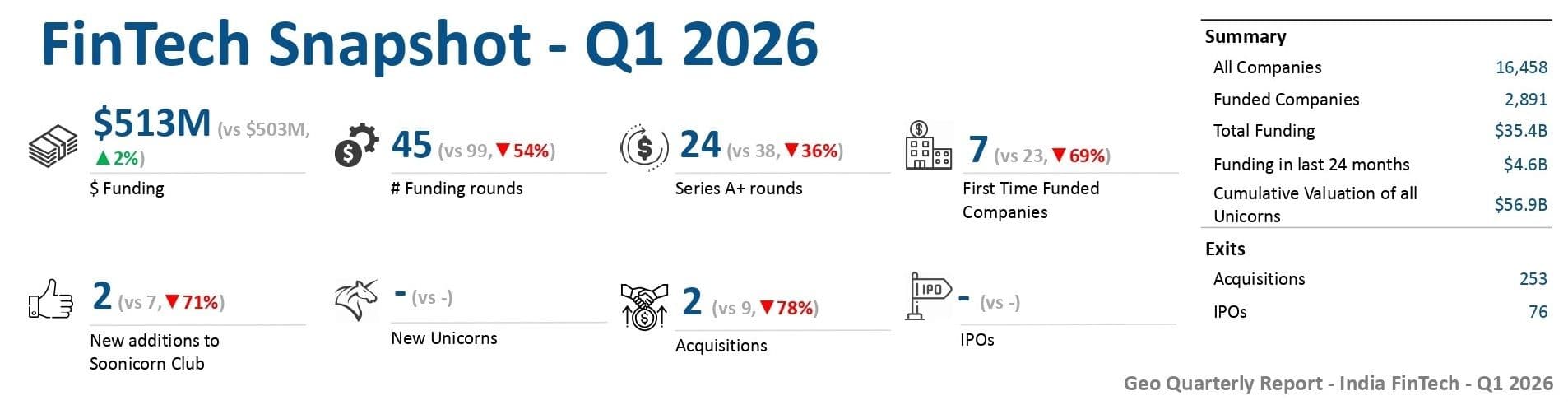

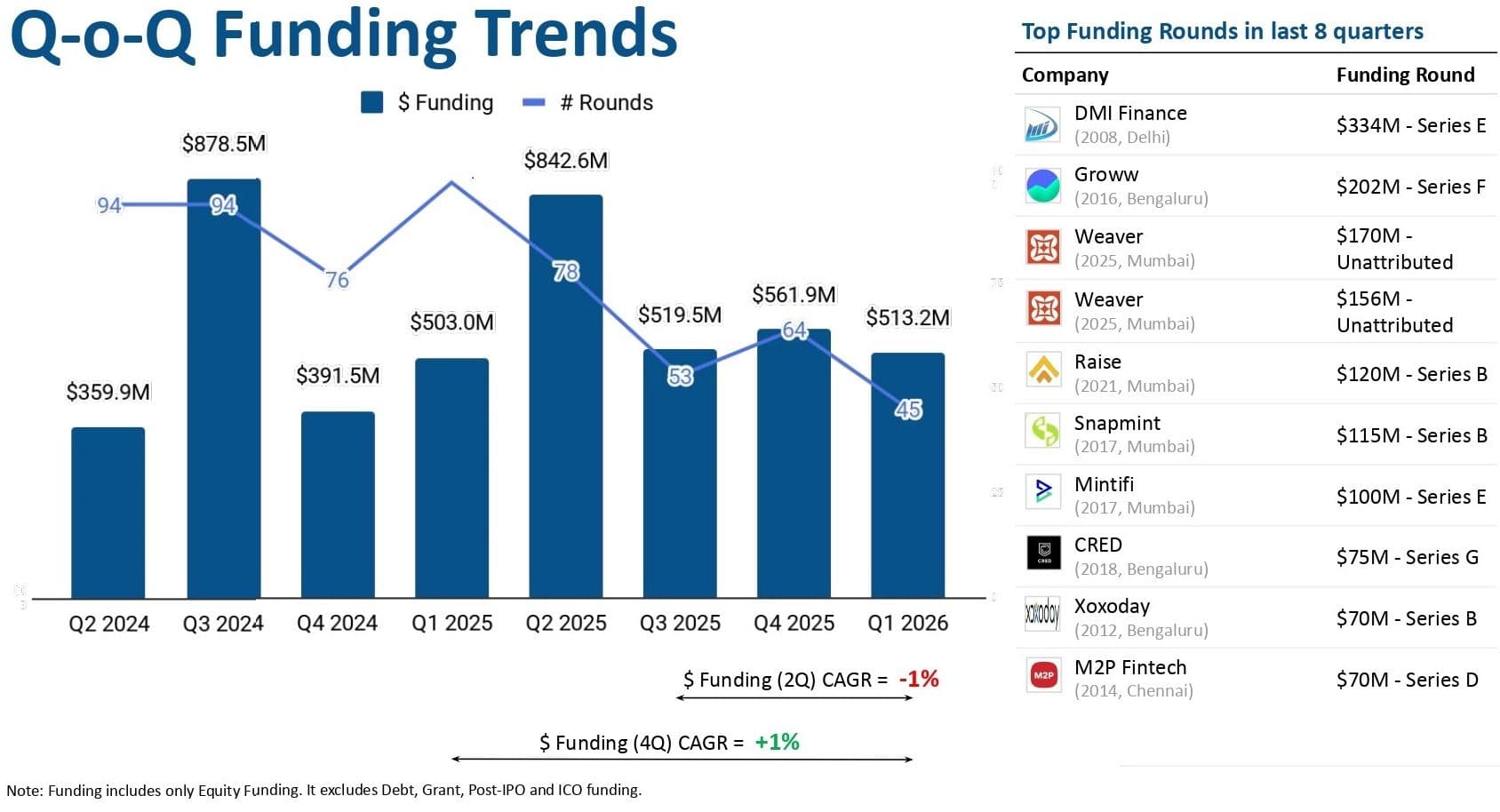

New Delhi: India’s fintech sector has begun 2026 on a note of apparent stability, masking an underlying stress. According to the Tracxn Geo Quarterly Report: India FinTech - Q1 2026, total funding in the January-March quarter stood at $513 million, reflecting a marginal 2% increase over $503 million in the same quarter of 2025. However, on a sequential basis, funding declined 9% from $562 million in Q4 2025, pointing to a softening momentum.

The stability in aggregate capital inflows contrasts sharply with deal activity. The number of funding rounds dropped to 45, down 54% from 99 deals a year earlier. Even more telling is the collapse in new participation, as only seven companies raised capital for the first time during the quarter, a steep 69% decline year-on-year.

This widening gap between funding volume and deal count signals a decisive change in how capital is being deployed. Investors are no longer spreading risk across a large number of startups. Instead, they are concentrating capital into a narrower set of companies that:

- demonstrate stronger operating metrics

- clearer monetisation pathways

- greater resilience to macroeconomic volatility.

The trend also reflects a broader reset under way in venture capital markets, where the emphasis has shifted from rapid scale and user acquisition to disciplined growth and capital efficiency. Fintech, once among the most aggressively funded sectors, is now exhibiting signs of maturation, with investors recalibrating expectations around returns and risk.

The divergence becomes more pronounced when funding is broken down by stage. Late-stage investments emerged as the primary driver of funding in Q1 2026, rising 126% quarter-on-quarter and 13% year-on-year to $273 million. This segment alone accounted for more than half of total funding during the quarter.

Early-stage funding, by contrast, declined sharply on a sequential basis, falling 47% to $214 million, although it remained 13% higher than the same period last year. The most severe contraction occurred at the seed stage, where funding dropped 65% year-on-year to $25.7 million, underlining growing investor reluctance to back early, unproven ventures.

The data indicates that capital is moving up the maturity curve. Investors are favouring companies that have already validated their business models and are closer to profitability, rather than those still in the experimentation phase. This is consistent with global venture capital trends, where higher interest rates and tighter liquidity conditions have made long gestation investments less attractive.

Large-ticket transactions are increasingly shaping the funding landscape. The quarter recorded one $100 million-plus round, with Mumbai-based Weaver raising $156 million. Such deals have a disproportionate impact on total funding figures, masking the broader slowdown in deal-making. Without these outliers, overall funding would likely have mirrored the sharp decline in transaction volumes.

The implication is clear. While capital remains available, it is being deployed selectively, with investors backing fewer companies but committing larger sums to each.

