New Delhi: India’s economic recovery is entering a more fragile phase as global geopolitical tensions, elevated crude oil prices and sustained foreign capital outflows tighten domestic financial conditions, raising fresh concerns over growth, inflation and fiscal stability.

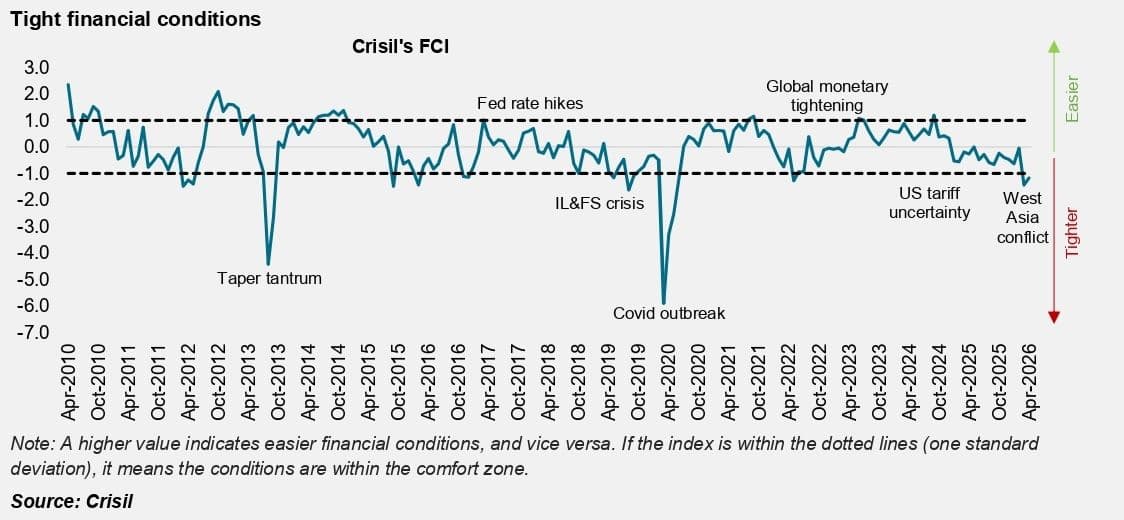

According to the Crisil report, Financial Conditions Index – Macroeconomics First Cut, released this week, India’s financial conditions remained under stress in April despite marginal improvement in liquidity and equity sentiment. The report said the Crisil Financial Conditions Index (FCI) stood at -1.2 in April compared with -1.4 in March, signalling conditions remained significantly tighter than the long-term average.

