement: Steel demand growth is expected to improve to 9-10% in FY2027, with capacity utilization rising to approximately 83%. Cement volumes are projected to grow by 7-8%, supported by housing and infrastructure projects.

- Power and Energy: Electricity demand is expected to rebound to 5% growth in FY2027. Gross power generation capacity addition is estimated to reach 54 GW in FY2026, led primarily by the renewable energy segment.

- Agriculture: Upbeat farm sector trends, including estimated YoY increases in major Rabi crops, are expected to support rural consumption despite the global headwinds.

The combination of rising CPI inflation — projected to average 4.3% in FY2027 compared to 2.1% in FY2026 — and softening GDP growth leaves the Monetary Policy Committee (MPC) in a complex position. ICRA anticipates an “extended pause” on policy rates throughout the next fiscal year. However, the RBI is expected to remain active in managing liquidity and intervening to curb volatility in the USD/INR pair, which is likely to face a downward bias due to global sentiment and FPI sell-offs.

As India navigates these global cross-currents, the duration of the West Asia conflict will remain the single most influential factor in determining whether the economy can maintain its 6.5% growth floor or face further moderation.

(Cover photo by Rahul Kashyap on Unsplash)