Lending Dominates

At a sectoral level, lending continues to dominate India’s fintech investment landscape. Alternative lending alone attracted $344 million in Q1 2026, accounting for a significant share of total funding. Affordable housing finance followed with $156 million, while banking technology drew $78.6 million.

This concentration reflects the relative maturity and scalability of credit-focused fintech models in India. Online lenders led the business model rankings, securing $310 million across 14 deals, far ahead of segments such as business payments, payment routing and regulatory technology.

The continued dominance of lending suggests that investors are prioritising segments with clearer revenue generation and predictable cash flows. In contrast, areas that rely heavily on customer acquisition or network effects without immediate monetisation are facing greater scrutiny.

Geographically, funding remains heavily concentrated in a few established hubs. Mumbai-based startups accounted for 61% of total funding at $311 million, while Bengaluru contributed 30% with $152 million. Other cities such as Gurugram, Delhi and Chennai together accounted for less than 10%, highlighting a sharp concentration of capital.

This geographic skew reflects investor preference for ecosystems that offer a combination of experienced founders, deep talent pools, and proximity to financial institutions. It also suggests that startups outside the leading hubs may face increasing challenges in accessing growth capital in a tightening funding environment.

Investors Turn Selective

Exit activity in Q1 2026 remained subdued, reinforcing the cautious tone of the market. The sector recorded just two acquisitions, down 50% compared to Q1 2025 and 78% lower than the previous quarter. There were no IPOs during the quarter, extending a slowdown in public market exits.

The most notable transaction was the $1.2 billion acquisition of Brahma by Polymarket, which accounted for the bulk of exit value. Beyond this, exit activity remained limited, reducing liquidity avenues for investors and potentially delaying return cycles.

Investor participation trends also point to a more selective funding environment. The number of new institutional investors declined, and first-time investor participation continued to weaken over recent quarters. Established venture firms such as Peak XV Partners, Lightspeed Venture Partners and Accel remained active at the early stage, while Bessemer Venture Partners and Analog Capital led late-stage investments.

The absence of new unicorns, combined with reduced deal flow and muted exit activity, signals a cooling of valuation momentum across the sector. However, this does not indicate a withdrawal of investor interest. Instead, it reflects a transition toward stricter evaluation standards, with greater emphasis on governance, profitability and sustainable growth. The trend is unambiguous. Fintech funding is no longer about volume. It is about selectivity, scale and disciplined capital allocation.

(Cover photo by Antonio Janeski on Unsplash)