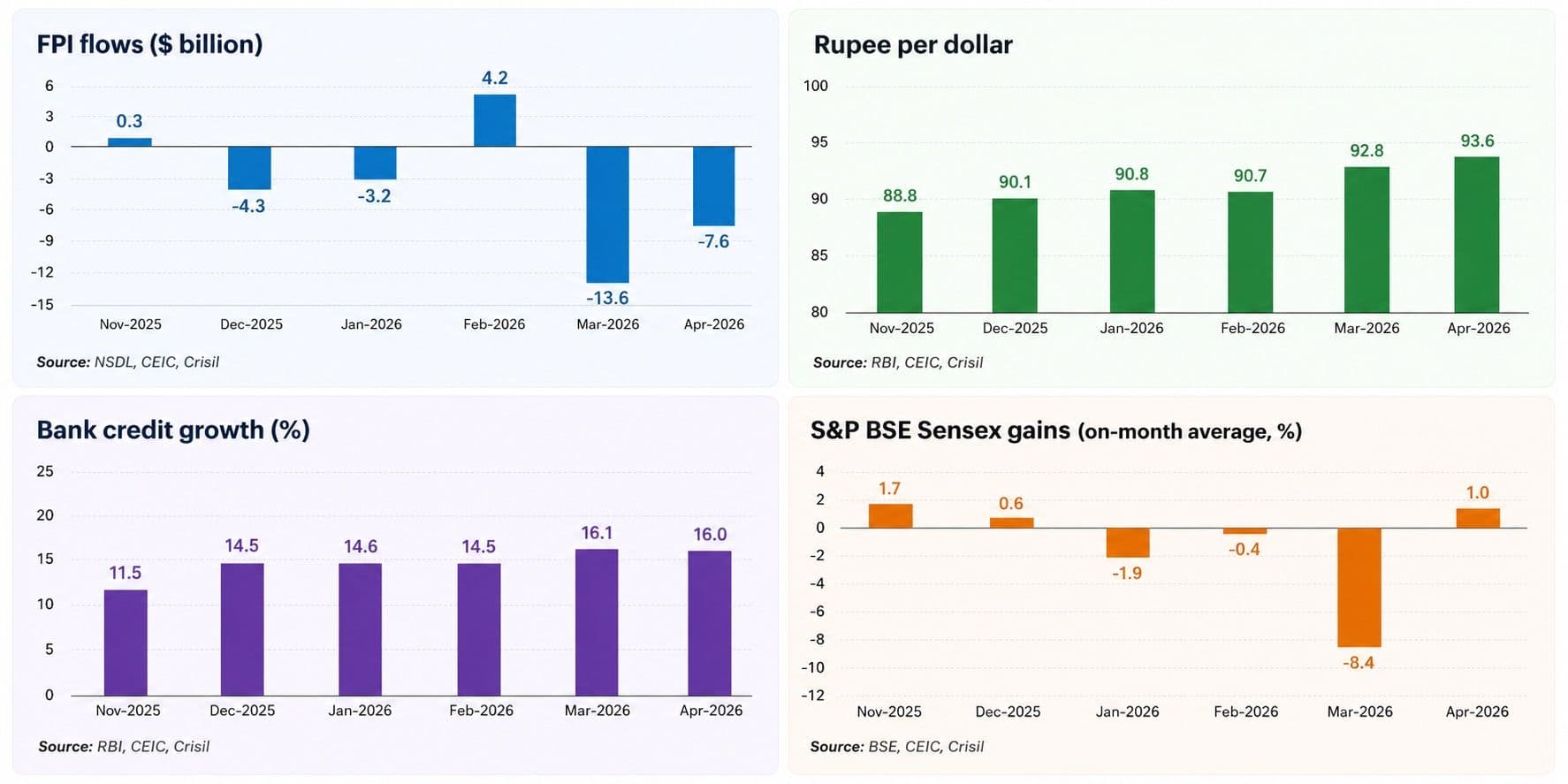

The report said escalating tensions in West Asia have emerged as the biggest external risk confronting the Indian economy, triggering volatility across currency, bond and equity markets. Foreign portfolio investors (FPIs) remained cautious amid geopolitical uncertainty, withdrawing $7.6 billion from Indian markets in April after pulling out $13.6 billion in March.

“The rupee surpassed 95 per dollar for the first time by month-end, driven by high FPI outflows and a surge in crude oil prices,” says the report. “The Reserve Bank of India’s (RBI) regulatory measures, such as capping banks’ net open rupee positions in the onshore deliverable market at $100, helped mitigate further rupee depreciation.”

The sharp depreciation in the rupee has amplified concerns over imported inflation at a time when crude oil prices remain elevated. Brent crude averaged $120.4 per barrel in April, the highest monthly average in more than a decade, after registering a 16.1% month-on-month increase, according to the report.

Bond markets, too, reflected growing investor nervousness. The benchmark 10-year government security yield rose sharply to an average 6.96% in April from 6.75% in March, weighed down by fiscal concerns, higher crude prices and sustained debt outflows.

“The term premium over the repo rate reached approximately 170 bps, its highest monthly average since September 2022,” according to the report. The tightening in sovereign yields points to mounting borrowing pressures for both the government and corporates as global risk aversion intensifies.

Growth Inflation Risks

The report paints a challenging macroeconomic outlook for India as inflationary pressures and weaker global demand threaten to erode growth momentum over the current fiscal year.

“Persistently elevated oil prices can have an impact on several macroeconomic indicators, including growth, inflation, the current account deficit and the fiscal deficit,” says the report. “Higher inflation domestically will shrink monetary space this fiscal.”

Crisil expects retail inflation to rise to 5.1% this fiscal compared with 2% last fiscal, driven by expectations of a below-normal monsoon and rising commodity prices. The report also warned that the RBI may have limited flexibility on rate actions if inflationary pressures persist.

The outlook on growth has also weakened materially. “We expect gross domestic product (GDP) growth to weaken to 6.6% from 7.6%, weighed down by higher commodity prices, an unfavourable monsoon, softer global growth and higher inflation, creating a challenging growth-inflation mix,” says the report.

The deterioration in financial conditions comes even as parts of the domestic economy continue to show resilience. Bank credit growth remained robust at 16% in April, supported by strong lending to services and personal loan segments. Systemic liquidity surplus also climbed to a four-year high of Rs 5 lakh crore in mid-April due to increased government spending and the maturity of government securities.

Still, economists believe the positive domestic indicators may not fully offset external vulnerabilities if geopolitical risks persist through the year. Elevated oil prices could widen India’s current account deficit while exerting additional pressure on the rupee and imported inflation.

The report also flagged shrinking monetary flexibility globally. It noted that S&P Global expects the European Central Bank (ECB) to raise rates twice during 2026, while the US Federal Reserve is likely to hold rates steady for the rest of the year instead of initiating earlier anticipated cuts.

Investor Confidence Wavers

Despite the broader stress in financial markets, Indian equities showed intermittent resilience in April amid hopes of easing geopolitical tensions and temporary moderation in crude prices.

“The benchmark indices, S&P BSE Sensex and Nifty 50, rose by an average of 1% and 1.2%, respectively,” according to the report. However, it added that market volatility remained above trend, reflecting continued investor caution.

The report said systemic liquidity conditions improved enough to soften several money market rates. Rates on six-month commercial paper and certificates of deposit eased meaningfully during April as surplus liquidity increased.

Yet, the broader financial environment remains vulnerable to external shocks. “The overall impact on financial conditions can amplify with the rise in scale, duration and intensity of external shock,” says the report. “Elevated global uncertainty may continue to cause nervousness among investors, leading to FPI outflows, adversely impacting equity markets and the rupee.”

The assessment underscores the increasingly difficult balancing act facing policymakers. While India’s domestic demand and banking system continue to provide some support to the economy, the combination of volatile oil prices, weaker currency, sticky inflation and slowing global growth is narrowing policy options.

The country’s macroeconomic fundamentals remain relatively resilient, but the external environment is turning significantly more hostile. As geopolitical tensions reshape capital flows and commodity markets, India’s economic trajectory in 2026 may depend less on domestic demand and more on how long global uncertainty persists.